If your insurance claim is unfairly denied or delayed, the Insurance Ombudsman is your strongest free legal ally. This guide shows how to use AI to turn scattered complaints into sharp, well-structured submissions that cite IRDAI rules and consumer laws, boosting your chances of success without costly legal help.

Table of Contents

Introduction

Last month, Samuel sat across from me in my office, clutching a stack of papers and wearing the frustrated expression I have seen on multiple clients’ faces over my decade-long career.

“Sir, they rejected my claim again,” he said, sliding the insurance company’s letter across my desk. “Third time. They are saying the accident was not covered, but I have read my policy ten times. I know I am right.” He paused, frustration in his eyes. “I even filed a complaint with the insurer, but they have not responded at all.”

I picked up the letter. Standard corporate language. Vague references to “policy exclusions.” No specific citations. Classic stalling tactics.

“Samuel,” I said, “have you heard of the Insurance Ombudsman?”

He shook his head.

“It is your option. Free, fast, and frankly, insurers hate it because they cannot buy their way out.” I leaned back in my chair. “But here is the thing, most people mess up their complaints so badly that even winning cases get thrown out on technicalities.”

Series recap and overview

Series overview and recap

In Part 4, we explored how to leverage AI assistance in drafting compelling internal grievance letters to insurance companies, providing legitimate claimants with a clear legal framework to challenge unjust claim denials. Today, via this article, I am going to share something that would have saved Samuel three months of frustration: how to use AI as your complaint-drafting partner.

Before diving in, here is what this comprehensive series covers:

Part 1: Fraud detection – Identify warning signs and behavioural indicators that expose insurance fraud before you fall victim.

Part 2: Legal strategy – Construct airtight cases, whether you’re pursuing fraud charges or defending against false accusations.

Part 3: Understanding your rights – Master every legal avenue available when insurance companies wrongfully reject your claims.

Part 4: Strategic complaints – Craft correspondence that compels insurance companies to take immediate action and provide prompt responses.

Part 5: Ombudsman intervention (Current article) – Harness this no-cost, influential mechanism to compel companies to honour their payment obligations.

Part 6: Consumer protection – Secure not only your claim settlement but also compensation for harassment and emotional distress.

Part 7: Criminal action – Lodge police complaints that prosecutors will actively pursue in cases of fraud and deception.

Part 8: Constitutional safeguards – Access to High Court intervention when fundamental rights are breached or emergency relief is required.

Your complete guide to insurance justice is at your fingertips!

Understanding the Insurance Ombudsman

Before we dive into AI-powered drafting, let me explain exactly what the Insurance Ombudsman is and when you can approach this powerful grievance mechanism.

What is the insurance ombudsman?

The Insurance Ombudsman is a quasi-judicial authority established under the Insurance Ombudsman Rules 2017, by the Insurance Regulatory and Development Authority of India (IRDAI). Think of it as a specialised court for insurance disputes, but without the formal court procedures and costs.

“Is it really free?” Samuel had asked me during our first meeting.

Absolutely. No filing fees, no lawyer fees required, and no court costs. The entire process is designed to be accessible to policyholders.

