Master insurance fraud detection with this practical guide for legal professionals. Learn proven techniques to spot red flags, authenticate documents, and identify suspicious claim patterns. From client meeting to case building, discover actionable frameworks that transform suspicion into successful prosecution. Essential for legal practitioners and investigators seeking to protect clients from fraudulent schemes.

Table of Contents

Introduction

Three months into my practice, I sat across from Firdaus, a 45-year-old marketing wizard whose health insurance claim had been rejected. She had undergone what she claimed was emergency cardiac surgery, but the insurer suspected fraud. The hospital bills looked pristine. The discharge summary was detailed. Everything seemed legitimate.

Until we noticed the doctor’s signature on the discharge summary did not match his signature on the admission form.

That single inconsistency unravelled a Rs. 15 lakh fraud involving fake medical procedures, forged documents, and a network of complicit healthcare providers. Firdaus was not the victim; she was the orchestrator. But what struck me most about this case was not the sophistication of the fraud; it was how easily it could have been detected within 48 hours if someone had known what to look for.

This pattern repeats across India’s insurance sector daily. Insurance fraud costs the industry over Rs. 45,000 crores annually, and that is not just a number on a corporate balance sheet. Every fraudulent claim translates to higher premiums for honest policyholders, reduced coverage options, and a climate of suspicion that affects genuine claimants who desperately need help.

The Firdaus case taught me that early detection is not just about saving money; it is about protecting the entire ecosystem. When we catch fraud early, we prevent fraudulent networks from expanding, protect genuine policyholders from premium increases, maintain the integrity of the insurance system, and reduce litigation costs for all parties involved.

The first part of our 8-part series focuses on detection, the make-or-break stage in any insurance fraud case. From phantom hospitalisations to staged car crashes, we will uncover common schemes, behavioural red flags, and document tells. You will also learn practical tools to catch fraud early because, in insurance fraud, prevention is often the only real cure.

What will this series cover?

Ever wondered why some people win against insurance companies while others give up? This 8-part series gives you the exact strategies that work.

Part 1 (This article): Fraud detection – Spot the red flags and behavioural patterns that reveal insurance fraud before you become a victim.

Part 2: Legal strategy – Build bulletproof cases, whether you are prosecuting fraud or defending against false allegations.

Part 3: Know your rights – Navigate every legal remedy available when insurance companies wrongfully deny your claims.

Part 4: Effective complaints – Write letters that insurance companies can actually act upon and respond to immediately.

Part 5: Ombudsman – Use this free, powerful system to force companies to pay what they owe.

Part 6: Consumer complaint – Win not just your claim but also compensation for harassment and mental agony.

Part 7: Criminal complaints – File police complaints that prosecutors will actually pursue for fraud and cheating cases.

Part 8: Constitutional protection – Approach the High Courts when your fundamental rights are violated or urgent relief is needed.

Whether you are a policyholder fighting denial, a lawyer building cases, or an investigator catching fraud, you will have the practical tools that level the playing field against giant corporations.

Ready to turn legal rights into real results?

Types of insurance fraud

A. Health Insurance

“Doctor says I need immediate surgery,” the caller told our client, a health insurer, at 2 AM on a Sunday. Red flag number one: Genuine medical emergencies rarely involve detailed insurance discussions at midnight.

Common health insurance frauds:

- Phantom treatments: Billing for procedures never performed. I once reviewed a case where a patient was allegedly treated for a broken leg while hospital CCTV showed him walking normally throughout his stay.

- Upcoding: Billing simple procedures as complex ones. A routine appendectomy becomes “complicated laparoscopic surgery with multiple complications.”

- Staged accidents: Coordinated between patients, doctors, and sometimes ambulance operators. The timing is usually suspicious, claims filed within hours of policy activation.

B. Life insurance

The “repeat death” fraud I mentioned earlier is not uncommon. Here is how it typically works:

A person takes multiple life insurance policies under slightly different names or using family members’ identities. When they stage their death, claims are filed across different insurers who don’t immediately cross-reference.

