Learn how to use AI tools like Claude to draft legally compliant board report disclosures under section 134 of the Companies Act, 2013. This article shows how to automate and customise directors’ responsibility statements, performance evaluations, and independent declarations, while ensuring statutory language is preserved and liability risks are managed. Perfect for in-house legal teams and compliance professionals.

About this series

This is Part 4 of our 8-part series on using AI to draft board reports under the Companies Act 2013.

Complete series overview:

- Part 1: Getting Started

- Part 2: Building the foundation (Group 1)

- Part 3: Financial performance and capital management (Group 2)

- Part 4: Directors’ statements and professional judgment (Group 3) ← You are here

- Part 5: External stakeholders and audit relations (Group 4)

- Part 6: Risk management and CSR disclosures (Group 5)

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – real-time board report creation

Haven’t started from Part 1? No problem! This article works independently, but you will gain more value by reading the series in sequence.

What you will learn in this article: When directors sign responsibility statements, each word can create personal legal risk. In today’s session, Arjun and Ms. Rao tackle the legally sensitive part of board reports – statements that directors personally sign and take responsibility for. You will see how they balance legal protection with professional communication.

Key Characters:

- Arjun Sharma: Junior lawyer learning AI tools for legal work

- Ms. Priya Rao: Senior partner, now contributing actively and sharing expertise

- Nova AgriTech: Agri-tech client needing professional judgment disclosures that directors will personally certify

Quick recap: where we are

[For series readers: Skip to “Today’s Focus” below] [For new readers: Here’s what happened so far]

Previously, Ms. Rao was initially sceptical about using AI for legal work. Arjun demonstrated Claude’s understanding of legal requirements and systematic organisation. They successfully created professional Group 1 governance content and sophisticated Group 2 financial analysis that impressed Ms. Rao with investment-grade quality.

The step-by-step approach we use:

- Upload comprehensive company information (so Claude understands the business)

- Test Claude’s understanding (before asking it to draft anything)

- Improve drafts step by step (refine content through focused prompts)

- Review everything carefully (lawyer oversight ensures accuracy)

Groups completed:

- Group 1: Foundational Structure & Governance

- Group 2: Financial Performance & Capital Management

- Group 3: Board Responsibilities & Performance ← Today’s focus

- Remaining groups: 4-6 to be covered in subsequent parts

Nova AgriTech quick profile:

- Strong governance foundation established in Group 1

- Impressive financial performance documented in Group 2

- A board of 5 directors who must personally certify their responsibilities

Today’s focus: Group 3 – Board responsibilities & performance

In this article, you will watch Arjun and Ms. Rao handle the most sensitive legal content – statements that directors personally sign and become liable for.

This requires a different approach than previous groups have taken.

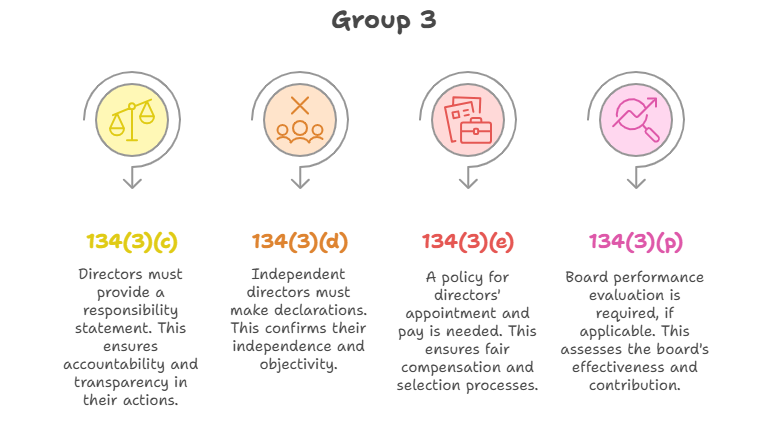

Group 3 requirements we are covering:

- Section 134(3)(c): Directors’ Responsibility Statement

- Section 134(3)(d): Independent director declarations

- Section 134(3)(e): Directors’ appointment and remuneration policy

- Section 134(3)(p): Board performance evaluation (if applicable)

By the end, you will understand:

- How to handle exact mandatory legal language requirements

- Techniques for customising standard statements to specific companies

- The critical importance of human review for liability protection

Tackling the communication strategy for group 3 disclosures in the board report: a different kind of challenge

“Alright, Groups 1 and 2 are done. What do you think about Group 3, Arjun?” Ms. Rao asked, reviewing their completed governance and financial sections.