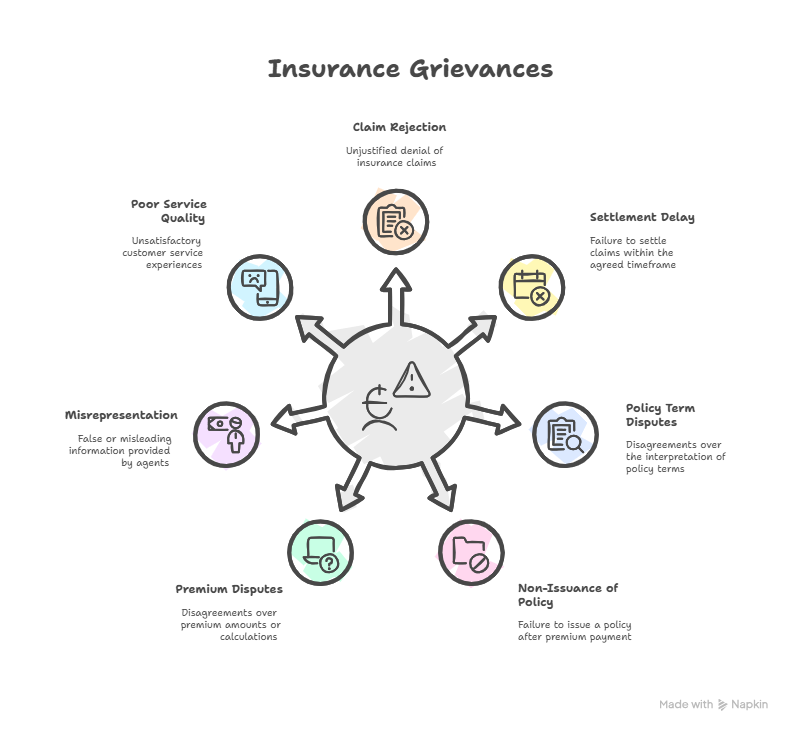

When can you approach the ombudsman?

Here are the specific grounds under which you can file a complaint:

Timelines that you must know:

- You must first give the insurance company a chance to resolve your grievance (minimum 30 days)

- You have one year from the date of final rejection by the insurer to approach the Ombudsman

- Claims above Rs. 50 lakhs are generally outside the Ombudsman’s jurisdiction (though this varies by region)

Jurisdictional boundaries:

India has 17 Insurance Ombudsman offices covering different states and union territories. You must approach the ombudsman in whose jurisdiction:

- Your insurance policy was issued, OR

- You reside or work, OR

- The cause of action arose

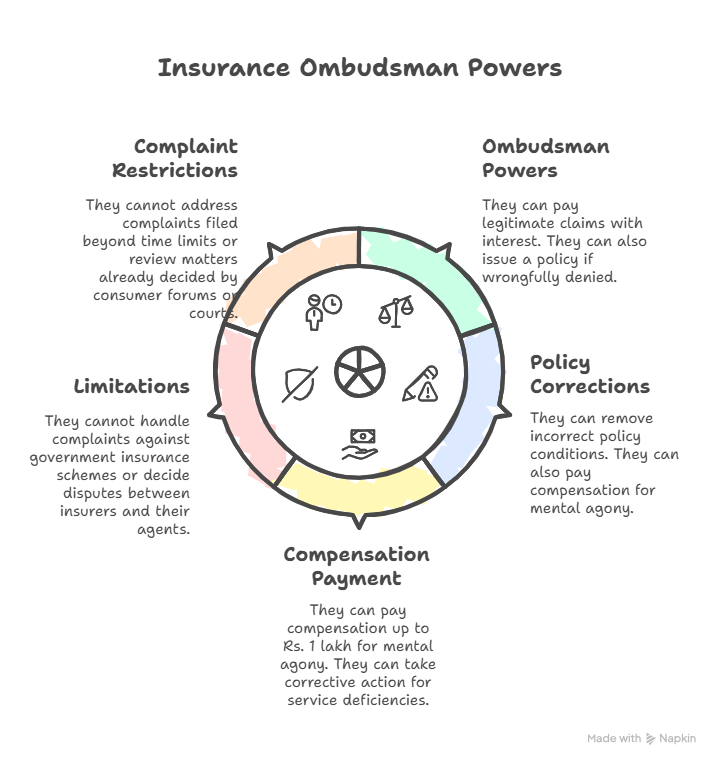

What the Ombudsman can and cannot do for you:

I always tell my clients: “The Ombudsman’s decision is binding on the insurance company, but not on you. If you are not satisfied, you can still approach consumer courts or civil courts.”

Now that you understand the framework, let us see how AI can help you navigate this system effectively.

Here is your step-by-step framework

Before we dive deeper into Samuel’s journey, let me share something important about the AI tool selection process.