Case Study: The Fisherman’s Tale

In 2022, I handled a case where a fisherman from Kerala had allegedly drowned. His wife filed claims with three different insurers totalling Rs. 40 lakhs. The death certificate was genuine. The police report seemed authentic.

The fraud unravelled when we noticed something odd: the man’s mobile phone had been active for two days after his supposed death, accessing social media from a location 200 kilometres away.

Turns out, he had bribed local officials to issue a false death certificate after staging his drowning. He planned to live under a new identity while his family collected the insurance money.

Section 45 of the Insurance Act 1938 mandates that life insurance policies cannot be disputed after three years, except in cases of fraud. This makes early detection crucial, as proving fraud becomes significantly harder.

C. Motor insurance

“The accident happened so fast, I could not avoid hitting his car,” explained the claimant. But the traffic camera footage told a different story; it showed him deliberately ramming into a stationary vehicle.

- Staged accidents are elaborate productions. Multiple vehicles, fake witnesses, and sometimes even corrupt police officers participate. The total claim value is usually split among participants.

- Phantom repairs involve claiming for repairs never done or inflating actual repair costs. I have seen cases where claimants submitted bills for Rs. 2 lakh worth of parts for a minor dent that required Rs. 20,000 in actual repairs.

- Vehicle dumping: Owners stage thefts or accidents for vehicles with outstanding loans or mechanical problems. The vehicle is either sold in parts or hidden until the insurance payout is received.

D. Commercial insurance

Commercial insurance fraud often involves sophisticated financial manipulation.

- Inventory inflation: Businesses inflate inventory values before filing theft or fire claims. I once worked on a case where a textile manufacturer claimed Rs. 50 lakhs worth of silk was destroyed in a fire. The reality? Most of the silk had been sold months earlier; the fire was deliberately set to destroy evidence.

- Arson for profit: Struggling businesses sometimes resort to deliberately destroying their property. The challenge for lawyers is proving intent, especially when the fire appears accidental.

- False employee claims: Companies create fake employees to claim workers’ compensation benefits. Payroll records are manipulated, and benefits are paid to non-existent workers.

E. Agent and broker fraud

Sometimes the fraud comes from within the insurance ecosystem itself.

- Premium skimming: Agents collect premiums from clients but never forward them to insurers. Clients only discover the fraud when they try to file claims.

- Churning: Agents repeatedly cancel and rewrite policies to generate additional commissions, often without client knowledge.

- Forged applications: Agents forge client signatures or misrepresent client information to secure policies that would not otherwise be approved.

Under section 42 of the Insurance Act 1938, agents owe fiduciary duties to both insurers and clients. Breaching these duties can result in license cancellation and criminal prosecution for cheating under section 318 of the Bharatiya Nyaya Sanhita 2023 (“BNS”).

Common red flags and suspicious indicators

After eight years of practice, I have learned that insurance fraudsters follow patterns. They cannot help themselves.

A. Behavioural red flags

- The over-eager claimant

Genuine claimants are often stressed, confused, and need guidance through the claims process. Fraudulent claimants? They know the process too well.

I once met a “victim” who rattled off policy terms and conditions from memory, cited specific IRDAI guidelines, and provided pre-printed forms for every conceivable document the insurer might request. His house had allegedly been burgled, but he seemed more excited than distressed.

Real victims ask questions like: “What happens next?” or “How long will this take?”

Fraudsters make statements like: “As per the xyz clause of the policy terms, you need to process this within 30 days.”

- The evasive storyteller

Truth-tellers provide consistent details even when questioned repeatedly. Liars struggle with consistency.

A simple technique I use is to ask for the same information in different ways during different conversations. Genuine claimants provide the same core facts. Fraudsters often contradict themselves.

- The documentary evidence enthusiast

Be suspicious when claimants provide too much documentation too quickly. Genuine claimants often struggle to gather the required documents. Fraudsters come prepared with everything, sometimes even documents you have not requested yet.

