Learn how to use AI to draft risk management, CSR, and operational disclosures that transform compliance into strategic positioning. In Part 6 of our board report series, discover how to balance transparency with competitive advantage, creating forward-looking assessments that build investor confidence while maintaining legal protection.

Series overview: AI-powered board report preparation under section 134

This is Part 6 of our 8-part series on using AI to draft board reports under the Companies Act 2013.

Complete Series Overview:

- Part 1: Getting started

- Part 2: Building the foundation (Group 1)

- Part 3: Financial performance and capital management (Group 2)

- Part 4: Directors’ statements and professional judgment (Group 3)

- Part 5: External stakeholders and audit relations (Group 4)

- Part 6: Risk management and CSR disclosures (Group 5) ← You are here

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – complete board report

Haven’t started from Part 1? No problem! This article works standalone, but you will get more value by reading the series sequentially.

What you will learn in this article:

Risk and CSR disclosures require a completely different mindset – transforming abstract business philosophy into concrete strategic narratives. You will see how Arjun and Ms. Rao handle risk disclosure without creating investor anxiety and CSR narratives that demonstrate genuine business integration.

Key characters:

- Arjun Sharma: Junior lawyer developing advanced AI collaboration skills

- Ms. Priya Rao: Senior partner, now confident in strategic AI applications

- Nova AgriTech: Their client needs sophisticated risk and CSR positioning

Recap:

[For series readers: Skip to “Today’s Focus” below]

[For new readers: Here is what happened so far]

The journey so far:

Ms. Rao was skeptical about AI for legal work. Through parts 1-5, Arjun demonstrated systematic AI collaboration that produced investment-grade content. They have successfully completed governance foundations, financial storytelling, directors’ statements, and external stakeholder communications. Each group built logically while maintaining professional excellence.

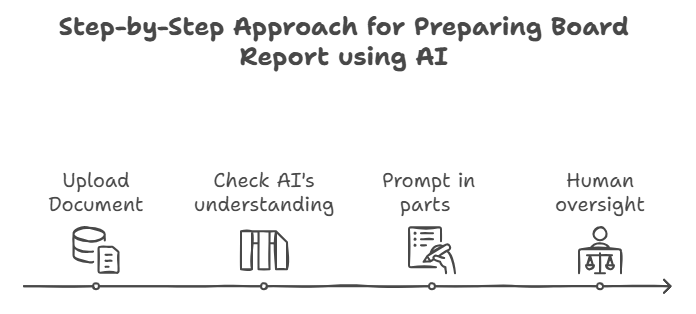

The step-by-step approach we have developed:

- Document-based context (upload comprehensive company info)

- Strategic analysis (test Claude’s understanding)

- Step-by-step improvement (refine drafts through focused prompts)

- Human oversight (lawyer review and validation)

Groups completed so far:

- Group 1: Company identity and governance

- Group 2: Financial performance and highlights

- Group 3: Directors’ statements and professional judgment

- Group 4: External stakeholders and audit relations

- Group 5: Risk and CSR disclosures (today’s focus)

Today’s focus: Group 5

In this article, watch Arjun and Ms. Rao navigate the most subjective board report content – areas where legal requirements intersect with corporate philosophy and strategic communication psychology.

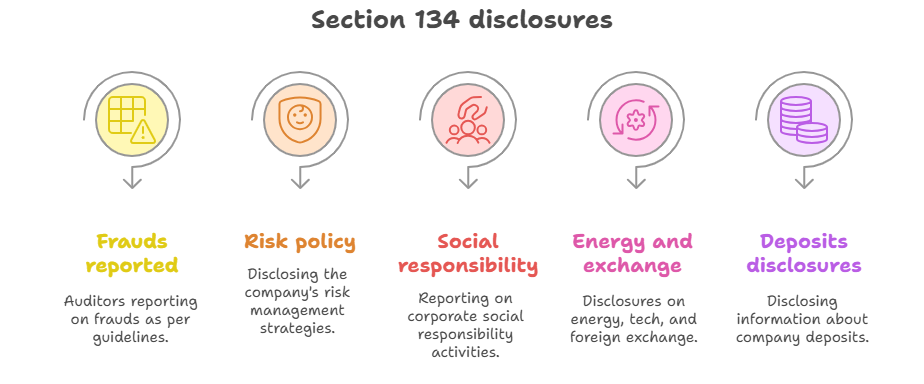

Group 5 requirements we are covering:

- Section 134(3)(c1): Frauds reported by auditors

- Section 134(3)(n): Risk management policy

- Section 134(3)(o): Corporate social responsibility

- Section 134(3)(m): Energy conservation, technology absorption, foreign exchange

- Rule 8(5)(v-vi): Deposits disclosures

By the end, you will understand:

- How to create philosophical context documents for AI analysis

- Techniques for balancing transparency with competitive sensitivity

- Ways to transform compliance into strategic advantage narratives

Prompting for risk and CSR disclosures in the board report

“Ms. Rao, do you want to try giving prompts for this group?” Arjun asked, settling into his chair at Khanna Legal Solutions.

Ms. Rao set down her coffee after a break, studying the screen with interest. “You know what? I would like that. After watching you handle the first four groups, I am curious to test my own prompting skills.”

She leaned forward, examining the requirements. “Unlike other groups, this one is where we identify threats that could threaten the company’s existence. CSR narratives that need to sound authentic rather than corporate-speak. Forward-looking assessments that balance optimism with legal protection.”

“Exactly the challenge,” Arjun agreed. “How do you prompt an AI to navigate corporate philosophy?”

Ms. Rao considered this thoughtfully.

“Every previous group built on concrete foundations – governance facts, financial data, legal requirements, stakeholder relationships. But Group 5 is about judgment calls that even experienced lawyers struggle with.”

“Risk tolerance, social responsibility, authenticity, strategic optimism – balanced with legal protection,” Arjun added. “These are not technical skills Claude can learn from documentation.”

“Which makes this the perfect test,” Ms. Rao said, a slight smile crossing her face.

“Can our systematic approach handle subjective professional judgment, or have we found its limits? Let’s find out.”

Creating a management philosophy document for Claude

Ms. Rao opened a fresh document on her laptop. “If I am going to prompt this effectively, I need to think differently about our context approach.”

“How so?” Arjun asked, curious to see her perspective.

“Groups 1-4 succeeded because we gave Claude comprehensive factual context. But Group 5 requires something different.” She began typing. “What if we teach Claude to think like Nova’s management team rather than just giving it business facts?”

Arjun nodded approvingly. “You are thinking about creating a philosophical intelligence briefing document rather than a factual context document.”

“Precisely. Claude needs to understand Nova’s management philosophy – risk tolerance, communication preferences, strategic positioning principles. The invisible framework that guides how leadership wants to position the company.”

She continued working on the document, occasionally pausing to consider her approach.

Nova AgriTech risk & impact philosophy – Group 5 context

Management’s risk philosophy: Nova’s leadership views risk management as a strategic advantage demonstration rather than defensive compliance. The company operates on the principle that sophisticated risk identification and proactive mitigation actually build investor confidence by showing management competence.

Identified business risks with strategic positioning:

- Technology obsolescence risk: Rapid 18-month innovation cycles in IoT/AgriTech Management positioning: Emphasize proactive R&D investment and technology partnerships as mitigation

- Regulatory changes: State-level agricultural policy variations affecting adoption. Management positioning: Frame regulatory engagement and compliance excellence as competitive moats

- Competitive threats: Agricultural giants entering precision farming.

Management positioning: Present as market validation and emphasize first-mover advantages - Climate variability: Weather impacts on agricultural demand Management positioning: Position adaptive technology as a solution, not a victim of climate change

CSR integration philosophy: Nova’s leadership refuses to treat CSR as separate from business strategy. Every social initiative must demonstrate clear business value while creating genuine community impact.