For Samuel’s case, we primarily used Claude AI, though this entire framework works just as effectively with ChatGPT, Bard, or other AI platforms. Here is why Claude became our go-to choice for these complaints:

- Maintains a formal, professional tone that Ombudsmen expect

- Shows solid understanding of Indian legal frameworks and consumer protection laws

- Excels at organising messy, emotional narratives into clean chronological order

- Less prone to making up legal citations or referencing non-existent case law

But here is the reality check: The prompts and AI responses I am sharing with you are carefully drafted examples based on patterns I have observed across hundreds of insurance disputes. Your actual results might look different depending on several factors:

- Which AI platform will you choose (free ChatGPT vs. paid Claude vs. Google Bard)

- The specific version you are accessing (AI models get updated constantly)

- How do you phrase your prompts and questions

- The unique complexity of your particular case

Consider these examples as a template, not a guaranteed outcome. The framework works, but like any tool, your skill in using it matters.

Step 1: But first, tell AI what you need

“But I do not know how to explain what happened!”

Samuel’s frustration is universal. Most people start by dumping their entire story on AI, hoping it will magically sort everything out. That is like giving a chef random ingredients and expecting a perfect dish.

Instead, I have learned to flip the process. Let AI tell you what it needs first.

“Think of AI as your client,” I told Samuel. “Before you begin to draft, you would ask them what information you need to draft a proper complaint, right?”

Here’s our opening conversation with Claude:

Samuel: “I want to file a complaint with the Insurance Ombudsman regarding a rejected motor insurance claim. Please give me a list of all the factual and legal questions I should answer so you can help me draft a proper complaint.”

Claude’s response:

“I’ll need comprehensive information to draft an effective complaint. Please provide:

Factual Details:

- Your complete contact information (name, age, occupation, address, phone, email)

- Insurance company name, branch, and contact details

- Policy specifics (number, type, issue date, validity period, premium amount)

- Vehicle details (make, model, year, registration number)

- Incident details (date, time, location, nature of accident/damage)

- Claim process timeline (submission date, documents provided, insurer responses)

- Specific rejection reason given by the insurer

- All follow-up communications were attempted

- Financial impact (repair costs, loss amount, expenses incurred)

Legal Prerequisites:

- Have you first complained to the insurer and waited 30 days?

- Is this a personal policy (not commercial)?

- Is the claim value under Rs. 50 lakhs?

- Is this matter pending in any other court?

- Are you filing within one year of the insurer’s final response?*

Why this approach works: Instead of guessing what is important, AI gives you a structured checklist. Samuel immediately saw gaps in his own understanding.

“I forgot to keep track of exact dates,” he admitted. “And I did not know the one-year rule existed.”

This single conversation prevented what could have been a dismissed complaint due to incomplete information.

Step 2: Feed AI the complete facts

With Claude’s questions as our guide, Samuel could now provide a comprehensive, organised response instead of an emotional dump.

Samuel’s structured response:

Samuel: “Here are my answers to your questions:

Personal details: Samuel Thompson, 34, Software Engineer, Flat 204, Green Park Apartments, Santacruz (west), Mumbai – 401301. Phone: 9876543210, Email: [email protected]

Insurer details: SecureAuto Insurance Company Limited, Santacruz (west), Mumbai.

Policy information: Policy No. SA-45789, Comprehensive Motor Insurance, Valid from 15 March 2024 to 14 March 2025, Annual Premium: Rs. 18,500

Vehicle: Honda City 2022, Registration: MH02CZ1234

Incident: 17 May 2024, around 2:30 PM, a car was rear-ended by a truck while stopped at a traffic light on the Mumbai Pune Expressway. Major damage to the rear bumper, boot, and taillights.

Claim process: Filed claim on 18 May with FIR copy, photos, garage estimate of Rs. 65,000, and filled claim forms. The insurer rejected on 25 June, citing ‘pre-existing damage to the vehicle not disclosed at policy inception.’

Follow-up: Sent emails on 28 June and 5 July requesting clarification. No response was received.

Legal compliance: Yes, filed a complaint with the insurer on 2 July, 30+ days have passed. Personal vehicle. claim under Rs. 50 lakhs. Not filed elsewhere. Within one year.”

