When an insurance claim is delayed or unfairly denied, filing a strong internal complaint is your first step toward resolution. This article shows how policyholders can use AI to draft clear, persuasive complaints backed by facts and IRDAI regulations. It helps you save time, reduce legal costs, and improve your chances of getting the claim settled.

Table of Contents

Introduction

“I stared at the blank page for two hours.”

That is what Arjun Nair told me when he walked into my office last month. His health insurance claim had been rejected, and he knew he needed to file a formal complaint with the company. But every time he sat down to write, the words just would not come.

“I am so angry I cannot think straight,” he said. “Every draft I write sounds like I am either begging or screaming. Neither feels right.”

Sound familiar?

But here is what I discovered after handling hundreds of insurance disputes: the quality of your first complaint letter determines everything that follows.

“Look,” Arjun continued, spreading documents across my desk, “I have already been fighting this health insurance claim for three months. I have proof of everything: medical emergency, proper hospitalisation, and all required documents submitted on time. But when I complained to their grievance officer, they sent me a two-line response saying my complaint ‘lacks merit.'”

The insurance company had told Arjun something that, unfortunately, rings true in most claim disputes: “Sir, your complaint is too emotional and does not cite proper legal grounds. We need structured grievances that clearly show regulatory violations, not just customer dissatisfaction.”

Here is the reality: most complaint letters filed by insurance claimants are either too emotional (“They cheated me!”), too technical (drowning in legal jargon), or too scattered (jumping between dates and facts). Result? Insurance companies often dismiss them as routine customer service issues rather than serious legal challenges.

“The worst part,” Arjun said, “is that I know I am right. My policy clearly covers this condition, all my documents are genuine, and they are just using technicalities to avoid payment. But I do not know how to put that into a complaint that actually forces them to act.”

Now imagine this: You ask AI for a question checklist, answer the questions, and in one hour, you have a clean, legally sound complaint that actually compels insurance company action.

“I need to file this complaint myself,” Arjun said. “But I do not know how to structure it properly. The company’s grievance officer said most complaints they receive are poorly drafted and don’t lead to action. How do I make sure mine gets their attention?”

“Give me one hour to teach you the framework,” I told him. “You will draft the complaint yourself, but AI will guide you through every step.”

Series overview and recap

We saw how Part 3 of this series equipped legitimate claimants with the legal roadmap to fight wrongful denials.

Now in this article, we will learn how to use AI tools to write professional, legally sound complaint letters to insurance companies. It follows Arjun Nair, whose health insurance claim was wrongfully denied. It provides a 5-step framework using AI prompts to transform frustration into structured complaints that cite specific IRDAI regulations and compel immediate action from insurers.

Before you proceed, know that this series covers:

Part 1: Fraud detection – Spot the red flags and behavioural patterns that reveal insurance fraud before you become a victim.

Part 2: Legal strategy – Build bulletproof cases, whether you are prosecuting fraud or defending against false allegations.

Part 3: Know your rights – Navigate every legal remedy available when insurance companies wrongfully deny your claims.

Part 4 (This article): Effective complaints – Write letters that insurance companies can actually act upon and respond to immediately.

Part 5: Ombudsman – Use this free, powerful system to force companies to pay what they owe.

Part 6: Consumer complaint – Win not just your claim but also compensation for harassment and mental agony.

Part 7: Criminal complaints – File police complaints that prosecutors will actually pursue for fraud and cheating cases.

Part 8: Constitutional protection – Approach a High Court when your fundamental rights are violated or urgent relief is needed.

Whatever you want to know is just a click away!

What exactly is this grievance process?

Think of it as your official way to say “Hey, this is not fair!” to your insurance company. It is not just a suggestion; it is the law. The IRDAI (that is India’s insurance watchdog) made it mandatory for every insurance company to have someone whose job it is to listen to your complaints and fix them. They call this person a Grievance Redressal Officer, or GRO for short.