CSR strategic business integration:

- Farmer training programs (1,200+ professionals): Market expansion disguised as social responsibility

- Sustainable technology (25% chemical reduction): Competitive differentiation through environmental innovation

- Rural employment (45 new jobs): Market penetration enabler and community relationship builder

- University partnerships: R&D strategy and talent pipeline development disguised as academic collaboration

Operational excellence strategic positioning: Management views operational metrics as competitive advantage evidence rather than compliance reporting.

- Energy conservation (15% reduction): Demonstrates operational sophistication and cost management

- Technology absorption (40% import substitution): Proves innovation capability and strategic independence

- Foreign exchange management (30% exposure reduction): Shows international business readiness

- Process optimization (12% cost reduction): Validates scalability and margin expansion potential

Strategic communication principles:

- Strategic optimism: Honest assessment within a confident business narrative

- Proactive positioning: Frame challenges as opportunities under management control

- Evidence-based confidence: Support all forward-looking statements with historical performance

- Competitive intelligence protection: Transparency without strategic vulnerability

“This captures the strategic philosophy behind every disclosure,” Ms. Rao said, reviewing her work.

“Now Claude can understand that when we discuss risks, we are demonstrating management sophistication. When we describe CSR, we are providing business strategy integration.”

“The strategic communication principles section will be particularly important,” Arjun observed. “That gives Claude the framework for balancing transparency with confidence.”

Testing Claude’s philosophical understanding

“Alright, just like the last 4 groups, I must first upload the document before asking Claude to draft anything,” Ms. Rao said. ” I am first testing whether Claude can understand corporate communication psychology.”

Ms. Rao, after taking some time, crafted this prompt:

First prompt:

“Based on the Nova AgriTech Risk & Impact Philosophy document uploaded, analyze how Group 5 disclosures require different communication psychology than Groups 1-4.

Focus specifically on:

(1) Risk communication that demonstrates management sophistication without creating business sustainability anxiety,

(2) CSR narratives that show genuine social impact while positioning initiatives as business strategy validation,

(3) Forward-looking assessments that display strategic thinking without creating liability exposure,

(4) Operational disclosures that transform technical metrics into competitive advantage evidence.

Explain how these communication challenges require ‘strategic optimism’ – honest assessment within confident business narrative frameworks that maintain investor confidence while satisfying transparency requirements.”

Claude’s response (Click here to see) demonstrated a sophisticated understanding that impressed both lawyers.

“Look at this strategic framing,” Ms. Rao said, reading through the comprehensive analysis.

“Claude wrote: ‘Group 5 disclosures require fundamentally different communication psychology that transforms traditional compliance reporting into strategic positioning.’ That’s exactly the insight we needed.”

Arjun scrolled through Claude’s response with growing amazement.

“Notice how it understood risk communication as ‘management credibility signaling.’ That’s not legal analysis – that’s strategic communication theory.”

Claude had positioned Nova’s approach as sophisticated risk identification that actually builds investor confidence rather than undermining it.

The AI explained how institutional investors interpret thorough risk analysis as management sophistication, while similar disclosures from smaller companies might signal weakness.

“The CSR analysis is particularly insightful,” Ms. Rao observed.

“Claude understood Nova’s approach of rejecting traditional separation between social responsibility and business strategy. Their farmer training programs become ‘market expansion disguised as social responsibility’ – capturing exactly how authentic CSR should integrate with business objectives.”

“And look at the forward-looking assessment framework,” Arjun added.

“Claude positioned it as ‘evidence-based confidence’ – supporting all projections with historical performance while maintaining proactive positioning. That demonstrates understanding of legal liability management.”

Drafting the complete group 5 board report disclosure

With Claude’s philosophical understanding confirmed, Ms. Rao moved to implementation:

“Now for the real test,” she said, crafting her second prompt.