Claude’s immediate response:

“Thank you for the comprehensive information. I can see several strong legal grounds for your complaint:

- Deficiency in Service: The insurer failed to specify what ‘pre-existing damage’ they are referring to

- Unfair Trade Practice: The rejection reason is vague and potentially fabricated

- Breach of Contract: If no such pre-existing damage exists, rejection is wrongful

Before I drafted the complaint, I noticed the insurer took 39 days to respond to your claim (18 May to 25 June). This delay itself is a grievance ground under IRDAI guidelines that require claim settlement within 30 days.

Should I include this delay as an additional grievance point?”

Samuel was amazed. “I did not even realise the delay was a separate issue!”

This is the power of structured information feeding. AI does not just organise your facts, it identifies legal arguments you might have missed.

Step 3: Ask AI to draft the complete complaint

Now comes the moment of truth. With organised facts and identified legal grounds, AI can create a professional-grade complaint.

Our drafting prompt:

Samuel: “Using the above facts, draft a complete complaint to the Insurance Ombudsman. Make it formal but not overly legalistic. Ensure that the deficiency and such other defaults are clearly highlighted in the complaint.”

Claude’s draft:

Here is the draft.

Samuel read through the draft twice. “This looks like it came from a law firm,” he said, clearly impressed.

The transformation was remarkable. From scattered facts to a structured, persuasive legal document. But we were not done yet.

Step 4: Ask AI to refine the tone and add legal precision

Legal accuracy is crucial, but so is tone. The first draft was formal but needed that perfect balance, assertive without being aggressive, and detailed without being verbose.

Our refinement conversation:

Samuel: “Polish this complaint to make it more professional and respectful for filing before the Insurance Ombudsman. Also, ensure the legal language is precise and the tone remains objective throughout.”

Claude’s refined version (key improvements):

“FACTS OF THE CASE (Revised): I respectfully submit that on 17 May 2024, my insured vehicle was involved in an accident while stationary at a traffic signal. The vehicle was rear-ended by a truck, causing substantial damage to the rear portion, as evidenced in the enclosed photographs.

Claim intimation was made within 24 hours as required under the policy terms. All requisite documents were submitted promptly on 18 May 2024. Despite this compliance, the insurer took 39 days to respond, well beyond the IRDAI-mandated 30-day timeline for claim settlement.

The rejection, when it finally came, was based on an allegation of ‘pre-existing damage not disclosed at policy inception.’ This allegation is factually incorrect and appears to be a pretext to avoid a legitimate claim settlement.

NATURE OF GRIEVANCE (Enhanced): The complainant submits that the insurer’s conduct constitutes:

a) Unfair Trade Practice under the Consumer Protection Act, 2019, by making false allegations to reject a valid claim b) Deficiency in Service by failing to settle/reject the claim within the prescribed 30-day period c) Breach of Good Faith by not providing specific details of the alleged pre-existing damage d) Negligent Customer Service by failing to respond to legitimate queries seeking clarification”.

The difference was subtle but significant. The refined version sounded more like a legal brief and less like a customer complaint. It cited specific laws and used precise legal terminology while maintaining respectful language.

Step 5: Generate annexures

“What documents do I actually need to attach?” Samuel asked.

This question stumps most people. They either attach everything (creating unwieldy 50-page submissions) or miss critical documents (getting complaints dismissed for incompleteness).

Our annexure conversation:

Samuel: “Based on this complaint, create a numbered annexure list and provide a comprehensive checklist of documents needed for filing with the Insurance Ombudsman.”

Claude’s systematic response:

“ANNEXURE LIST:

Annexure-1: Copy of Insurance Policy No. SA-45789;

Annexure-2: Premium payment receipts

Annexure-3: FIR No. 445/2024 dated 17 May 2024

Annexure-4: Claim intimation letter dated 18 May 2024

Annexure-5: Completed claim form with acknowledgement

Annexure-6: Photographs of the accident site and vehicle damage

Annexure-7: Garage repair estimate dated 20 May 2024

Annexure-8: Claim rejection letter dated 25 June 2024

Annexure-9: Email communications dated 28 June and 5 July 2024

Annexure-10: Complaint to insurer dated 2 July 2024

This systematic approach impressed even me. In eight years of practice, I have seen lawyers miss documents that AI caught automatically.