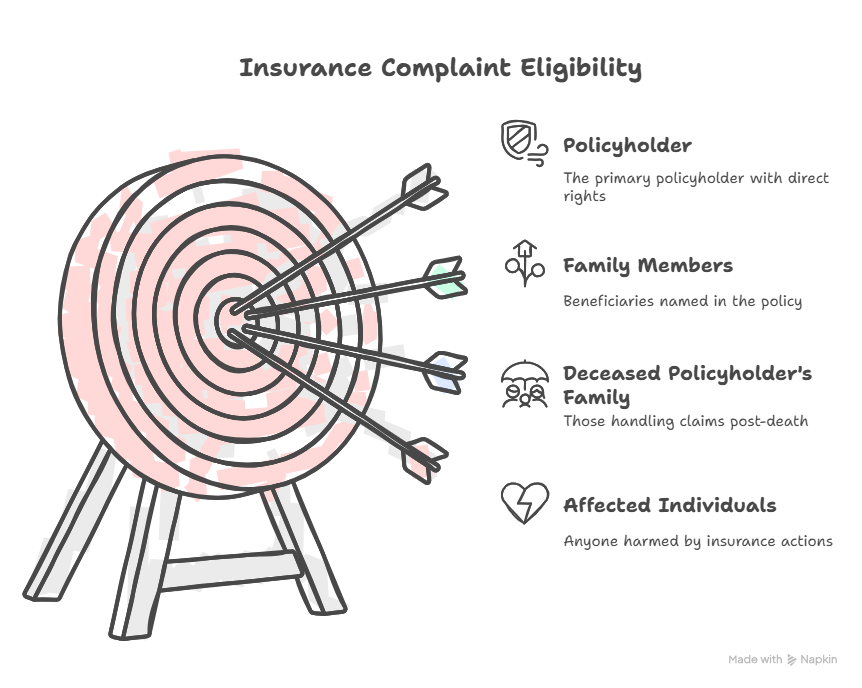

Who can lodge a complaint?

Pretty much anyone who has been affected by the insurance company’s actions:

- You, if you hold the policy

- Your family members named in the policy (like your spouse or kids who would get the money if something happened to you)

- Your family, if you have passed away, and they are dealing with claim issues

- If the insurance company’s decision or behaviour has hurt you or your loved ones, you have every right to speak up.

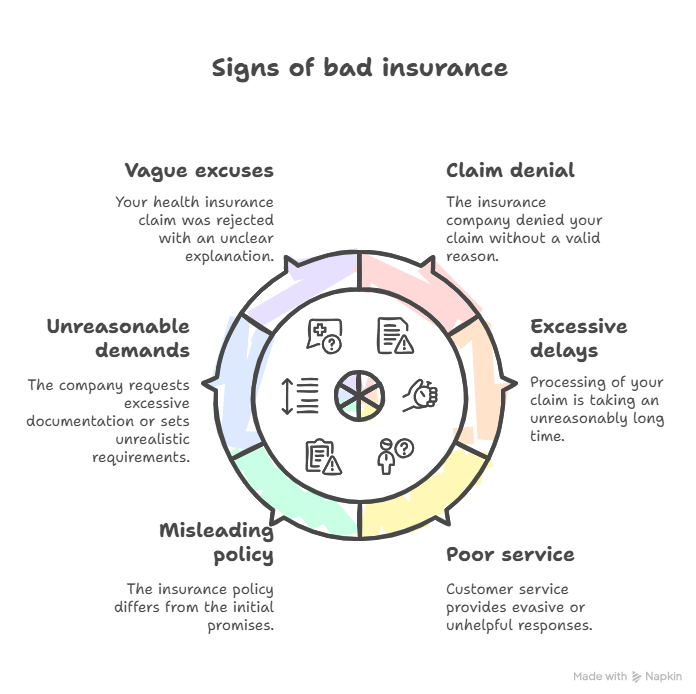

What kind of problems can you complain about?