“Group 3 involves a different tone entirely,” Arjun replied, pulling out section 134(5) from the Companies Act.

“This is not about strategic communication anymore. When directors sign the Directors’ Responsibility Statement, they are personally certifying internal controls, accounting estimates, and legal compliance. Every word carries potential liability.”

Ms. Rao leaned forward, studying the section. “So, how do we handle that with Claude?”

“We need Claude to use the exact mandatory language required by law, but we can customise the specific details to make it relevant to Nova’s actual circumstances,” Arjun explained.

“The Directors’ Responsibility Statement has six mandatory points under section 134(5). We cannot change those core requirements, but we can reflect Nova’s actual operations within them.”

“What about the other Group 3 requirements?” Ms. Rao asked.

“The board performance evaluation and remuneration policy need to demonstrate genuine oversight without revealing competitive information,” Arjun continued.

“It is about being transparent enough for institutional investors while protecting Nova’s strategic details. The key is showing real governance without giving away too much.”

Ms. Rao nodded thoughtfully.

“That does sound like a delicate balance. How do we give Claude the right context for this?”

Uploading group 3 disclosure strategy to Claude

The same way as we did it for Groups 1 and 2, i.e., by uploading the document,” Arjun said, opening a new document.

“We are going to upload the relevant information so that Claude is able to understand Nova’s governance practices, board evaluation methods, and the specific details that make the mandatory statements accurate.”

Ms. Rao nodded.

“The Directors’ responsibility statement must reflect Nova’s actual accounting practices, control systems, and compliance procedures. Generic language will not work for sophisticated institutional investors.”

Arjun began creating Nova’s governance intelligence document:

Nova AgriTech Group 3 governance document

Directors’ responsibility context:

- Accounting standards: Ind AS applicable for company size and nature

- Internal controls: CFO-certified financial reporting controls implemented

- Control assessment: Quarterly review process with independent verification

- Going concern: Strong financial position with 18-month cash runway

- Law compliance: Legal department tracks 23 applicable regulations

- Risk management: Board-level risk committee established Q3 FY 2024-25

Independent directors’ status:

- Dr. Priya Sharma: Agricultural scientist, no material relationships with the company

- Mr. Rajesh Kumar: Technology investor, independent per section 149(6) criteria

- Annual declarations: Both provided independence confirmations in March 2025

- Board reliance: Strategic guidance on agricultural applications and technology scaling

Board performance and remuneration:

- Evaluation method: Annual self-assessment questionnaire plus peer feedback

- Performance criteria: Strategic guidance effectiveness, oversight quality, stakeholder value creation

- Remuneration philosophy: Fixed sitting fees plus performance-linked annual retainer

- Policy disclosure: Transparent criteria for appointment based on expertise and independence

Professional governance standards:

- Meeting preparation: Board packs distributed 72 hours prior to meetings

- Decision documentation: Detailed minutes with rationale for major decisions

- Stakeholder communication: Quarterly updates to institutional investors

- Regulatory compliance: Proactive engagement with regulatory changes

Ms. Rao reviewed the group 3 governance document.

“This gives Claude the specific details needed to customise mandatory statements authentically. It is not just about Nova’s numbers anymore – it is about how Nova actually operates.”

“Exactly. Now Claude can customise the Directors’ Responsibility Statement to reflect Nova’s actual control environment rather than using generic language,” Arjun agreed.

Can AI understand governance narrative in a board report?

Following their step-by-step approach, Arjun uploaded the group 3 governance document and began with the most critical requirement:

First prompt:

Based on the Nova AgriTech group 3 governance document uploaded, analyse the Group 3 requirements for their FY 2024-25 board report:

Section 134(3)(c) Directors’ Responsibility Statement,

Section 134(3)(d) Independent Directors’ Declarations,

Section 134(3)(e) Directors’ Appointment and Remuneration Policy, and

Section 134(3)(p) Board Performance Evaluation.

