In the first of two parts, master essential practical skills to tackle healthcare fraud, learn how to identify medical scams, collect strong evidence, and engage effectively with police and consumer forums. Whether you are a healthcare lawyer, law student, or a victim of fraud, this guide equips you with actionable tools to get you started.

Table of Contents

Introduction

Dean’s introduction:

“Good morning, distinguished faculty and future advocates. Today, we have the privilege of hosting Mr. Shoumen Chatterjee, a healthcare attorney. Over the past thirteen years, Mr. Chatterjee has investigated over 200 cases of healthcare fraud, recovered more than Rs. 100 crores for victims and insurers, and helped draft landmark legislation that now protects millions of patients nationwide.

His expertise spans from complex hospital billing schemes to pharmaceutical kickback networks, and his cases have been featured in landmark Supreme Court judgments.

Today, he will share insights from the front lines of healthcare fraud investigation, providing you with both the legal framework and practical tools, such as complaint drafting and investigating techniques, that you will need as future practitioners. Please join me in welcoming Mr. Shoumen Chatterjee”.

Mr. Chatterjee’s opening:

“Thank you, Dean Sharma, for that generous introduction. Good morning, future lawyers.

When I first stepped into a courtroom eighteen years ago to argue my first healthcare fraud case, I thought I understood what medical fraud looked like. I imagined it would be obvious: falsified documents, blatantly fake procedures. I was naive. The reality of healthcare fraud is far more insidious and more sophisticated than I ever imagined.

Healthcare fraud is not just about numbers on spreadsheets or regulatory violations. It is about vulnerable people at their most desperate moments being exploited by the very system designed to save them.

Let me share with you the human face of this crisis, because understanding the victims is what will make you effective advocates.

Mrs. Desai is a 67-year-old retired mathematics teacher from Pune. One morning, she opens her insurance statement to find a Rs. 4.5 lakh charge for cardiac bypass surgery performed at Mumbai’s “Premier Heart Institute.” The date of service? Last Tuesday. The only problem? Mrs. Desai has never been under anaesthesia in her life, has never set foot in Mumbai, and her heart is perfectly healthy.

Or consider Rati Sharma, a new mother in Bangalore. When her eighteen-month-old son Aarav develops a fever one evening, she rushes him to what online reviews proclaimed as the city’s “best pediatric facility.” What should have been a simple viral fever consultation becomes a nightmare. They perform unnecessary blood tests, fabricate complications, order expensive scans, and present her with lab reports claiming Arjun has a rare genetic blood disorder requiring immediate treatment costing Rs. 80,000. When Priya questions the diagnosis, seeking a second opinion, they threaten to call child services, claiming she is endangering her son by refusing treatment.

These are not isolated incidents from crime thrillers. These are real cases that have landed on my desk.

In the first part of this two-part lecture series, we will dissect the dark anatomy of medical fraud. You will learn to recognise the statistical red flags that expose even the most sophisticated fraudsters. You will master investigative techniques that can uncover fraud hidden in medical data.

In Part II, we will learn how to draft a consumer commission complaint using AI (step-by-step) that delivers compensation.

By the end of this session, you will possess a complete legal toolkit for representing patients, hospitals and legitimate insurers in healthcare fraud cases.

Understand the types of healthcare fraud

I have learned that healthcare fraudsters are like criminal specialists, each with their own twisted expertise:

Phantom billing: These are the ghosts of the medical world. They charge for treatments that exist only in their imagination. I caught one cardiologist who billed insurance for 30 heart surgeries in a single month, impressive, considering he was on vacation in Goa for two weeks.

Upcoding: The medical equivalent of ordering a basic coffee and getting charged for a premium espresso with gold flakes. A simple blood test becomes a complex analysis, and a routine checkup transforms into a comprehensive cardiac evaluation.

Unbundling: Imagine buying a car and getting separate bills for each screw, bolt, and wire. These fraudsters take a single procedure and split it into dozens of billable components. One appendectomy becomes 15 different charges.

Fake insurance claims: The classic con. They create entire fictional patients, complete with believable medical histories, symptoms, and treatments. I once uncovered a clinic that had 200 “patients” with identical birthdays; they would run out of creativity.