B. Documentation inconsistencies

- Signature analysis

This saved us in Firdaus’s case. Simple signature comparison can reveal:

- Different writing instruments are used across supposedly related documents

- Varying pressure patterns

- Inconsistent letter formations

- Date discrepancies

Medical reports dated before the alleged injury. Police FIRs filed after insurance claims. Purchase receipts for items claimed as stolen but dated after the alleged theft.

- Language patterns

Multiple documents supposedly from different sources but showing identical writing styles, vocabulary, or formatting patterns often indicate a single author.

- Forensic red flags

Documents that look too clean for their supposed age or circumstances. Hospital discharge summaries without standard hospital letterheads. Police reports without proper case numbers or registration details.

C. Timing and pattern analysis

- The new policy rush

Claims filed within days or weeks of policy inception deserve extra scrutiny. While genuine emergencies do occur, statistical analysis shows that fraudulent claims are disproportionately filed during early policy periods.

- Seasonal patterns

Certain types of fraud spike during specific seasons. Vehicle thefts increase before Diwali (when vehicle demand is high). Health claims often surge just before policy renewal dates.

- The serial claimant

Policyholders with multiple claims across different insurers or excessive claims frequency compared to statistical norms warrant investigation.

- Geographic clustering

Multiple similar claims from the same locality, involving the same hospitals, repair shops, or service providers, often indicate organised fraud rings.

Tools and techniques for detection

- Manual review

Despite advances in technology, human judgment remains irreplaceable in fraud detection.

- The three-call rule

I always insist on at least three separate conversations with claimants:

- Initial call: Let them tell their story without interruption

- Detail verification: Ask specific questions about the circumstances

- Document review: Discuss submitted documents and request clarifications

Inconsistencies may emerge across these conversations.

- Site verification

For significant claims, physical verification is essential. I have caught fraudsters by simply visiting the alleged accident site and finding that the claimed circumstances were physically impossible.

- Witness interviews

Independent witness interviews often reveal crucial details. Fraudulent witnesses tend to provide overly detailed accounts that sound rehearsed, while genuine witnesses remember only key information clearly.

- Technology-assisted detection

- Data analytics and pattern recognition: Modern insurers use sophisticated algorithms to flag suspicious patterns

- Claims velocity: Multiple claims from the same area within short timeframes

- Network analysis: Identifying connections between claimants, healthcare providers, and service stations

- Artificial intelligence and machine learning applications in fraud detection:

These technologies are widely used in 2025, with insurers leveraging AI for predictive analytics, natural language processing (NLP) for document analysis, and computer vision for image verification:

- Analyse document authenticity through advanced NLP, examining fonts, formatting, and linguistic patterns

- Cross-reference claims data with public records and databases using predictive analytics

- Identify image manipulation in submitted photographs through computer vision technology

- Leading Indian insurers like Bajaj Allianz deploy AI-driven fraud detection systems for real-time claim analysis

- IRDAI’s 2024 Sandbox Regulations actively encourage insurtech innovation and technology adoption for fraud prevention

- Database cross-referencing

The General Insurance Council’s Motor Insurance Database helps identify:

- Multiple claims for the same incident

- Vehicles with suspicious claim histories

- Patterns across different insurers

- Forensic audits

- Financial analysis

Forensic accountants can uncover:

- Inconsistencies between claimed losses and actual financial impact

- Suspicious financial transactions preceding claims

- Tax return discrepancies with claimed asset values

- Digital forensics

Modern investigations often require digital forensics:

- Mobile phone data analysis to verify location claims

- Social media activity inconsistent with claimed injuries or losses

- Email trail analysis reveals premeditation

- Medical record analysis

For health insurance claims, independent medical experts can identify:

- Treatments inconsistent with diagnosed conditions

- Billing patterns suggesting unnecessary procedures

- Medical records showing evidence of pre-existing conditions were not disclosed

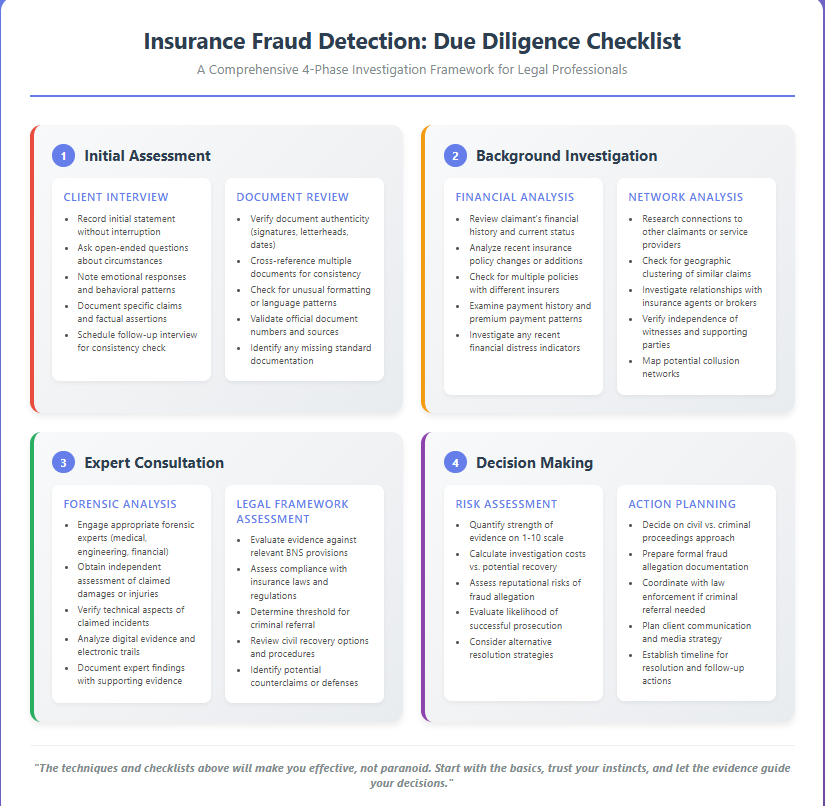

Role of lawyers in insurance fraud detection: A step-by-step case study

Our role extends far beyond courtroom advocacy. We are often the first line of defence against insurance fraud. Let me walk you through exactly how this works in practice using a case that landed on my desk two years ago.

Case study: the Rs. 25 lakh commercial fire fraud

The initial call

The call came from Star General Insurance Company. “We have a suspicious commercial fire claim that needs investigation,” said their claims director. “Our initial review has raised several red flags, and we need legal guidance on how to proceed.”

The claim was filed by Mr. Kapoor, owner of a mid-sized textile business in Surat. The claim amount: Rs. 25 lakhs for destroyed inventory and property damage. Mr. Kapoor had submitted all required documentation, fire department reports, police FIR, and inventory records, but the insurance company’s internal review team suspected something was not right.

As the insurance company’s counsel, my role was to determine whether this was a legitimate claim or an elaborate fraud, and if fraud was suspected, to build a case that would stand up in court.

Here is exactly how I approached this case, step by step:

Step 1: The due diligence framework in action

A. Client interview protocol

Instead of accepting the documents at face value, I implemented my structured questioning approach:

Initial meeting: Working with the insurance company’s claims team, I structured the interview with Mr. Kapoor around key questions:

- “Tell me about the fire in your own words, from the beginning.”

- “When did you last visit the warehouse before the incident?”

- “Who has access to the warehouse keys?”

- “What security measures were in place?”

Mr. Kapoor’s story was remarkably detailed, too detailed. He described the exact time the fire started (2:47 AM), the wind direction, and even the colour of the flames. Most genuine victims struggle to remember precise details during traumatic events.

Follow-up meeting: I asked the same questions differently:

- “Walk me through your evening routine on the day before the fire.”

- “How did you learn about the fire?”

- “What was your first reaction?”

Red flag alert: His timeline had shifted by 20 minutes, and suddenly he “remembered” receiving a call from a security guard, a detail absent from his initial account.

