When dealing with insurance fraud or wrongful claim denials, a well-drafted consumer complaint can be more effective than costly civil litigation. This guide shows how AI can turn scattered facts and frustration into clear, structured complaints that cite IRDAI rules and consumer laws, helping lawyers, law students, and policyholders improve outcomes while keeping legal costs low.

Table of Contents

Introduction

Introduction

Last Tuesday, my colleague Naina burst into my office holding her phone like it was about to explode.

“You will not believe what just happened,” she said, “remember that life insurance claim rejection case I was struggling with? The one where the client’s wife died and the insurer is being difficult about the suicide clause?”

I nodded. Naina had been wrestling with that case for weeks, trying to draft a consumer complaint that would actually get the insurance company’s attention.

“Well, I just got off the phone with the client. He is thrilled. The insurer called him yesterday, offering to settle for 80% of the claim amount.”

“That is great news,” I said, genuinely happy for her. “What changed their mind?”

“That is the thing,” Naina grinned. “I used AI to draft the complaint. And it worked better than anything I have written in five years of practice.”

Now, I will be honest. When Naina first told me about using AI for legal drafting, I was sceptical. Like most lawyers, I had visions of robot-generated gibberish filled with made-up case citations. But the results spoke for themselves.

Here is the thing about consumer complaints: they are deceptively simple. You think you can just explain what happened, cite some consumer protection laws, and hope for the best. But insurance companies get hundreds of these complaints every month. Most are poorly written, missing key legal points, or so emotional that they read like angry letters to the editor.

“The problem,” Naina explained, “is that we lawyers either write complaints that are too technical, full of legal jargon that makes the client’s story disappear, or we write them too simply and miss the legal hooks that make insurers take notice.”

“Show me exactly what you did,” I said, pushing aside the brief I was working on. She pulled up her laptop. “Let me show you the conversation I had with Claude”.

Series recap and overview

In Part 5, we explored how to effectively utilise the Insurance Ombudsman system as a powerful, cost-free mechanism to compel insurance companies to honour their obligations and settle legitimate claims.

Before we proceed, here is what this comprehensive series encompasses:

Part 1: Fraud detection – Identify warning signs and behavioural indicators that expose insurance fraud before you fall victim.

Part 2: Legal strategy – Construct airtight cases, whether you are pursuing fraud charges or defending against false accusations.

Part 3: Understanding your rights – Master every legal avenue available when insurance companies wrongfully reject your claims.

Part 4: Strategic complaints – Craft correspondence that compels insurance companies to take immediate action and provide prompt responses.

Part 5: Ombudsman intervention – Harness this no-cost, influential mechanism to compel companies to honour their payment obligations.

Part 6: Consumer protection (Current article) – Secure not only your claim settlement but also substantial compensation for harassment, mental agony, and deficiency in service.

Part 7: Criminal action – Lodge police complaints that prosecutors will actively pursue in cases of fraud and deception.

Part 8: Constitutional safeguards – Seek High Court intervention when fundamental rights are breached or emergency relief is required.

Your complete roadmap to insurance justice awaits! Transform from a frustrated claimant into an empowered consumer who knows exactly how to make insurance companies accountable.

Through this article, I’ll reveal what could have spared Samuel months of legal uncertainty: how to leverage consumer courts not just for claim recovery, but for comprehensive justice, including compensation for harassment and mental agony.

How will you go about it?

A brief disclaimer before we begin:

While we used Claude AI for Arjun’s case due to its formal tone, understanding of Indian legal frameworks, and ability to organise complex narratives chronologically, this framework works well with ChatGPT, Bard, or other AI platforms. The prompts and responses shared here are carefully drafted examples based on patterns from hundreds of insurance disputes. Your actual results may vary depending on which AI platform you choose, the specific version you are using, how you phrase your prompts, and your case’s unique complexity. Consider these examples as templates rather than guaranteed outcomes; the framework is effective, but your skill in applying it will determine the quality of your draft.