Kickback schemes: The “you scratch my back, I will scratch yours” of healthcare fraud. Labs pay doctors for unnecessary referrals, pharmaceutical companies bribe doctors for specific prescriptions, and imaging centres offer vacations for MRI orders.

Ghost patients: Perhaps the most disturbing, claiming reimbursements for people who never existed or, worse, who are deceased. I have seen death certificates used as props in elaborate billing schemes.

Real story: In 2022, a Thane insurance company came to me with a puzzle. A small suburban hospital was claiming to perform more chemotherapy sessions than the All India Institute of Medical Sciences. When we investigated, we found 50 identical treatment records, same drugs, same doses, same treatment dates. The “patients”? All fabrications. The hospital’s defence was that it was a “clerical error.” Right. A Rs. 2 crore clerical error.

What provisions are contravened?

When dealing with healthcare fraud cases, you are never short of legal weapons. These crimes violate so many laws that you can hit fraudsters from multiple angles:

- Section 318 (Cheating): Your workhorse. When a hospital bills for procedures they never performed, this section becomes their worst nightmare. It is cognisable, which means police can arrest without a warrant.

- Section 336 (Forgery): Perfect for fake discharge summaries, fabricated lab reports, or altered prescriptions. I once nailed a clinic director who was personally signing off on fake medical certificates for insurance claims.

- Section 61 (Criminal conspiracy): When multiple people are involved, and in healthcare fraud, they usually are. The doctor, the billing manager, and the TPA executive are all part of the conspiracy.

Real example: A Delhi dialysis centre was billing Rs. 5 lakh monthly for sessions that never happened. We used section 318 to get the police moving, and the forensic audit revealed fabricated patient logs. Result: three arrests and Rs. 3 lakh recovered for the insurance company.

Section 7 (Public servant bribery): Essential when government hospital officials are involved. I exposed a central government health scheme official in Mumbai who was approving ghost patient claims for a 10% commission. His downfall? He got greedy and approved claims for more patients than the hospital could physically accommodate.

- Section 66C (Identity theft): When fraudsters steal patient identities to file claims. One gang I prosecuted had a database of 5,000 stolen Aadhaar numbers they used to create fake patients.

- Section 66D (Cheating by personation): For fake hospital websites or impersonation of legitimate medical institutions.

- Section 43 (Unauthorised access): When they hack into hospital systems to alter records or steal patient data.

- Legislation on insurance

- Section 14: Essential when hospitals refuse to cooperate with investigations. I caught a chain of hospitals in Delhi systematically deleting patient records whenever the IRDAI sent inspection notices. Their mistake? They used the same IT vendor, which kept backup logs of all deletions.

- Section 32C (Insurance to vulnerable sections): With the help of this provision, I exposed a network that specifically targeted illiterate tribal patients in Odisha, filing fake claims using their Aadhaar cards. The scheme unravelled when they claimed the same patient had heart surgery in three different states simultaneously.

- Section 102: Non-compliance with insurance regulations. I prosecuted an insurer whose automated system flagged 847 suspicious claims from one hospital, but management overrode the alerts for six months. Their greed cost them their license.

- Regulation 9: Unfair claim settlement practices- When insurers approve fraudulent claims while rejecting legitimate ones. I discovered a pattern where one insurer was approving 90% of claims from hospitals paying them kickbacks while rejecting 60% of claims from honest hospitals.

- Regulation 8: Misrepresentation of policy terms. I caught a hospital billing for “emergency cardiac procedures” when patients had only come for routine check-ups. They were exploiting policy language that did not clearly define “emergency.”

- Regulation 13 & 16: Breach of surveyor code of conduct- I flipped a corrupt surveyor who was rubber-stamping inflated claims without site visits. His downfall? He approved a Rs. 15 lakh claim for a hospital that had been demolished six months earlier.

- Failure to prevent money laundering- When fraud proceeds are being laundered- I traced a network where claim money was flowing through 12 shell companies before reaching the fraudsters. The insurer’s failure to report these obvious suspicious transactions made them liable for the entire scheme (e.g., funnelling kickbacks through fake claims).