Step 6: Manual edits

Samuel: “The AI draft looks good. Should I submit it directly?”

Me: “Hold on. Always do a manual review first, check all dates, add personal details AI missed, and make sure it sounds like your voice, not a robot’s.”

Samuel: “What should I focus on?”

Me: “Accuracy of facts, personal impact details, and authentic tone. AI gives you the framework, but your personal touches make it believable.”

To,

Date: 03/07/2024

The Insurance Ombudsman,

3rd Floor,

Jeevan Seva Annexe,

S. V. Road,

Santacruz (W), Mumbai – 400 054.

Subject: Complaint against SecureAuto Insurance Company Limited – Wrongful rejection of motor insurance claim and deficiency in service

- I, Samuel Thompson, aged 34 years, working as a Software Engineer and residing at Flat 204, Green Park Apartments, Santacruz (West), Mumbai – 401301, respectfully submit this complaint against SecureAuto Insurance Company Limited for wrongful rejection of my motor insurance claim and gross deficiency in service.

- I hold a comprehensive motor insurance policy bearing number SA-45789 with SecureAuto Insurance Company Limited, issued from their Santacruz (West), Mumbai branch. The policy covers my Honda City 2022 vehicle (Registration: MH02CZ1234) for the period from 15 March 2024 to 14 March 2025, for which I have paid an annual premium of Rs. 18,500 in full. As a responsible policyholder, I have maintained regular premium payments and complied with all policy terms and conditions throughout the policy period.

- The present complaint arises from the insurer’s wrongful rejection of my legitimate motor insurance claim following an accident that occurred on 17 May 2024, where my vehicle suffered significant damage due to being rear-ended by a truck while stationary at a traffic signal. Despite submitting all required documentation promptly and following proper procedures, the insurer has rejected my claim based on vague and unsubstantiated allegations, causing me considerable financial hardship and mental agony.

- It is crucial to mention at the outset that at the time of purchase, the agent of SecureAuto Insurance made explicit promises about their “hassle-free claim settlement process” and “quick resolution within 15-20 days.” The agent assured me that comprehensive coverage meant complete protection from accidents and that their company was known for customer-friendly claim handling. Based on these representations and the trust placed in their service commitments, I decided to choose SecureAuto over other available insurers in the market.

- I submit that on 17 May 2024, my insured vehicle was involved in an accident while stationary at a traffic signal. The vehicle was rear-ended by a truck, causing substantial damage to the rear portion, as evidenced in the enclosed photographs.

- Claim intimation was made within 24 hours as required under the policy terms. All requisite documents were submitted promptly on 18 May 2024. Despite this compliance, the insurer took 39 days to respond, well beyond the IRDAI-mandated 30-day timeline for claim settlement.

- The rejection, when it finally came, was based on an allegation of ‘pre-existing damage not disclosed at policy inception.’ This allegation is factually incorrect and appears to be a pretext to avoid a legitimate claim settlement.

- The complainant submits that the insurer’s conduct constitutes:

- Unfair trade practice under the Consumer Protection Act 2019, by making false allegations to reject a valid claim

- Deficiency in service by failing to settle/reject the claim within the prescribed 30-day period

- Breach of good faith by not providing specific details of the alleged pre-existing damage

- Negligent customer service by failing to respond to legitimate queries seeking clarification

- The above grievances constitute violations under:

- Consumer Protection Act 2019 – Unfair trade practices and deficiency in service

- Insurance Act 1938 and IRDAI regulations regarding timely claim settlement

- Indian Contract Act 1872 – Breach of contractual obligations

- IRDAI (Protection of Policyholders’ Interests) Regulations, 2017

- In light of the above facts and circumstances, I humbly request you to

respectfully pray that this Hon’ble Office may be pleased to:

- Direct SecureAuto Insurance Company Limited to settle my legitimate claim amounting to Rs. 65,000 within 15 days of this order

- Award interest at the rate of 12% per annum on the claim amount from the date of claim submission (18 May 2024) till the date of actual payment

- Award compensation of Rs. 20,000 for mental harassment, inconvenience, and deficiency in service caused by the insurer’s wrongful actions

- I

most respectfullya loyal customerpaying premiums regularly, and this wrongful rejection has caused me significant financial hardship and mental agony. I trust that this Hon’ble Office will ensure justice is served and direct the insurer to settle my legitimate claim at the earliest.