Explain how these four requirements create comprehensive governance accountability for Nova AgriTech’s institutional investors.

Click here to see the complete conversation and here to see claude’s response in PDF.

Claude’s response was immediately impressive. Claude’s analysis positioned Nova’s governance framework as an “interconnected accountability ecosystem” that directly serves institutional investor interests.

Ms. Rao was particularly impressed by how Claude positioned Independent Directors’ Declarations within Nova’s investment context, explaining why independent oversight becomes crucial for institutional investors evaluating going concern assessments and reserves management.

“This is not just compliance analysis,” she observed, scrolling through the comprehensive response. “Claude actually understood how these governance requirements work together to create investor confidence.”

“The business-focused legal analysis is exactly what we needed,” Arjun agreed.

“Instead of treating each requirement as a separate checkbox, Claude showed how they create a comprehensive governance story that speaks to institutional investors.”

“Now let us get the actual mandatory language requirements,” Arjun said, moving to the most critical element.

Getting the board report content right

Second prompt:

Based on Nova AgriTech documents, draft group 3 disclosures for their board report:

(1) Independent directors’ declarations under section 134(3)(d),

(2) Director’s responsibility statement under section 134(3)(c),

(3) Directors’ appointment and remuneration policy disclosure under section 134(3)(e), and (4) Board performance evaluation under section 134(3)(p).

Keep each disclosure concise and focused on Nova’s specific circumstances.

Click here to see the complete conversation and here to see claude’s response in PDF.

Claude delivered well-structured disclosures for all four requirements. But as Ms. Rao read through the Directors’ Responsibility Statement, she caught a critical issue.

“Wait a minute,” she said, frowning at the screen.

“The Directors’ Responsibility Statement looks professional, but it is missing something crucial.”

She pulled up section 134(5) of the Companies Act.

“Look at this, section 134(5) mandates that directors must use specific language – six exact points labelled (a) through (f). Claude wrote good content about Nova’s controls and compliance, but where are the mandatory statutory phrases?”

Arjun leaned over to see what she meant.

“You are absolutely right. Section 134(5) does not give us flexibility with the language. Directors have to certify using the exact words the law requires.”

“Exactly,” Ms. Rao continued.

“Claude gave us a narrative about Nova’s accounting practices and internal controls, but directors need to state: ‘in the preparation of the annual accounts, the applicable accounting standards had been followed along with proper explanation relating to material departures’ – that’s the mandatory language.”

“So we need Claude to use the statutory framework first, then customise the details within each point to reflect Nova’s specific circumstances?”

“Right. The six mandatory points are non-negotiable. But within each point, we can reference Nova’s actual practices – like the 18-month cash runway for going concern, or the 23 regulations being tracked for compliance.”

Arjun began typing a follow-up prompt to fix this critical gap.

Getting the mandatory language right

Follow-up prompt:

The Directors’ Responsibility Statement in your previous response needs correction. Section 134(5) of the Companies Act 2013 mandates that directors must use exact statutory language for six specific points (a) through (f).

Please redraft ONLY the Directors’ Responsibility Statement section using:

- The precise mandatory opening language: ‘The Directors confirm that:’

- All six mandatory points (a) through (f) with their exact statutory wording as required by Section 134(5)

- Within each mandatory point, customise the specific details to reflect Nova AgriTech’s actual circumstances (18-month cash runway, 23 regulations tracked, CFO-certified controls, etc.)

Do not change the core statutory language – only add Nova-specific details within the framework that Section 134(5) requires. This statement will be personally signed by directors, so legal precision is essential.

Click here to see the complete conversation and here to see claude’s response in PDF.

This time, Claude delivered exactly what they needed.

“Perfect,” Ms. Rao said, reviewing the corrected response.

“Now we have the exact section 134(5) framework – ‘The Directors confirm that:’ followed by points (a) through (f) with the precise statutory language.”

She read through each point carefully.

“Look at point (b) – it starts with the mandatory language ‘the directors had selected such accounting policies and applied them consistently…’ then adds Nova’s specific context about the 18-month cash runway. That is exactly right.”

“And point (f) is excellent,” Arjun added.