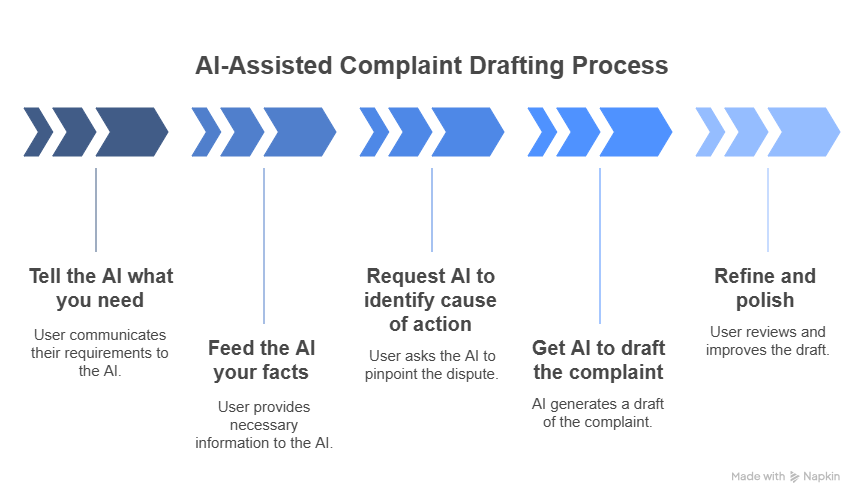

Step 1: Tell the AI what you need

“The first thing I learned,” Naina said, “is that you cannot just haphazardly feed information on AI and expect some great draft. You need to be specific about what you want.”

She showed me her opening prompt:

“I need to draft a consumer complaint against a life insurance company for wrongful claim rejection. The insurer is denying a death claim, citing the suicide clause, but I believe their application of this clause is incorrect. Please tell me what specific information you need to draft a strong complaint that addresses both the factual and legal issues.”

“See how I did not just say ‘write a complaint’?” Naina pointed out. “I told it exactly what kind of case it was and what I suspected the legal issue might be.”

The AI’s response was impressive:

“I’ll need comprehensive information to draft an effective consumer complaint. Here is what I need:

A. Case-Specific Facts:

1. Policyholder Information:

- What is the full name and age of the policyholder?

- What is the exact policy number and name of the insurance company?

- When was the policy purchased, and what is the sum assured?

- What is the complete premium payment history? Were all premiums paid on time, and if not, what were the delays?

2. Death Circumstances:

- What was the exact date and time of death?

- What was the official cause of death as stated in the death certificate?

- What were the specific circumstances surrounding the death? Where was the deceased found, by whom, and what immediate steps were taken?

- What medical records and reports are available, including autopsy or post-mortem findings?

3. Claim Process:

- When exactly was the claim first intimated to the insurance company?

- What is the complete timeline of document submission? What documents were submitted and when?

- What acknowledgements or receipts were provided by the insurer for the claim and documents?

- How long did the insurer take to process and respond to the claim?

4. Rejection Details:

- What exact reason did the insurer provide for rejecting the claim?

- Which specific policy clause or legal provision did they cite in their rejection?

- Did they provide any evidence or an investigation report to support their decision?

- What was the exact wording used in the rejection letter?

5. Policy Terms:

- What are the exact terms of the suicide clause in the policy?

- What is the waiting period specified for suicide coverage?

- Are there any other exclusions or conditions that might be relevant to this case?

- What does the policy say about the insurer’s investigation rights and procedures?

B. Legal Context:

1. Policy Validity Period:

- How many years, months, and days was the policy in force before the death occurred?

- Was there any lapse in premium payments that might have affected the policy’s validity?

2. Suicide Clause Applicability:

- Has the suicide clause waiting period (typically 1-2 years) been completed before the death?

- If the waiting period has expired, what does the law say about suicide coverage after this period?

3. Evidence of Intent:

- What evidence, if any, supports the theory that the death was intentional suicide?

- What evidence contradicts the suicide theory? Was there a suicide note, previous attempts, or documented depression?

- What do the medical records and treating doctors say about the deceased’s mental state?

4. Medical History:

- Did the deceased have any pre-existing medical conditions, particularly mental health issues?

- What medications was the deceased taking, and were they properly prescribed?

- Is there any documented history of suicidal ideation or attempts?

5. Investigation Standards:

- Did the insurer follow proper investigation procedures as mandated by IRDAI guidelines?

- What investigation methodology did they use, and was it transparent?

- Did they interview relevant parties like family members, doctors, or witnesses?

C. Procedural Issues:

1. Communication Timeline:

- What is the complete timeline of all communications between the policyholder and the insurer?

- How long did each interaction take, and what was discussed or requested?

- Are there any written records of phone calls, emails, or meetings?