Red flags

Fraud leaves footprints; you just need to know where to look. Whether you are building a case or defending against accusations, these patterns tell the story:

- For prosecutors/complainants:

The statistical impossibility: A single doctor performing more procedures than humanly possible. I once found a surgeon who claimed to do 12-hour operations while simultaneously being in the outpatient clinic.

The carbon copy syndrome: Identical diagnostic codes, identical treatment plans, identical billing amounts. Real medicine is not that uniform.

The holiday hero: Procedures performed on days when the hospital was officially closed. One clinic I investigated was performing “emergency surgeries” during Diwali when their operating theatre was locked for renovations.

The prescription pattern: Doctors who always prescribe the most expensive drugs or always refer to the same lab. Medicine has variations; kickback schemes don’t.

Personal story: I was reviewing claims for a Mumbai hospital when something caught my eye. They had submitted 47 claims for appendectomies in a single month, all performed by the same surgeon, all with identical complications, all resulting in identical billing amounts. When we investigated, we found the surgeon had been copying and pasting the same operation notes for months.

- For defence lawyers:

Q: My hospital client is accused of upcoding. The evidence looks bad. What is my angle?

A: Look for system errors first. I defended a Nagpur clinic where the billing software was automatically upgrading routine visits to complex consultations due to a coding error. Intent matters; prove it was a technological malfunction, not deliberate fraud.

Q: Police seized our EMR systems without following proper protocol. Can I challenge this?

A: Absolutely. Demand chain-of-custody documentation. I got a major case dismissed because investigating officers could not prove they had not tampered with digital records during seizure.

Q: They are alleging kickbacks, but the evidence is circumstantial. Weak points?

A: Focus on the lack of direct financial evidence. Frequent referrals to a particular lab are not criminal without proof of quid pro quo arrangements.

Investigative techniques

Building a healthcare fraud case is like performing surgery; it requires precision, patience, and the right tools. Let me walk you through my methodology using a real case:

Step 1: Evidence gathering

This was in 2023, when a young entrepreneur, Purav, approached me. His insurance company had rejected his wife’s cancer treatment claim, citing a pre-existing knee replacement surgery he supposedly had, a surgery that existed only in fraudulent billing records.

Document summons: Using section 94 of Bharatiya Nagrik Suraksha Sanhita 2023, we obtained Purav’s complete medical records from the hospital. The knee surgery appeared in billing records, but nowhere in actual medical files.

Third-party discovery: We summoned the Third Party Administrator (TPA) handling the claims. Their records showed payments for procedures that were not reflected in the hospital’s medical notes.

Witness statements: Purav’s family doctor provided an affidavit confirming he had never referred Purav for knee surgery. Fortunately, a former hospital billing clerk turned whistleblower revealed the systematic fraud.

Step 2: Forensic analysis

Expert engagement: We hired a healthcare forensic accountant who found timestamp anomalies. Purav’s “surgery” was billed before his hospital admission records were created.

Pattern analysis: The accountant discovered the hospital had a suspicious 89% rate of high-value procedures, compared to the regional average of 23%.

Metadata examination: EMR (Electronic Medical Record) systems leave digital fingerprints. We proved that a billing clerk had backdated entries to create fake surgical records.

Step 3: Digital evidence preservation

Hashing protocols: All digital evidence was cryptographically hashed to ensure integrity for court presentation.

Cryptographically hashed is a process that ensures the integrity and authenticity of digital evidence by providing proof that any digital evidence is the same as the original since its upload. If any alteration is made to the evidence, the system generates a new hash value that does not match the original one.

Chain of custody: We meticulously documented every person who handled the evidence, preventing defence challenges.

Mirror imaging: With court permission, we created exact copies of the hospital’s servers to preserve evidence before it could be altered.

Step 4: Regulatory interface

IRDAI complaint: We filed a formal complaint with the insurance regulator, triggering their investigation powers.

The state health authority reported the hospital to the state medical authorities for license violations.

Result: Purav’s wife got her cancer treatment coverage restored, the hospital paid Rs. 5 lakh in penalties, and three employees faced criminal charges.