Almost anything that feels unfair:

- They said “no” to your claim without giving you a real reason

- You have been waiting forever for them to process your claim

- They are giving you the run around when you call customer service

- The policy they sold you is not what they promised

- They are asking for ridiculous documents or making unreasonable demands

- They rejected your health insurance claim with some vague excuse (which, by the way, they are not allowed to do anymore)

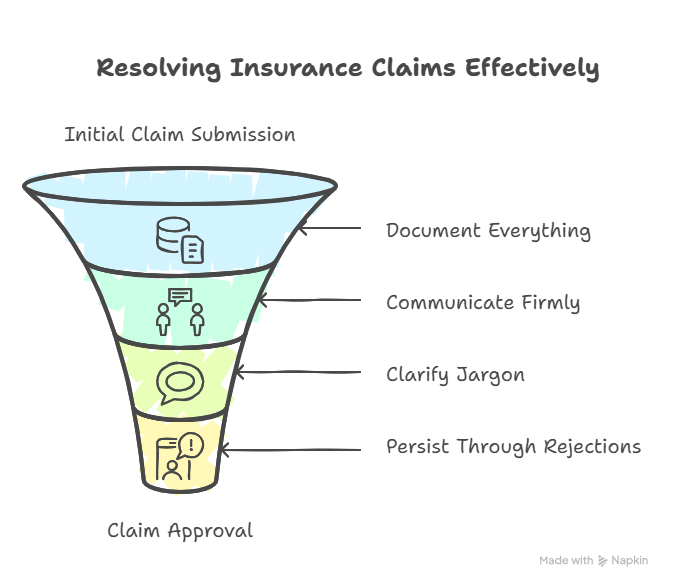

How do you file this complaint?

It is simpler than you think:

Step 1: Find your insurance company’s GRO: Every insurance company has to display its GRO’s contact details prominently. Check their website, and your policy documents, or just call their customer care and ask for the Grievance Redressal Officer’s email or address.

Step 2: Write your complaint: Do not overthink this. Write a simple email or letter explaining:

- Your policy number

- What happened that upset you

- What do you want them to do about it

- Attach any documents that support your case (like the rejection letter, medical reports, etc.)

Step 3: Mention the rules: Add this line to show you know your rights: “I am filing this grievance under Regulation 17 of the IRDAI (Protection of Policyholders’ Interests) Regulations, 2017.”

Step 4: Send it and wait: They have to respond to you within 15 days.

Here are the five steps which will help you write a solid complaint.

The 5-Step AI framework

For Arjun’s case, we used Claude AI (Anthropic) as our primary tool, though this framework works equally well with ChatGPT (OpenAI). Here is why we chose Claude:

- Excellent at maintaining a formal, professional tone

- Strong understanding of the Indian legal context and regulations

- Better at organising complex information chronologically

- Less likely to hallucinate legal provisions or case citations

Also, a quick disclaimer, the prompts and AI responses shown in this article are illustrative examples based on common insurance dispute scenarios. Actual AI responses may vary depending on:

- The specific AI tool used (Claude, ChatGPT, Bard, etc.)

- The version and model you are accessing (free vs. paid versions)

- Your exact wording of prompts and questions

- The complexity of your specific case details

- Timing of your interaction (AI models are regularly updated)

Step 1: Get the question checklist

Goal: Get a complete list of information needed for your insurance complaint.

Prompt:

“I want to draft a formal complaint letter to an insurance company’s Grievance Redressal Officer regarding wrongful claim denial. Before I provide the details, give me a structured list of legal and factual questions I need to answer to ensure the complaint is complete, persuasive, and suitable for escalation under Indian insurance law and IRDAI regulations.”

AI gives you this checklist:

I will provide you with essential questions for drafting an insurance complaint:

FACTUAL QUESTIONS:

About you

- What is your full name, age, and current occupation?

- What is your complete residential address, including the PIN code?

- What is your contact number and email address?

About your insurance policy

- What is your policy number, and what type of insurance do you have (health, life, motor, etc.)?

- When was the policy issued, and what is its current status?

- What is your premium payment history, including frequency and date of last payment?

- What is the name of the insurance company and their registered or branch office address?

About the claim

- What incident or loss are you filing the claim for, and when did it occur?

- What is the total amount you claimed?

- When did you submit your claim, and what documents did you provide at the time?

- How did the insurance company respond, and what was the timeline of their response?