B. Document authentication process

Working with forensic document experts, we examined:

- Inventory records: The warehouse supposedly contained Rs. 20 lakhs worth of silk fabric

- Purchase invoices: Recent bulk purchases from suppliers

- Fire department report: Professional assessment of fire cause and damage

- Insurance policy: Coverage details and recent amendments

Discovery: The inventory records showed massive fabric purchases just two weeks before the fire. When we cross-referenced with supplier bank records (with proper legal authorisation), we found the payments were made, but the goods were never delivered to the warehouse address.

- Background verification deep dive

Our investigation revealed:

- Mr. Kapoor’s business had been struggling with cash flow for six months

- He had recently increased his insurance coverage by 40%

- Two similar businesses in the same industrial area had filed fire claims in the past year

- All three businesses shared the same insurance agent

Step 2: Legal risk assessment framework

Before advising the insurance company to contest the claim, I systematically evaluated:

- Strength of evidence analysis

Available evidence:

- Contradictory witness statements

- Suspicious inventory procurement patterns

- Financial distress documentation

- Forensic fire investigation inconsistencies

Missing evidence:

- Direct proof of arson

- Clear motive beyond financial difficulty

- Witness to deliberate fire-setting

- Potential defence strategies

Fraudsters typically raise these defences:

- Genuine emergency defence: “We were in financial trouble, but the fire was accidental”

- Documentation error defence: “Any inconsistencies are due to stress and confusion”

- Third-party liability: “Someone else may have set the fire”

- Cost-benefit analysis

- Investigation costs: Rs. 3 lakhs (forensic experts, legal fees, documentation)

- Potential fraudulent payout: Rs. 25 lakhs

- Risk of wrongful denial: Reputational damage + potential bad faith claims

- Benefits of successful fraud detection: Setting precedent, preventing network expansion

Decision: Proceed with formal fraud investigation.

Step 3: Internal investigation management

- Evidence preservation protocol

Physical evidence:

- Secured fire-damaged samples before cleanup commenced

- Photographed the scene from multiple angles within 48 hours

- Obtained original CCTV footage from neighbouring buildings

- Preserved electronic records through proper forensic imaging

Digital evidence:

- Secured Mr. Kapoor’s business email account (with court order)

- Preserved mobile phone data showing location history

- Obtained bank transaction records for the past 12 months

- Secured insurance agent communication records

Chain of custody: Every piece of evidence was catalogued with:

- Collect the timestamp and location

- Personnel involved in the collection

- Storage conditions and security measures

- Transfer documentation between experts

- Coordinating with law enforcement

When to involve police: I initiated police involvement when we discovered evidence suggesting deliberate fire-setting. Here is the legal framework I followed:

Section 318 BNS (Cheating): Required proving:

- Deception by Mr. Kapoor (false inventory claims)

- Inducement of the insurance company to act (file a claim)

- Resulting wrongful loss (Rs. 25 lakh potential payout)

Section 326 BNS (Mischief by fire with intent to destroy building):

- A deliberate act of setting fire to a building or structure

- Specific intent to destroy or damage the building

- The building was actually damaged or destroyed by fire

Section 336 BNS (Forgery): Required proving:

- Creation of false documents (inflated inventory records)

- Intent to defraud (increase claim amount)

- Potential use in legal proceedings (insurance claim process)

Evidence submission:

- Filed a FIR with the local police station

- Provided forensic reports as supporting evidence

- Coordinated witness statements with the investigating officer

- Maintained parallel civil investigation for insurance purposes

- Managing legal privilege

Protecting privileged communications:

- Structured investigation through the insurance company’s in-house counsel

- Used common interest privilege for multi-party coordination (insurer, reinsurer, legal team)

- Maintained separate files for privileged vs. discoverable materials

Disclosure obligations: When criminal conduct became apparent, I:

- Informed the insurance company of disclosure obligations

- Advised on mandatory reporting requirements under IRDAI guidelines

- Structured communications to protect legitimate privilege claims

Step 4: Client advisory role

- Risk mitigation strategies implementation

Based on this case, I advised the insurance company to implement:

Policy design improvements:

- Mandatory cooling-off periods for coverage increases above 25%

- Required independent inventory verification for claims above Rs. 10 lakhs

- Enhanced background checks for new commercial policies

Claims handling procedures:

- Two-person interaction requirement for high-value claims

- Mandatory site inspection within 24 hours of claim filing

- Cross-referencing system for allegations involving the same agents or geographic areas

- Regulatory compliance management

IRDAI compliance checklist:

- Reported suspected fraud within 30 days as required

- Maintained investigation timeline within prescribed limits

- Documented customer grievance handling process

- Ensured data protection compliance during the investigation

Step 5: Building anti-fraud professional networks

- Essential professional relationships

Successful fraud detection requires a network of trusted professionals:

Forensic experts and investigators: I maintain relationships with specialists in fire investigation, document analysis, digital forensics, and financial fraud. These relationships prove invaluable when cases require rapid expert consultation.

Medical professionals: For health insurance fraud cases, having access to independent medical experts willing to provide honest opinions is crucial. I have built relationships with doctors across specialities who understand the legal requirements for expert testimony.

Technology specialists: Digital evidence analysis has become essential in modern fraud investigations. I work with specialists who can trace electronic communications, analyse metadata, and preserve digital evidence properly.

Law enforcement officers: Building relationships with officers specialising in financial crimes helps ensure smooth coordination when criminal referrals become necessary. These relationships also provide insights into emerging fraud patterns.

Conclusion

Eight years ago, I thought insurance law was about interpreting policy terms and arguing coverage disputes. I was wrong.

Today’s insurance lawyer must be part detective, part data analyst, and part behavioural psychologist. The fraudsters are getting organised; that means we need to be more hands-on.

But here is what gives me hope: every fraud case I have worked on has made me better at spotting the next one. Every technique fraudsters develop leaves traces for those who know how to look.

Detection is only half the battle. Once you have identified fraud, what are your legal options? How do you build a bulletproof case? What are the procedural pitfalls that can derail even strong fraud cases?

Part 2 of this guide will cover:

- Civil vs. criminal proceedings: choosing your battlefield

- Evidence standards and burden of proof challenges

- Specific sections of the BNS, Insurance Act, and IRDAI regulations

- Practical litigation strategies that actually work

- Settlement vs. prosecution: making the strategic choice

- Protecting your client from counterclaims and reputation damage

I will share stories from cases where we got it right and cases where we got it spectacularly wrong. Because in fraud litigation, experience is not just the best teacher; it is often the only teacher.

FAQs

- Can I be held liable if I unknowingly assist my client in filing a fraudulent claim?

No criminal liability, but you could face professional misconduct charges if you ignored obvious red flags. Always exercise reasonable due diligence, ask if the story makes sense, the documents look authentic, and the client’s behaviour seems genuine.

- What’s the most common mistake lawyers make in fraud investigations?

Focusing only on documents while ignoring behavioural red flags. People can forge papers but struggle to maintain consistent lies. Always interview claimants multiple times and watch for inconsistencies in their stories.

- Are there regional fraud patterns in India I should know about?

Yes. Kerala has marine insurance fraud, Gujarat sees industrial fire fraud (especially textiles), Punjab has crop insurance fraud, and Mumbai/Delhi have sophisticated motor accident networks. Regional patterns often reveal organised rings.

- What if I discover my insurance client is systematically denying legitimate claims?

Document everything, review your retainer agreement, and consider withdrawal. You cannot assist systematic fraud. Short-term loss protects long-term reputation.

- Can AI replace human judgment in fraud detection?

No, but it is a powerful tool. AI handles pattern recognition and database cross-referencing, but misses behavioural cues, cultural context, and ethical nuances. The future is AI screening + human investigation for complex cases.

Allow notifications

Allow notifications