Second prompt:

“Apply your ‘strategic optimism’ framework to draft Nova AgriTech’s complete Group 5 disclosures for their FY 2024-25 board report.

Structure as:

(1) Section 134(3)(c1) – Frauds reported by auditors (demonstrate robust detection systems) (2) Section 134(3)(n) – Risk management policy (use your ‘management credibility signaling’ approach)

(3) Section 134(3)(o) – Corporate social responsibility (apply your ‘CSR as business strategy validation’ framework)

(4) Section 134(3)(m) – Energy conservation, technology absorption, foreign exchange (use your ‘operational excellence as competitive advantage’ approach)

(5) Rule 8(5)(V-VI) – Deposits disclosures (confirm non-applicability while demonstrating financial sophistication)

Maintain strategic optimism principles: proactive transparency, strategic context integration, evidence-based confidence, and competitive intelligence protection.”

“I like how you structured that,” Arjun observed. “You are asking Claude to apply the specific frameworks it identified rather than giving generic instructions.”

“Exactly. If Claude truly understood the communication psychology, it should be able to execute on its own insights,” Ms. Rao replied.

Click here to see the conversation with Claude.

Claude produced a favourable response

The board report language that appeared represented a quantum leap in AI-assisted legal drafting.

“This is extraordinary,” Ms. Rao said, reviewing the comprehensive response. “Look at the fraud disclosure opening: ‘Nova AgriTech’s comprehensive fraud detection and prevention framework reflects our commitment to operational excellence and stakeholder confidence.’ Even a ‘no frauds reported’ disclosure becomes evidence of sophisticated governance.”

Strategic implementation highlights:

1. Fraud disclosure – Turning zero risk into governance strength

Rather than simply stating “no frauds reported,” Claude constructed a sophisticated governance narrative positioning Nova’s clean record as evidence of superior risk management systems, featuring “AI-powered transaction monitoring” and “institutional-grade risk management capabilities.”

2. Risk management – Converting threats into strategic advantages

Each identified risk became a competitive advantage narrative.

Technology evolution risks?

Claude positioned Nova’s “aggressive R&D investment strategy representing 12% of revenue” as proof they’re “innovation leaders rather than followers.”

3. CSR – Business strategy disguised as social responsibility

Claude opened with: “Nova AgriTech’s CSR initiatives represent strategic business development disguised as social responsibility.”

Every social program received a three-dimensional analysis: Business Strategy Integration, Community Impact, and Strategic Advantage.

4. Operational excellence – Metrics become competitive intelligence

Claude transformed a 15% energy reduction into evidence of “operational sophistication and cost leadership capabilities” while positioning technology absorption as “innovation capability and strategic independence.”

Human review and validation

“Let me verify legal compliance systematically,” Ms. Rao said, applying her professional review standards to Claude’s output.

She methodically checked each requirement while Arjun observed her process.

“Perfect legal compliance,” she concluded after her thorough review.

“Section 134(3)(c1) fraud disclosure clearly stated, risk management policy detailed with specific identification and mitigation strategies, CSR policy and implementation described with measurable impact metrics…”

She paused, reading through the response again.

“Though I have to say, this language might be too technical for smaller private companies. The strategic positioning and investment-grade terminology – while impressive – could be overwhelming for companies with simpler shareholder structures.”

“That is a good point,” Arjun replied.

“But in that case, you can always give a prompt to Claude to tone down the language to make it easier for shareholders to understand the board report with simple language. The beauty of AI collaboration is that you can adjust the complexity level based on your specific audience.”

Ms. Rao nodded thoughtfully. “So we could prompt Claude to use the same strategic framework but with more accessible language for family-owned businesses or smaller private companies?”

“Exactly. Something like ‘Please revise this using simpler language suitable for non-institutional shareholders while maintaining the strategic positioning,'” Arjun suggested.

“That is the flexibility I appreciate,” Ms. Rao said.