Police and consumer complaints: what they must contain

- Police complaint contents

A healthcare fraud police complaint must tell a story that even a non-medical officer can understand:

- Complainant details: Complete identification, including occupation, helps establish credibility

- Accused details: Hospital name, key personnel, digital identifiers, addresses

- Incident chronology: Timeline with specific dates, amounts, and fraudulent acts

- Legal violations: Cite relevant BNS sections, IT Act provisions if digital fraud is involved

- Evidence: List all attachments: bills, medical records, witness statements, expert reports

You may refer to my article on matrimonial fraud for a quick reference on how to draft a police complaint that initiates action.

Example: Purav’s complaint included fake billing records, expert analysis showing impossibilities, and witness statements. The clear presentation led to immediate FIR registration.

- Consumer complaint contents

For civil remedies under the Consumer Protection Act 2019:

- Header: Proper addressing to the appropriate consumer forum based on claim value

- Parties: Clear identification of all respondents: hospital, insurance company, TPA

- Facts: Detailed narrative of fraud, financial impact, and harassment suffered

- Legal grounds: Cite CPA 2019 provisions, service deficiency, unfair trade practices

- Evidence: Comprehensive documentation, including correspondence showing deficient service

- Relief sought: Specific monetary compensation, costs, interest calculations

- Affidavit: Sworn verification of complaint accuracy

Who to contact when medical fraud strikes

When healthcare fraud hits, knowing exactly who to call can mean the difference between getting justice and watching criminals walk free. Here is your no-nonsense roadmap based on real cases I have handled:

1. Your local police station

When to go: When someone has clearly stolen money through fake medical bills, forged documents, or identity theft. This covers most healthcare fraud scenarios.

What they handle: Criminal charges under sections 318 (cheating), 336 (forgery) of BNS 2023, or IT Act violations when digital fraud is involved.

How to approach: Walk in with a complaint and printed copies of everything: fake bills, real medical records, bank statements. Tell them someone stole money by creating fake medical treatments. Keep it simple, avoid medical and legal jargon.

2. Cybercrime cell

When to go: If computers, apps, or digital systems were used to commit the fraud. Think hacked medical records, fake hospital websites, or tampered electronic prescriptions.

What they handle: Identity theft, impersonation, and unauthorised access to medical databases.

How to approach: File online at cybercrime.gov.in or visit your nearest cybercrime police station. Upload screenshots, transaction IDs, email headers, anything digital that proves the fraud.

3. IRDAI (insurance watchdog)

When to go: If your insurance company wrongly denied claims, if someone filed fake claims using your policy, or if hospitals are collaborating with insurers to cheat.

What they handle: Insurance fraud, unfair claim settlements, policy misrepresentation under IRDAI regulations.

How to approach: Use their Bima Bharosa portal (bimabharosa.irdai.gov.in) or call 155255. They are surprisingly responsive and have real power to make insurers behave.

4. Medical Council

When to go: If a doctor prescribed unnecessary treatments for kickbacks, performed procedures you did not need, or violated medical ethics.

What they handle: Professional misconduct, license suspension, and ensuring doctors follow medical ethics.

How to approach: Contact your State Medical Council or the National Medical Commission. Submit copies of prescriptions, bills, and witness statements showing unethical behaviour.

5. Consumer forums

When to go: When you want compensation, refunds, or damages. This is your civil remedy route, not criminal punishment, but financial justice.

What they handle: Service deficiency, unfair practices, and monetary compensation under the Consumer Protection Act 2019.

How to approach: File at the District Consumer Forum (for claims under Rs. 1 crore). Bring bills, correspondence with the hospital/insurer, and an affidavit. Filing fees are minimal.

6. Anti-Corruption Bureau/CBI (For government hospital fraud)

When to go: If government hospital staff or officials are involved in taking bribes or approving fake claims in government schemes.

What they handle: Corruption in public sector healthcare under the Prevention of Corruption Act 1988.

How to approach: File with your state’s Anti-Corruption Bureau or CBI regional office. Bring evidence of bribery, fake approvals, or misuse of government healthcare funds.

7. State health department (For hospital license issues)

When to go: If a hospital or clinic is operating without proper licenses, if they are providing substandard care, or if you want an official audit of their practices.

What they handle: Hospital licensing, quality standards, and regulatory compliance under the Clinical Establishments Act 2010.

How to approach: Contact your state’s Directorate of Health Services. They can order surprise inspections and have the power to shut down non-compliant facilities.