- What specific reason did the company give for rejecting or delaying your claim?

About your complaint history

- When and how did you first raise a complaint with the insurance company?

- Who did you speak with, and do you have any complaints or reference numbers?

- What steps have you taken to resolve the issue so far?

- How did the company respond to your follow-up or grievance?

Legal and regulatory questions

- Do you believe the claim denial violates any terms of your policy?

- Do you have evidence that the company violated IRDAI’s claim settlement timelines?

- Is there any indication of unfair trade practice or service deficiency?

- Do you believe the insurer has violated any specific IRDAI regulations during the claim process?

- Which legal provisions or IRDAI guidelines support your complaint?

Step 2: Give well-thought-out and detailed responses

Goal: Provide complete information for AI to work with.

What to tell AI:

“Here are my detailed answers to all your questions:

About me:

- Arjun Nair, 38 years, Marketing Manager at Tech Solutions Pvt. Ltd.

- A-305, Green Valley Apartments, Khar Road, Mumbai- 400 100

- Mobile: +91-9876543210, Email: [email protected]

About my policy:

- Policy No: HLTH/2021/789456, Family Health Insurance

- Policy issued: April 10, 2021, current and active (over 3 years old)

- Annual premium Rs. 45,000, paid on time via auto-debit on April 5, 2025

- XYZ Health Insurance Ltd., Corporate Tower, Nehru Place, Mumbai- 110019

About the claim

- I am filing the claim for a hospitalisation that occurred due to a sudden cardiac arrest. I was admitted to XYZ Hospital in Mumbai on 15th May 2025 and discharged on 25th May 2025. The incident was unexpected, and I was taken to the emergency unit by my family. The hospitalisation included ICU care, diagnostic tests, and post-discharge medication.

- The total amount claimed is Rs. 8,50,000, which includes hospital room charges, ICU fees, doctor consultations, diagnostic reports, medicines, and follow-up care.

- I submitted the claim on 26th May 2025 through the insurer’s online portal. The documents I attached include:

- Original hospital discharge summary

- Final hospital bill and payment receipts

- Diagnostic reports

- Doctor’s prescription and treatment notes

- Health insurance policy copy

- KYC documents (Aadhaar, PAN)

- The claim form is duly filled and signed

- I received an acknowledgement of receipt of my claim on 21st May. On 23rd May, the insurance company requested additional clarification regarding pre-existing conditions. I provided the requested clarification with my past medical history and a letter from my treating doctor. However, on 25th May 2025, the claim was formally rejected via email. No detailed investigation or verification was done beyond requesting clarification.

- The insurer rejected my claim on the grounds that the treatment was allegedly related to a pre-existing condition not disclosed at the time of policy issuance. However, I have never had any history of cardiac problems and have disclosed all prior conditions at the time of applying. Their basis for rejection is vague and unsupported by any clinical records.

About your complaint history

- I raised my first formal complaint on 6th June 2025 via email to the insurance company’s grievance redressal officer. I also logged a complaint through their online customer care portal the same day.

- I interacted with Mr. Rahul Taneja from the grievance cell over a phone call on 1st June. I was provided with a complaint reference number: GRV-789012-24. I followed up multiple times by phone and email.

- I submitted additional medical documentation from my cardiologist confirming that there was no pre-existing condition. I followed up with written communication and requested a senior-level review. I also submitted a letter of dissatisfaction with the claim handling. Despite repeated efforts, I did not receive a satisfactory resolution.

- The company has maintained the same position and did not offer a fresh review. Their final response on 5th June reiterated the earlier rejection without offering any clarification on how they determined a pre-existing condition existed. They ignored my doctor’s certificate and failed to consider the clinical facts provided.

Legal and regulatory questions

- Yes. The denial violates the terms of my policy, which clearly states that exclusions due to pre-existing conditions apply only when the condition is proven to have existed prior to the policy start date and was not disclosed. Since no such pre-existing condition existed, and no medical proof has been provided by the insurer, the rejection is not in line with the policy terms.