2. Processing Delays:

- How long did the insurer take to acknowledge the claim, request documents, and provide a final decision?

- Did these timelines comply with IRDAI guidelines for claim processing?

- What reasons, if any, did the insurer provide for any delays?

3. Grievance Redressal:

- Was a formal grievance filed with the insurer after the claim rejection?

- How long has it been since the grievance was filed, and what response has been received?

- Were the insurer’s grievance redressal procedures followed properly?

4. Unfair Practices:

- Is there documentation of any unfair practices by the insurer, such as asking for unreasonable documents or information?

- Did the insurer act in bad faith by making decisions without adequate evidence?

- Were there any instances of harassment, delayed responses, or unprofessional behaviour?

- Did the insurer provide clear, specific reasons for their decisions, or were their communications vague and evasive?

Please provide these details so I can identify the strongest legal arguments and draft a complaint that addresses both Consumer Protection Act violations and insurance law issues.”

“That is when I realised,” Naina said, “that AI is not just a writing tool. It is like having a senior lawyer review your case strategy before you even start drafting.”

Step 2: Feed the AI your facts

Naina’s second prompt was lengthy:

Here is a detailed response to those queries for the life insurance case:

A. Case-Specific Facts:

1. Policyholder Information:

- Full name and age: Arjun Malhotra, age 45 years, working as a Senior Software Engineer at Tech Solutions Pvt. Ltd.

- Policy details: Policy Number LS-789456 with LifeSecure Insurance Company Limited, purchased on January 15, 2020

- Sum assured: Rs. 50 lakhs (Term Life Insurance with 20-year term)

- Premium payment history: All premiums paid punctually through auto-debit from the HDFC Bank account ending 4567. Annual premium of Rs. 28,500 paid on time every January 15th from 2020 to 2024. No defaults, lapses, or delayed payments.

2. Death Circumstances:

- Date and time: September 15, 2024, approximately 11:30 PM

- Official cause of death: “Acute respiratory depression due to Zolpidem overdose” as per the death certificate issued by KEM Hospital, Mumbai

- Circumstances: Priya Malhotra (deceased) was found unconscious in her bedroom by her husband, Arjun, at 11:30 PM. He immediately called the 108 ambulance service and rushed her to KEM Hospital, where she was declared dead on arrival at 12:15 AM on September 16, 2024.

- Medical records: Post-mortem report shows therapeutic levels of Zolpidem in blood (not lethal overdose levels). No signs of physical trauma. Coroner’s report states, “circumstances of death inconclusive regarding intent, could be accidental or intentional.”

3. Claim Process:

- Claim intimation: October 2, 2024, through online portal and confirmed via email (Reference: CLM/2024/789456)

- Document submission timeline:

i. October 10, 2024: Death certificate, policy documents, and claim forms submitted

ii. October 15, 2024: Medical records and post-mortem report submitted

iii. October 20, 2024: Police panchnama and hospital records submitted

- Acknowledgements: Email acknowledgement received for each submission with reference numbers

- Processing time: 90 days from claim intimation to rejection (October 2 2024, to January 8 2025)

4. Rejection Details:

- Rejection reason: “Claim denied under Policy Clause 8.2 (Suicide Exclusion) and Section 45 of the Insurance Act. Our investigation concludes that the death was the result of intentional self-harm.”

- Specific clause cited: Policy Clause 8.2 and Section 45 of the Insurance Act, 1938

- Evidence provided: None. Investigation report not shared despite multiple requests

- Exact wording: “After thorough investigation, we have concluded that the death of the life assured appears to be intentional self-harm; hence, the claim is repudiated under the suicide exclusion clause.”

5. Policy Terms:

- Suicide clause: “No benefit shall be payable if the life assured commits suicide within 2 years from the date of commencement of the policy”

- Waiting period: 2 years from policy commencement (completed January 15, 2022)

- Other exclusions: War, nuclear risks, criminal acts, none applicable to this case

- Investigation clause: “Company reserves the right to investigate claims and may require additional documents as deemed necessary”

B. Legal Context:

1. Policy Validity Period:

- Duration: 4 years, 8 months, and 1 day (from January 15, 2020, to September 15, 2024)

- Premium status: No lapses. All premiums are paid on due dates, with auto-debit confirmations available

2. Suicide Clause Applicability:

- Waiting period completion: Yes, completed on January 15, 2022 (2 years from policy start)