“It uses the required language about compliance systems, then specifies Nova’s actual approach – the 23 regulations being tracked, the Q3 risk committee establishment, and the proactive regulatory engagement.”

“This is the critical difference between generic compliance and professional legal work,” Ms. Rao emphasised.

“The statutory framework is non-negotiable, but we can make it meaningful by incorporating the company’s actual circumstances within each point.”

Pro tip for readers: If you are unsure how to phrase a prompt to get what you need, do not worry! You can simply tell Claude what you want to achieve and ask it to suggest the right prompt. For example: “I need the Directors’ Responsibility Statement to use exact section 134(5) language. Can you help me create a prompt that will ensure this?”

Human review: The critical final step

“This experience perfectly demonstrates why human oversight is essential when using AI for legal work,” Ms. Rao reflected, looking back at their process.

“Think about what just happened. Claude produced professional-quality content that looked impressive at first glance. The language was sophisticated, the structure was logical, and it covered all the right topics. But it was missing the fundamental legal requirement – the exact section 134(5) mandatory language.”

Arjun nodded.

“Without your legal expertise catching that gap, we would have created a Directors’ Responsibility Statement that directors could not actually sign. It would have looked professional but been legally inadequate.”

“Exactly. This is the perfect example of AI collaboration done right,” Ms. Rao continued.

“AI excels at organisation, structure, and even understanding business context. But it takes human legal judgment to spot when statutory requirements are not being followed precisely.”

“The key insight,” she concluded, “is that AI amplifies human expertise rather than replacing it. Claude handles systematic organisation and professional language, but we make the critical legal judgments that ensure accuracy and compliance.”

What we have accomplished

“In about half an hour, we have created legally compliant Group 3 disclosures that balance mandatory requirements with Nova-specific customisation,” Arjun reflected.

Time comparison:

- Traditional approach: 4-5 hours for Group 3 due to legal precision requirements

- AI-assisted approach: 30+ minutes, including careful legal review

- Quality level: Professional liability protection maintained throughout

Key insights gained:

- Mandatory language preservation while enabling meaningful customisation

- Professional liability considerations require enhanced human oversight

- Context specificity improves authenticity without compromising legal protection

- Systematic approach scales to handle the most sensitive legal content

Ms. Rao reviewed their completed Groups 1-3 sections. “What is remarkable is how each group builds logically. Group 1’s governance structure supports Group 2’s financial performance, which validates Group 3’s professional responsibility claims.”

“The narrative coherence is particularly important for Group 3,” Arjun noted.

“When directors certify their responsibilities, they are backing up the governance and financial stories we have already told.”

Key takeaways:

- Mandatory legal language can be customised with company-specific details

- Professional liability content requires enhanced human oversight and verification

- Context documents enable authentic customisation rather than generic templates

- Legal precision and strategic communication can be balanced with a careful approach

Progress Check: You have now seen how to handle the most legally sensitive board report content using AI. This professional judgment foundation prepares you for Group 4’s external stakeholder communications, where we’ll tackle auditor relations and regulatory disclosures.

Next steps

If you are following the series:

- Next: Part 5 covers Group 4 (External Stakeholders and Audit Relations)

- Previous: Part 3 covered Group 2 (Financial Performance and Capital Management)

If you are new to the series:

- Start from Part 1 for the complete methodology

- Jump to Part 8 to see the live demonstration

Want to try this yourself?

- Always verify mandatory language against actual statutory requirements

- Create detailed context documents for accurate customisation

- Apply enhanced human review for liability-sensitive content

Complete article series

- Part 1: Getting Started

- Part 2: Building the Foundation (Group 1)

- Part 3: Financial Performance and Capital Management (Group 2)

- Part 4: Directors’ Statements and Professional Judgment (Group 3) ← You are here

- Part 5: External Stakeholders and Audit Relations (Group 4)

- Part 6: Risk Management and CSR Disclosures (Group 5)

- Part 7: Final Assembly and Compliance Verification (Group 6)

- Part 8: Live Demonstration – Real-Time Board Report Creation

This professional judgment foundation sets the stage for the external stakeholder communications covered in Part 5, where we will see how Claude handles auditor responses and regulatory relationship management.

Allow notifications

Allow notifications