- Yes. As per the IRDAI (Protection of Policyholders’ Interests) Regulations, 2017, insurers are required to process claims within 30 days from receipt of the last required document. My claim was filed on 26th May and was rejected on 30th May without a thorough investigation. The process was rushed and did not reflect a fair evaluation. Additionally, the insurer failed to provide a clear and reasoned decision, as required under the IRDAI norms.

- Yes. Denying a legitimate claim based on unsubstantiated assumptions without conducting due diligence amounts to a deficiency in service. Ignoring a treating doctor’s certificate and failing to review supplementary evidence also constitutes an unfair trade practice under the Consumer Protection Act 2019.

- Yes. The insurer has violated:

- Regulation 9(6) of the IRDAI (Protection of Policyholders’ Interests) Regulations, 2017, mandates a reasoned decision in writing for every claim rejection.

- Regulation 27 of the IRDAI (Health Insurance) Regulations, 2016, requires that insurers carry out fair and objective claim investigations.

- IRDAI Circular Ref: IRDA/HLT/REG/CIR/190/07/2020, which prohibits insurers from rejecting claims arbitrarily on vague grounds such as undisclosed conditions without medical proof.

- Section 2(11) of the Consumer Protection Act 2019 defines a deficiency in service.

- Regulations 9 and 27 of IRDAI’s Health Insurance and Protection of Policyholders Regulations

- IRDAI Master Circular on Health Insurance Business (July 2020)

- IRDAI’s timelines and redressal process under the Grievance Redressal Guidelines

- My policy booklet outlines the conditions under which claims may be denied, none of which apply in this case

AI responds: Thank you for the comprehensive information. Based on your answers, this is a case of wrongful claim denial involving regulatory violations, service deficiency, and potential unfair trade practices. I have all the information needed to draft a strong complaint that will compel immediate investigation and resolution.

Pro tip: Be as specific as possible with dates, amounts, and reference numbers.

Step 3: Get your first draft

Goal: Receive a mostly well-structured document, with the facts laid out in chronological sequence.

What to ask AI:

“Based on my detailed answers above, please draft a comprehensive complaint letter to the insurance company’s Grievance Redressal Officer that clearly establishes regulatory violations and compels immediate action for claim settlement.”

AI response can be seen here.

What you do: Read through carefully and identify areas that need improvement.

Step 4: Ask for specific improvements

Goal: Perfect your complaint by targeting specific weaknesses.

Refinement options (choose what you need):

For a stronger legal foundation:

“Add specific IRDAI regulation numbers and explain in simple language how each regulation applies to the facts of this case.”

For better timeline clarity:

“Add more specific details about each step in the claim process and what evidence supports each regulatory violation.”

For enhanced urgency:

“Strengthen the consequences section with specific details about escalation to the ombudsman, consumer forum, and IRDAI complaints.”

For more evidence clarity:

“Organise the evidence to show exactly what each document proves about the wrongful denial.”

AI gives an improved version (for example after asking for a stronger legal foundation):

Step 5: Enhance it where needed

Once you receive the improved version, make a few additional edits (it is usually mainly structural) to address points AI might have missed:

AI response:

To

Date: 02/07/2025

The Grievance Redressal Officer,

XYZ Health Insurance Ltd.,

Corporate Tower, Nehru Place,

Mumbai – 110019

Subject: Formal Complaint under Section 42 of the Insurance Act 1938 and IRDAI Regulations regarding against wrongful denial of Health Insurance Claim (Policy No: HLTH/2021/789456)

Sir/Madam,

- I, Arjun Nair, aged 38 years, Marketing Manager with Tech Solutions Pvt. Ltd., resident of A-305, Green Valley Apartments, Khar Road, Mumbai – 400100, Mobile: +91-9876543210, am filing this

formalcomplaint underSection 42 of the Insurance Act, 1938, and - I hold a family health insurance policy HLTH/2021/789456 issued on April 10, 2021, with an annual premium of Rs. 45,000 paid punctually via auto-debit on April 5, 2025. On May 15, 2025, I suffered a sudden cardiac arrest and was rushed to XYZ Hospital, Mumbai Emergency Department, by my family. This was a completely unexpected medical emergency requiring immediate ICU care, diagnostic tests, and intensive treatment.