- Legal position: As per Section 45 of the Insurance Act, 1938, after 2 years, even suicide is covered unless proven with conclusive evidence

3. Evidence of Intent:

- Supporting suicide theory: None provided by insurer

- Contradicting suicide theory:

i. No suicide note found

ii. No history of depression or mental health treatment

iii. Recent positive life events (booked family vacation to Goa for October 2024)

iv. Active participation in children’s school activities

v. Blood levels showed a therapeutic dose, not a lethal overdose

vi. No previous suicide attempts or ideation documented

4. Medical History:

- Pre-existing conditions: Chronic insomnia diagnosed in March 2022, mild anxiety disorder

- Current medications: Zolpidem 5mg prescribed by Dr. Kavita Sharma (Psychiatrist) for sleep disorder, taken for 2+ years

- Mental health status: No documented depression, suicidal ideation, or psychiatric hospitalisation

- Treating doctor’s opinion: Dr. Sharma’s records show the patient was stable, medication was working well, and no suicidal thoughts were expressed

5. Investigation Standards:

- IRDAI compliance: No evidence of following IRDAI guidelines for claim investigation

- Investigation methodology: Not disclosed despite requests

- Interviews conducted: No interviews with family, treating doctors, or friends

- Evidence gathering: No visit to the scene, no review of medical history with treating physicians

C. Procedural Issues:

1. Communication Timeline:

- October 2, 2024: Claim intimated online, acknowledgement received

- October 10, 2024: Documents submitted, receipt confirmed

- November 15, 2024: Follow-up call made, told “investigation in progress”

- December 5, 2024: Email sent requesting status update, no response

- December 20, 2024: Another email sent, no response

- January 8, 2025: Rejection letter received via email and post

2. Processing Delays:

- Timeline violation: 90 days taken vs. IRDAI mandated 30 days for life insurance claims

- Compliance breach: No interim communication about the investigation progress

- Reason for delay: None provided by insurer

- Impact: The family faced financial hardship during the extended waiting period

3. Grievance Redressal:

- Grievance filed: January 15, 2025, through the company’s grievance portal (Reference: GRV/2025/156789)

- Response timeline: 50+ days elapsed with no response (as of March 6, 2025)

- Company obligation: Should respond within 30 days as per IRDAI guidelines

- Approached the Insurance Ombudsman, but the claim was rejected without being given a fair opportunity to present my case.

4. Unfair Practices:

- Lack of transparency: Refusing to share the investigation report or methodology

- The burden of proof violation: Making a suicide allegation without providing evidence

- Procedural violations: Exceeding claim processing timelines without justification

- Bad faith behaviour:

i. Rejecting a claim without adequate investigation

ii. Ignoring grievance for 50+ days

iii. Not responding to legitimate queries about the investigation

iv. Applying suicide exclusion despite waiting period completion

v. Harassment through prolonged, unjustified claim processing

Additional Supporting Evidence:

- Bank statements showing regular premium payments

- Email trail of all communications with the insurer

- Medical certificates from the treating doctor

- Family testimonials about the deceased’s mental state

- Recent positive activities (vacation booking, school events attendance)

Step 3: Request the AI to identify and highlight the cause of action/point of dispute

“AI can do case analysis?” I asked, surprised. “Better than most juniors,” Naina smiled, “I just gave it this prompt.”

Prompt:

“Based on the legal and factual information I have provided, please identify the key legal issues and possible causes of action in this case. Highlight any statutory violations, contractual breaches, or procedural lapses that may be relevant.”

Response:

Based on the comprehensive factual and legal information provided, here’s my analysis of the key legal issues and causes of action:

A. PRIMARY LEGAL ISSUES IDENTIFIED:

1. Misapplication of the Suicide Exclusion Clause

- Legal Issue: Insurance company wrongly applied suicide exclusion after the 2-year contestability period had expired

- Statutory Basis: Section 45 of the Insurance Act, 1938 – after 2 years, the policy cannot be called into question except for fraud

- Contractual Analysis: Policy clearly states suicide exclusion applies only within the first 2 years; this limitation expired on January 15, 2022

2. Burden of Proof Violation

- Legal Issue: Insurer failed to prove suicide “beyond a reasonable doubt” as required by law

- Case Law Basis: Multiple Supreme Court judgments establish that the insurer must prove suicide conclusively, not merely show the possibility

- Evidence Gap: No evidence provided by the insurer to support the suicide theory