“This demonstrates that with proper philosophical context, AI can amplify sophisticated business judgment when properly guided, and then adapt that judgment to different audience needs. The key breakthrough is that our philosophical context strategy enabled Claude to think strategically rather than just organize legally.”

Key takeaways from AI-assisted risk and CSR disclosure writing in a board report

- Philosophical context documents help AI grasp how management thinks, not just what the business does.

- You can teach AI how to communicate strategy clearly by using simple, structured methods.

- Disclosures about risk or CSR can actually build a competitive edge if framed in a positive, strategic way.

- It is possible to follow legal rules while still crafting sharp, business-friendly messages, with the right prompts.

- Senior lawyers do not need to be tech experts—just using the right frameworks helps AI handle complex tasks well.

AI collaboration insights:

- You can use documents to guide AI, from basic facts all the way to deeper thinking.

- Doing some strategic thinking before drafting leads to much better results.

- Human input is still key—AI cannot replace professional judgment.

- Experts can get more out of AI by showing it how they think and plan.

Progress check: You have now seen how to handle the most philosophically complex board report content using AI. This strategic positioning foundation prepares you for Group 6’s final assembly, where we will integrate all components into a cohesive professional document.

Next steps

If you are following the series:

- Next: Part 7 covers Group 6 (Final Assembly and Compliance Verification)

- Previous: Part 5 covered Group 4 (External Stakeholders and Audit Relations)

If you are new to the series:

- Start from Part 1 for the complete methodology

- Jump to Part 8 to see the live demonstration

Want to try this yourself?

- Create philosophical context documents that capture management thinking

- Test AI’s understanding of communication psychology before requesting drafts

- Apply strategic optimism frameworks to transform compliance into competitive positioning

Complete article series

- Part 1: Getting Started

- Part 2: Building the foundation (Group 1)

- Part 3: Financial performance and capital management (Group 2)

- Part 4: Directors’ statements and professional judgment (Group 3)

- Part 5: External stakeholders and audit relations (Group 4)

- Part 6: Risk management and CSR disclosures (Group 5) ← You are here

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – complete board report creation

This strategic positioning foundation sets the stage for the final assembly communications covered in Part 7, where we will see how Claude integrates all components into a cohesive, professional board report that satisfies every stakeholder while positioning Nova AgriTech for continued success.

FREQUENTLY ASKED QUESTIONS

- What is the purpose of Group 5 disclosures under Section 134 of the Companies Act, 2013?

Group 5 disclosures cover risk management, CSR initiatives, energy and technology metrics, and deposits. Their purpose is to demonstrate management awareness of strategic risks and social responsibilities while complying with legal mandates. This article shows how these can be positioned as strengths rather than mere compliance items.

- How can AI tools like Claude help in drafting these disclosures?

AI tools can absorb philosophical context about a company’s risk appetite, CSR approach, and operational values. Once trained on such inputs, AI can generate sophisticated, investor-friendly board report drafts that reflect strategic thinking, mitigate liability exposure, and enhance business credibility.

- What makes Group 5 disclosures more challenging than previous sections of the board report?

Unlike prior groups that focus on factual data, Group 5 deals with subjective and strategic communication, like risk perception, corporate values, and public positioning. These require a careful balance between honesty and optimism, which AI can master if given the right prompting structure.

- What is a “philosophical context document,” and why is it important?

A philosophical context document outlines how management thinks—its values, strategic preferences, and communication principles. Feeding this to AI allows it to mirror the company’s tone and positioning in disclosures, turning basic reporting into persuasive, investment-grade messaging.

- Can AI-generated disclosures be adapted for smaller private companies or non-institutional shareholders?

Yes. AI outputs can be simplified by prompting the model to tone down the language for clarity and accessibility. For example, strategic frameworks can still be applied using plain English, making disclosures understandable to all shareholder types without sacrificing intent or compliance.

Allow notifications

Allow notifications