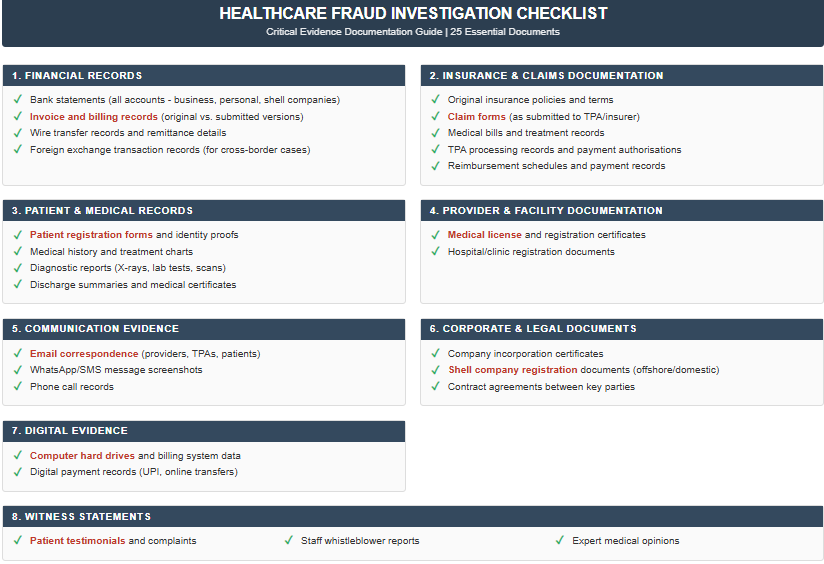

Which documents should you keep ready?

Before you walk into any police station or consumer forum, make sure you have these documents organised and ready. Missing even one crucial piece can derail your entire case:

These 25 documents form the backbone of any solid healthcare fraud case. Everything else is supporting evidence: nice to have, but not make-or-break for prosecution.

Pro tips

Start with multiple approaches: Do not put all your eggs in one basket. File criminal complaints AND consumer cases simultaneously. The pressure from different directions often forces quick settlements.

Document everything first: Before you approach anyone, gather all evidence. Once investigations start, hospitals often “lose” records or claim computer crashes.

Follow up religiously: Government agencies move at their own pace. Visit every two weeks, call regularly, and escalate to supervisors when progress stalls.

Use media strategically: Healthcare fraud gets public attention. Sometimes, a well-placed news story moves bureaucrats faster than legal notices.

Do not get overwhelmed by jurisdiction: If you are not sure which agency handles what, start with the local police and consumer forum.

Keep it simple: Police officers are not doctors. Avoid medical jargon in complaints. Focus on clear financial fraud rather than complex medical explanations.

Leverage regulators: IRDAI and medical councils have investigation powers that can freeze operations faster than criminal courts. Use them.

Expert testimony: Always hire medical and forensic experts. I have never won a complex healthcare fraud case without expert analysis of billing patterns and medical appropriateness.

Remember: Each agency has different powers and different timelines. Police can arrest people, IRDAI can force insurance payouts, medical councils can suspend licenses, and consumer forums can award compensation. Use them all strategically, and do not let anyone tell you that healthcare fraud is “too complicated” to prosecute. It is not, it just requires knowing which doors to knock on.

The key is acting fast, documenting everything, and not giving up when the first person you approach does not understand the problem. Healthcare fraud thrives in silence and confusion. Your job is to make noise in all the right places until someone listens.

Conclusion

Healthcare fraud is not just white-collar crime; it is the predatory exploitation of people when they are fighting for their lives. Every fake bill, every unnecessary procedure, every phantom patient represents someone’s shattered trust in the system meant to heal them. The techniques I have shared today, from spotting statistical impossibilities to navigating the maze of regulatory agencies, are not just professional skills. They are tools of justice for the Mrs. Desais and Rati Sharmas, whose stories opened this lecture. When you master these investigative methods, you become the last line of defence between vulnerable patients and criminals.

But investigation is only half the battle. In Part II, my junior colleague Advocate Shanaya Mehta will show you how to weaponise your evidence through AI-enhanced complaint drafting. You will learn to transform complex medical fraud into winning legal arguments that consumer forums cannot ignore. Because in this fight, it is not enough to catch the fraudsters, you have to make them pay.