B. STATUTORY VIOLATIONS:

I. IRDAI Regulations:

- Claim Settlement Timeline Violation

- Regulation: Claims must be settled within 30 days

- Violation: 90 days taken without justification

- Penalty: Interest liability and regulatory action

- Investigation Standards Breach

- Regulation: Transparent investigation methodology required

- Violation: No investigation report shared, methodology not disclosed

- Impact: Denial of due process to the policyholder

- Grievance Redressal Failure

- Regulation: 30-day response timeline for grievances

- Violation: 50+ days elapsed without a response

- Consequence: Direct grounds for Ombudsman complaint

II. Consumer Protection Act 2019:

- Deficiency in Service (Section 2(11))

- Delayed claim processing

- Inadequate investigation

- Non-responsive grievance handling

- Unfair Trade Practice (Section 2(47))

- Making false allegations without evidence

- Applying expired exclusion clauses

- Misleading claim rejection reasoning

C. CONTRACTUAL BREACHES:

1. Good Faith Obligation

- Principle: Insurance contracts require utmost good faith from both parties

- Breach: Insurer acting in bad faith by rejecting the claim without adequate evidence

- Impact: Fundamental breach of insurance contract principles

2. Investigation Clause Misuse

- Contract Term: Right to investigate claims

- Breach: Using the investigation right to delay rather than determine facts

- Consequence: Procedural abuse of contractual rights

3. Claims Settlement Obligation

- Primary Obligation: Duty to settle legitimate claims promptly

- Breach: Wrongful denial of a valid claim

- Remedy: Claim settlement plus damages

D. PROCEDURAL LAPSES:

1. Due Process Violations

- Failed to provide investigation findings

- No opportunity given to respond to adverse conclusions

- Lack of transparency in the decision-making process

2. Communication Failures

- Ignored multiple follow-up communications

- Failed to provide status updates during the investigation

- Non-compliance with grievance response timelines

3. Evidence Standard Violations

- Made conclusive determinations without adequate evidence

- Failed to interview key witnesses (family, doctors)

- Ignored contradictory evidence

D. POSSIBLE CAUSES OF ACTION IDENTIFIED:

1. Under the Consumer Protection Act, 2019:

- Deficiency in Service – 90-day claim processing delay, inadequate investigation, non-responsive grievance handling

- Unfair Trade Practice – Making false suicide allegations without evidence, applying expired exclusion clauses, and misleading claim rejection reasoning

2. Under the Insurance Act, 1938:

- Violation of Section 45 – Wrongful application of suicide exclusion after the 2-year contestability period expired

- Breach of Investigation Standards – Failure to conduct a transparent investigation and provide findings

3. Under Contract Law:

- Breach of Insurance Contract – Wrongful denial of valid claim, violation of good faith obligations

- Procedural Breach – Misuse of the investigation clause to delay rather than determine facts

4. Under IRDAI Regulations:

- Claim Settlement Timeline Violation – Exceeding 30-day statutory timeline without justification

- Grievance Redressal Failure – Non-compliance with the 30-day response requirement for grievances

- Investigation Process Violation – Failure to follow prescribed investigation methodology and transparency standards

E. CRITICAL GAPS AND AMBIGUITIES:

1. Medical Evidence Gaps

- Missing: Detailed toxicology report showing exact blood levels

- Needed: Expert medical opinion on accidental vs. intentional overdose

2. Timeline Ambiguities

- Unclear: Exact sequence of events on the night of death

- Needed: A more precise timeline from evening to discovery

3. Medication History

- Incomplete: Full prescription history and dosage changes

- Needed: Complete medical records from the treating psychiatrist

4. Investigation Details

- Missing: Insurer’s investigation methodology and findings

- Status: Requested but not provided

This analysis provides a comprehensive legal framework for pursuing the case through multiple available remedies.

“That analysis alone,” Naina said, “was worth more than what I could get from most junior lawyers. It organised the facts, identified the legal issues, and gave me a strategy.”

Step 4: Get AI to draft the complaint

“Now comes the actual drafting,” Naina explained. “But instead of asking for a generic complaint, I was specific about what I wanted.”

AI prompt:

“Using the facts and legal analysis above, draft a consumer complaint with these specific elements:

- Facts to be stated chronologically that emphasise the insurer’s procedural failures

- Legal arguments that focus on the burden of proof and IRDAI violations

- Specific relief sought, including compensation for harassment

- The professional tone is firm but not emotional

Structure it as a formal complaint to the District Consumer Commission with proper headings and citations to the Consumer Protection Act 2019.”