Place: Mumbai

Date: [Current Date]

Yours faithfully,

Samuel Thompson

Complainant

Enclosures:

Annexure-1: Copy of Insurance Policy No. SA-45789

Annexure-2: Premium payment receipts for 2024-25

Annexure-3: FIR copy dated 17 May 2024

Annexure-4: Claim intimation letter dated 18 May 2024

Annexure-5: Completed claim form with acknowledgement

Annexure-6: Photographs of the accident site and vehicle damage

Annexure-7: Garage repair estimate dated 20 May 2024

Annexure-8: Claim rejection letter dated 25 June 2024

Annexure-9: Follow-up email communications dated 28 June and 5 July 2024

Annexure-10: Formal grievance submitted to insurer dated 2 July 2024

Annexure-11: Copy of driving license and vehicle registration certificate

Step 7: Follow-up communications

“What if they do not respond?” Samuel asked a common concern.

Our follow-up strategy:

Samuel: “Write a professional follow-up email to check the status of my Insurance Ombudsman complaint filed 45 days ago, without sounding impatient or demanding.”

Claude’s follow-up template:

“Subject: Status Inquiry – Complaint No. [Reference Number] Against SecureAuto Insurance

Dear Sir/Madam,

I hope this email finds you well. I am writing to inquire about the status of my complaint filed on [Date] against SecureAuto Insurance Company (Policy No. SA-45789).

As 45 days have elapsed since submission, I would be grateful for a brief update on the current status of my case. Please let me know if any additional information or documentation is required from my end.

Thank you for your continued attention to this case.

Yours truly,

Samuel Thompson

Complaint Reference: [Number if available]

Contact: 9876543210

Why this AI approach works

Clarity beats emotion. AI helps separate facts from feelings.

Structure impresses. Proper formatting signals that you understand the system.

Completeness prevents dismissal. AI catches missing elements that could derail your case.

Consistency builds credibility. Every document follows the same professional standard.

Speed matters. What used to take weeks now takes hours.

Final thoughts

If you are facing an insurance dispute, do not let frustration cloud your judgment. Use AI as your drafting partner, but remember, it is a tool, not a lawyer.

For complex cases involving significant amounts or technical issues, consult a lawyer after preparing your AI-assisted draft. You will save time and money by arriving prepared.

For straightforward cases like Samuel’s, this AI approach might be all you need to level the playing field against insurance companies.

Remember: The Insurance Ombudsman is free, fast, and final. But only if you approach it right.

Frequently asked questions

- Can I use AI to draft complaints even if I am not tech-savvy?

Most AI platforms like ChatGPT are designed for everyday users. Just copy-paste the prompts I’ve provided and follow the structure. Think of it as having a legal assistant who works 24/7.

- Will the Ombudsman know I used AI to draft my complaint?

There is no requirement to disclose drafting methods, and a well-polished complaint actually demonstrates seriousness about your case. The focus should be on accuracy and completeness, not the drafting process.

- What if my insurance company has powerful lawyers and I’m just using AI?

The beauty of the Ombudsman system is that it levels the playing field. Corporate lawyers cannot argue procedure or technicalities when your complaint is properly structured and factually accurate.

- How long does the entire Ombudsman process take from complaint to resolution?

Typically 3-6 months, but many cases settle earlier once insurers realise they are facing a serious, well-documented complaint. The AI drafting process itself takes just a few hours.

- Can I use this same AI approach for other types of legal complaints?

Absolutely! The principles work for consumer courts, banking ombudsmen, and other grievance forums. Just adjust the prompts to match the specific requirements of each forum.

Allow notifications

Allow notifications