- I was admitted to XYZ Hospital on May 15, 2025, and discharged on May 25, 2025, after receiving critical cardiac care including ICU treatment, comprehensive diagnostic workup, and post-discharge medication. Total medical expenses amounted to Rs. 8,50,000, covering hospital room charges, ICU fees, doctor consultations, diagnostic reports, medicines, and follow-up care.

- Upon discharge,

I submitted - Despite submitting complete documentation for a genuine medical emergency, your company rejected the claim on May 30, 2025, citing “treatment related to pre-existing condition not disclosed at policy issuance.” This denial is medically and legally unsound and violates multiple regulations:

- This is to reiterate that my policy, issued on April 10, 2021, has been in force for over three years, making it legally incontestable under section 45

, Thiswhich prohibits questioning policies on the grounds of non-disclosure after three years unless fraud is specifically proven. Your denial citing “undisclosed pre-existing condition” directly violates this statutory protection without any allegation or proof of fraud. - Further, I have never had any history of cardiac problems and disclosed all prior medical conditions at policy inception. Sudden cardiac arrest can occur in individuals with no prior cardiac history. Your rejection is based on unsubstantiated assumptions without any medical evidence or clinical proof of pre-existing cardiac conditions.

- As soon as I received your rejection letter, I raised a formal complaint on 1st June 2025 (Reference: GRV-789012-24) with Mr. Rahul Taneja from your grievance cell. Despite providing additional medical documentation from my treating cardiologist confirming no pre-existing cardiac condition, your final response on June 5, 2025, reiterated the same unsupported position without addressing the clinical evidence provided.

- Given the above circumstances, you have violated the following IRDAI regulations:

- Regulation 9(6) of IRDAI (Protection of Policyholders’ Interests) Regulations 2017: Failed to provide a reasoned decision in writing with specific medical evidence for claim rejection.

- Regulation 27 of IRDAI (Health Insurance) Regulations, 2016: Failed to conduct a fair and objective claim investigation, rejecting the claim within 5 days without a proper medical review.

- IRDAI Circular Ref: IRDA/HLT/REG/CIR/190/07/2020: Violated prohibition against arbitrary claim rejection on vague grounds without medical proof.

- Timeline Violation: Rushed rejection within 5 days contradicts the requirement for a thorough investigation as mandated under IRDAI guidelines.

- You are aware that the arbitrary denial without proper medical investigation constitutes a “deficiency in service” under section 2(11) of the Consumer Protection Act 2019, as your company failed to meet reasonable professional standards expected from a health insurance provider.

EVIDENCE SUPPORTING CLAIM VALIDITY:

1. Complete medical records from XYZ Hospital confirming an emergency cardiac event

2. Treating cardiologist’s certificate confirming no pre-existing cardiac condition

3. Comprehensive diagnostic reports showing an acute cardiac episode

4. Three years of premium payment history demonstrating policy compliance

5. Original policy application showing complete medical disclosure

6. Hospital discharge summary confirming successful emergency treatment

- In view of the clear regulatory violations and arbitrary denial, I request:

- Immediate settlement of Rs. 8,50,000 within 15 days as mandated by IRDAI regulations

- Interest at 9% per annum for delay beyond regulatory timelines

- Written explanation with medical evidence supporting pre-existing condition claim

- Compensation for mental agony caused by wrongful denial during a cardiac emergency

- Failure to resolve this matter within the stipulated 15-day period will compel me to:

- File a complaint with the insurance ombudsman

- Approach the consumer commission under the Consumer Protection Act 2019

- File a complaint with IRDAI’s Integrated Grievance Management System (IGMS)

Yours faithfully,

Arjun Nair

Mobile: +91-9876543210

Email: [email protected]

Date: [Current Date]

Enclosures:

1. Copy of health insurance policy HLTH/2021/789456

2. Premium payment receipts and auto-debit confirmations

3. Complete medical records from XYZ Hospital

4. Emergency admission and discharge summary

5. Cardiac diagnostic reports and test results

6. Treating cardiologist’s certificate confirming no pre-existing condition

7. Itemised hospital bills and payment receipts

8. Original claim submission acknowledgement

9. Claim rejection email dated June 5, 2025

10. Grievance complaint correspondence (Reference: GRV-789012-24)

11. Additional medical documentation submitted during the grievance process

See how smooth that was? The AI did not just give a generic template; it actually organised the facts in legal order, incorporated specific regulations, and created something immediately usable. You only need to make minor personal touches.