The AI generated a genuinely impressive complaint. You can click here to take a look.

Step 5: Refine and polish

“The first draft was good, but it needed refinement,” Naina continued. “This is where the conversation with AI became really valuable.”

Her follow-up prompt:

“The draft is strong, but I want it to flow like a story. Averments should show how the insurer violates the law (wherever required). Make a few adjustments:

- Emphasise more strongly that the 2-year suicide clause period had expired

- Add a section about the insurer’s failure to follow IRDAI guidelines on claim investigation

- The cause of action must be highlighted in the averment itself and not separately

- Once you are done stating the facts, make the following averments:

- The complaint further declares that the matter regarding which this complaint has been made is not pending before any court of law or any other authority or any other tribunal(s).

- The prescribed court fee of Rs. 5000/- has been paid through UPI (Transaction ID No. 1234567) dated 6th March 2025. “

AI’s response (along with some manual edits)

BEFORE THE DISTRICT CONSUMER DISPUTES REDRESSAL COMMISSION

MUMBAI

CONSUMER COMPLAINT NO. ________ of 2025

IN THE MATTER OF:

ARJUN MALHOTRAAge: 45 years Having his address at Flat 301, Tech Heights,

Occupation: Senior Software Engineer

Andheri East, Mumbai – 400069

Contact: +91-9876543210

Email: [email protected]

… COMPLAINANT

VERSUS

LIFESECURE INSURANCE COMPANY LIMITED

Registered Office: LifeSecure Tower,

Bandra Kurla Complex, Mumbai – 400051

Branch Office: Ground Floor, Commercial Plaza,

Andheri East, Mumbai – 400069

… OPPOSITE PARTY

The Complainant most respectfully submits as follows:

- On January 15, 2020, I, Arjun Malhotra, purchased a Term Life Insurance Policy bearing number LS-789456 from LifeSecure Insurance Company Limited for a sum assured of Rs. 50 lakhs with a 20-year term. This policy was specifically purchased to secure my family’s financial future and my children’s education. A copy of the policy document is hereto annexed and marked as Exhibit A-1.

- Throughout the policy period, I have been

a model policyholder,paying the annual premium of Rs. 28,500 punctually every January 15th through auto-debit from my HDFC Bank account ending 4567. There have been no defaults, lapses, or delayed payments whatsoever. A copy of premium payment receipts is hereto annexed and marked as Exhibit A-2. - On

the fateful night of - I immediately called the 108 ambulance service and rushed her to the KEM Hospital, Mumbai. Despite all efforts, she was declared dead on arrival at 12:15 AM on September 16, 2024. A copy of the death certificate and hospital records is hereto annexed and marked as Exhibit B-1 and B-2, respectively.

- The official cause of death, as certified by KEM Hospital, was “Acute respiratory depression due to Zolpidem overdose.” However, what is crucial to note is that the post-mortem report revealed only therapeutic levels of Zolpidem in her blood, not lethal overdose levels. The coroner’s report specifically states that the “circumstances of death are inconclusive regarding intent, could be accidental or intentional.”

- Further, there were no signs of physical trauma, no suicide note was found, and Priya had no documented history of depression, suicidal ideation, or psychiatric hospitalisation. A copy of the postmortem report and coroner’s report is hereto annexed and marked as Exhibit B-3 and B-4, respectively.

- It is crucial to mention that far from showing any signs of suicidal intent, Priya was actively engaged in life and future planning. Just weeks before her death, we had booked a family vacation. She was actively participating in our children’s school activities and was scheduled to attend a parent-teacher meeting the week following her death.

- Dr. Kavita Sharma’s medical records consistently show that Priya was stable on her medication, which was working well. She had never expressed any suicidal thoughts during her treatment spanning over two years. A copy of Dr. Sharma’s Medical Records is hereto annexed and marked as Exhibit B-5.

- Being fully aware of my obligations under the policy, the Complainant intimated the claim to LifeSecure Insurance Company on October 2, 2024, through their online portal. The Complainant received an email confirmation with reference number CLM/2024/789456.

- The Complainant meticulously submitted all required documents

in a phased manner: on October 10, 2024, I submittedthe death certificate, policy documents, completed claim forms, medical records and the post-mortem report, the police panchnama and hospital records. Each submission was acknowledged by the Opposite Party with reference numbers, demonstrating their receipt of comprehensive documentation. A copy of the Claim Intimation Acknowledgement and Document Submission Receipts is hereto annexed and marked as Exhibit C-1 and C-2, respectively. - Despite receiving all necessary documents by October 20, 2024, the Opposite Party embarked on a deliberate course of delay and obfuscation. It is a matter of law that life insurance claims must be settled within 30 days of receipt of all required documents, failing which the insurer becomes liable to pay interest. However, LifeSecure Insurance took an unconscionable 90 days to process my claim.

- This delay

of 200%in violation ofbeyond the - On January 8, 2025, after this prolonged and unjustified delay, the Complainant received a rejection letter from LifeSecure Insurance. The rejection was based on the specious ground that the claim was “denied under Policy Clause 8.2 (Suicide Exclusion)” with the conclusion that “the death was the result of intentional self-harm.” A copy of the claim rejection letter is hereto annexed and marked as Exhibit D-3.

- The policy contained a standard suicide exclusion clause stating: “No benefit shall be payable if the life assured commits suicide within 2 years from the date of commencement of the policy.” This waiting period of two years was completed on January 15, 2022, nearly three years before Priya’s death on September 15, 2024.

This means that even if death were by suicide (which it was not), the claim would still be payable after the two-year period. - The Opposite Party’s reliance on the suicide exclusion clause after this period constitutes a gross violation of contractual terms and

statutory law,and amounts to unfair trade practice. Their conduct demonstrates complete disregard for established legal principles and policyholder rights. - This rejection constitutes multiple violations: firstly, a blatant misapplication of statutory law, as the suicide exclusion period had expired nearly three years prior. Secondly, deficiency in service

due to the 200% delaybeyond statutory timelines. Thirdly, unfair trade practices by making false allegations without evidence. - The Opposite Party’s conduct demonstrates a systematic breach of their contractual and statutory obligations designed to wrongfully deny a legitimate claim.

- What makes the Opposite Party’s conduct particularly egregious is its systematic violation of mandatory procedures for claim investigations. Despite claiming to have conducted a “thorough investigation,” they have completely failed to follow prescribed investigation protocols. Insurers are required to conduct transparent investigations, maintain proper documentation, and share findings with policyholders upon request. However, the Opposite Party has refused to share their investigation report or methodology with me, despite multiple requests. This constitutes a clear violation of regulatory transparency requirements and amounts to a deficiency in service.

- The guidelines further mandate that claims investigations must include interviews with relevant parties, examination of medical records with treating physicians, and proper evidence gathering. In this case, no interviews were conducted with me as the surviving spouse, with our treating doctor, Dr. Kavita Sharma, or with any family members or friends who could attest to Priya’s mental state.

- There was no visit to our residence, no review of medical history with treating physicians, and no transparent investigation process whatsoever. This failure to follow mandatory investigation procedures violates regulatory guidelines and constitutes a gross deficiency in service.

- Moreover, if an insurer concludes that a death was by suicide, it must provide conclusive evidence to support such a finding, especially after the two-year contestability period. The Opposite Party has provided no evidence whatsoever to support their suicide conclusion, making their rejection not only procedurally flawed but legally untenable. This conduct amounts to unfair trade practice as it involves making false allegations to avoid legitimate claim settlement. A copy of the requests for investigation report is hereto annexed and marked as Exhibit D-4.

- Following the wrongful rejection, the Complainant filed a formal grievance with LifeSecure Insurance on January 15, 2025, through their company’s grievance portal (Reference: GRV/2025/156789). Insurance companies must respond to grievances within 30 days, failing which it constitutes a deficiency in service. However, the Opposite Party completely failed to respond to my grievance.

- This demonstrates continued non-compliance with regulatory requirements and constitutes further deficiency in service. A copy of the grievance filing acknowledgement and a copy of the grievance complaint are hereto annexed and marked as E-1 and E-2.

- Having exhausted the grievance mechanism with the insurer without any response, the Complainant was compelled to approach the Insurance Ombudsman, Mumbai, on February 20, 2025. The Complainant sought redressal of his legitimate grievances through this regulatory mechanism.