What happens next?

The insurance company has to investigate your complaint properly and give you a written answer. They cannot just brush you off or give you a copy-paste response. If they are rejecting your complaint, they need to explain why with proper reasons.

If you are still not happy (or if they ignore you completely), you have two powerful options:

- Go to the Insurance Ombudsman – think of this as a free judge who specialises in insurance disputes

- File a case in the consumer court – another free option where you can get compensation for the harassment you have faced

You know the best part? You do not have to hire a lawyer or be one to use this system.

A few practical tips:

- Keep copies of everything: every email, every letter, every phone call record

- Be polite but firm in your communication

- Do not let them intimidate you with technical jargon

- If you do not understand something, ask them to explain it in simple terms

Most importantly: Do not give up after the first “no.” Many legitimate claims get approved once you file a formal grievance because companies realise you are serious about getting justice.

Why this 5-Step method works

For claimants:

- Clear roadmap: No confusion about what information is needed

- Complete coverage: AI’s questions ensure nothing important is missed

- Professional result: A legally formatted complaint that companies take seriously

- Time efficient: One hour vs. weeks of confusion and rewrites

For insurance companies:

- Easy to understand: Clear regulatory violations and timeline

- Action-oriented: Specific legal requirements demanding immediate response

- Evidence-ready: Clear documentation trail for internal review

- Professional presentation: Proper legal formatting commands respect and escalation awareness

Final thoughts

This systematic approach transforms insurance claimants from frustrated customers into empowered consumers, using AI as their legal assistant to ensure professional presentation and complete regulatory coverage.

Remember: You are not trying to become a lawyer; you are organising your facts in a way that makes it easy for insurance companies to see the regulatory violations and take immediate corrective action.

The insurance industry operates on risk assessment. Companies that recognise you as a knowledgeable, persistent claimant with strong legal grounds will settle quickly rather than risk regulatory action or adverse precedents.

Your AI-assisted complaint letter is your first demonstration of that knowledge and persistence. Make it count.

Next, we will show you exactly how to approach the Ombudsman and draft a complaint that gets results.

Frequently asked questions

- Can AI really help me write a complaint letter that is as good as what a lawyer would draft?

AI can structure your facts professionally and cite relevant regulations, but it is not a replacement for legal expertise in complex cases. For straightforward claim denials under Rs. 10 lakhs, AI-assisted complaints often achieve similar results to lawyer-drafted ones at a fraction of the cost.

- What if the AI gives me wrong legal information or cites regulations that do not exist?

Always verify AI-generated legal citations against official IRDAI and government websites before submitting. AI can occasionally hallucinate legal provisions, so treat it as a drafting assistant, not a legal authority. When in doubt, consult a qualified lawyer.

- How quickly can I expect results after sending an AI-drafted complaint letter?

Well-structured complaint letters typically get acknowledged within 2-3 days and resolved within 15-30 days if they clearly demonstrate regulatory violations. Insurance companies often settle quickly when they recognise legally informed complaints rather than risk ombudsman or consumer forum proceedings.

- Should I use the exact AI response or modify it for my situation?

Never copy-paste AI responses verbatim. Always personalise the language, verify all facts and figures, and adapt the tone to match your specific circumstances. The AI provides structure and a legal framework, but your unique situation requires customisation.

- What is the biggest advantage of using AI over writing the complaint myself?

AI helps you stay objective and professional when you are emotionally frustrated, ensures you do not miss important legal provisions like section 45 protection, and structures your complaint in a logical sequence that insurance companies take seriously rather than dismissing it as emotional venting.

Allow notifications

Allow notifications