- However, to the Complainant’s utter dismay, the Insurance Ombudsman’s office rejected my complaint on March 1, 2025, without providing me a fair opportunity to present my case. The Ombudsman’s rejection was cursory and failed to consider the substantial evidence that the Complainant had submitted or the clear violations of statutory provisions by the insurance company. This denial of natural justice and failure to properly adjudicate my complaint, coupled with the systematic failures of both the insurer and the regulatory mechanism, has left me with no alternative. The Opposite Party’s conduct clearly falls within the purview of unfair trade practices and deficiency in service. A copy of the complaint to the insurance ombudsman and the rejection order are hereto annexed and marked as Exhibit E-1 and E-2, respectively.

- In view of the facts stated above and the multiple violations committed by the Opposite Party, the Complainant most respectfully prays that this Hon’ble Commission may be pleased to:

- Direct the Opposite Party to settle the life insurance claim of Rs. 50,00,000 (Fifty Lakhs Only) within 30 days from the date of receipt of this order.

30 days of this order. - Award interest at the rate of 12% per annum on the claim amount from October 2, 2024 (date of claim intimation) till the date of actual payment.

- Award compensation of Rs. 5,00,000 (Five Lakhs Only) for mental agony, harassment, and deficiency in service caused by the Opposite Party’s wrongful conduct.

- Award litigation costs of Rs. 1,00,000 (One Lakh Only) for the

unnecessary Direct the Opposite Party to issue a written apology for their unfair trade practices and service deficiencies.- Pass any other order or direction that this Hon’ble Commission deems fit and proper in the circumstances of the case.

- The Complainant further declares that the matter regarding which this complaint has been made is not pending before any court of law, any other authority or any other tribunal(s).

- The prescribed court fee of Rs. 5,000/- has been paid through UPI (Transaction ID No. 1234567890) dated 6th March 2025.

- Based on the above facts and circumstances, it is evident that the Opposite Party has committed multiple violations of statutory provisions and regulatory guidelines, warranting intervention by this Hon’ble Consumer Commission to ensure justice and prevent such unfair practices in the future.

VERIFICATION

I, Arjun Malhotra, the Complainant above named, do hereby verify that the contents of the above complaint are true and correct to the best of my knowledge and belief and that no part of it is false and nothing material has been concealed therefrom.

Place: Mumbai

Date: March 6, 2025

Complainant

Arjun Malhotra

Final thoughts

This approach makes a lot of sense. The key insight is using AI as a sophisticated drafting tool rather than trying to replace legal judgment entirely.

What is particularly smart about Naina’s method is the division of labour, let AI handle the structural work, research organisation, and initial drafting, then apply human expertise for strategy, fact verification, and client-specific nuances.

The insurance company’s response validates this approach. They recognised the quality difference because most complaints they see are either overly emotional or too generic. A well-structured, legally precise complaint signals that the opposing counsel is serious and prepared.

The efficiency gains are significant, too. Instead of billing clients for hours of basic drafting work, lawyers can focus their time on higher-value activities like case strategy and client counselling.

This is not about AI replacing lawyers; it is about lawyers using AI to deliver better work more efficiently. The client gets a stronger complaint at a lower cost, and the lawyer can focus on what they do best: legal strategy and advocacy.

Frequently asked questions

- Can AI draft complaints better than junior lawyers?

AI excels at organising facts, identifying legal issues, and maintaining a consistent professional tone throughout lengthy documents. However, it can’t verify facts, understand local nuances, or make strategic decisions about emphasis. Think of it as a brilliant research assistant that never gets tired, but still needs experienced supervision.

- What if AI generates incorrect legal citations or makes up case law?

This is exactly why human oversight is crucial. Always verify any legal citations AI provides and never submit anything without a thorough review. The approach works best when you use AI for organisation and structure, then add your own legal knowledge and verify all references independently.

- Is this approach cost-effective for small law firms and solo practitioners?

Absolutely. Instead of spending billable hours on basic structural work and initial drafting, you can focus on strategy, client relations, and case-specific analysis. Your clients get professionally drafted complaints faster and at lower cost, while you can handle more cases efficiently.

- Will this eventually replace the need for legal education and experience?

Not at all. AI amplifies legal expertise but cannot replace it. You still need to understand the law, develop a case strategy, verify facts, and make judgment calls about what to emphasise. The technology makes experienced lawyers more efficient, but it can’t substitute for legal knowledge and professional judgment.

Allow notifications

Allow notifications

Thanks for sharing this useful blog with productive information.