FAQs

At the end of the first part, the questions came fast and furious.

- Can AI doctors commit fraud?

Absolutely. AI-powered diagnostic systems have been manipulated to generate false positive results, leading to unnecessary treatments and inflated billing. In one case, radiologists programmed AI to “detect” tumours that did not exist, triggering expensive cancer treatments. The scariest part? AI fraud is nearly impossible for patients to detect since the technology appears legitimate and sophisticated.

- Can your own doctor sell your medical identity?

Yes, and it is more common than you think. Medical identity theft involves doctors selling patient information to billing companies, who then submit fake claims using real patient details. Victims often discover the fraud when they are denied coverage for legitimate treatments because their “medical history” shows they have already received maximum benefits for conditions they never had.

- What constitutes criminal liability in AI-powered healthcare fraud?

When artificial intelligence systems are deliberately manipulated to generate false diagnoses, both the programmers and supervising physicians face criminal charges. The legal challenge lies in proving intent: was the AI malfunction accidental or deliberate? Courts have established that radiologists who program AI to detect non-existent tumours for billing purposes face the same fraud penalties as traditional diagnostic fraud. The key evidence: system logs showing manual overrides and pattern analysis of false positives correlating with billing cycles.

- How do courts handle cases involving deceased patients in billing fraud?

Billing for dead patients creates multiple criminal charges: healthcare fraud, identity theft, and often PMLA violations for money laundering. The prosecution must establish not just the fraudulent billing but also knowledge of death and intent to defraud. Medical records showing continued “treatment” after verified death dates provide the strongest evidence. Defence attorneys often argue administrative delays, making accurate death certification timestamps crucial for prosecution.

- What are the legal remedies for medical identity theft victims?

Victims of medical identity theft face a complex legal landscape. Civil remedies include correcting fraudulent medical records, recovering financial damages, and obtaining injunctive relief against further misuse. Criminal prosecution focuses on the perpetrators, often medical professionals who sold patient information. The challenge: proving the victim did not consent to the treatments. Insurance fraud statutes provide the strongest prosecution tools, with penalties ranging from 3-10 years imprisonment.

- How do prosecutors prove “phantom patient” schemes in court?

Phantom patient prosecutions require proving that patients never existed or never received claimed treatments. Evidence includes cross-referencing patient attendance with hospital CCTV footage, analysing appointment scheduling patterns, and verifying patient contact information. The prosecution must demonstrate systematic creation of false identities rather than isolated documentation errors. Digital forensics of hospital information systems often reveals bulk patient creation and impossible treatment timelines.

- What is the legal standard for proving “upcoding” versus legitimate billing?

Upcoding cases hinge on proving intentional misrepresentation versus reasonable medical judgment. Courts apply the “reasonable physician” standard: would a competent doctor have coded the procedure differently? Prosecution requires establishing a pattern of systematic overcharging rather than isolated incidents. Expert medical testimony becomes crucial, and statistical analysis showing billing patterns significantly above peer averages strengthens the case. The defence often argues medical complexity and patient-specific factors.

- What criminal charges apply when hospitals provide substandard care while billing for premium services?

This constitutes both healthcare fraud and potentially criminal negligence or endangerment. Prosecutors can pursue fraud charges for the billing deception and separate charges for patient harm. The legal complexity increases when patients suffer adverse outcomes: prosecutors must prove the substandard care was intentional rather than malpractice. Contract fraud charges may also apply if hospitals violated specific service agreements with insurers.

- How do money laundering laws apply to medical equipment fraud?

Medical equipment fraud often triggers prosecution under the Prevention of Money Laundering Act when proceeds are layered through shell companies. The challenge lies in proving the equipment transactions were designed to obscure illegal proceeds rather than legitimate price variations. Courts examine whether equipment prices fall within reasonable market ranges and whether purchasers conducted legitimate due diligence. Serial transactions involving the same equipment through multiple entities create strong money laundering evidence.

- What are the estate liability issues when deceased doctors’ credentials are used fraudulently?

Using deceased physicians’ credentials creates complex liability questions. The estate typically bears no criminal responsibility unless family members were involved. However, civil liability may exist if the estate failed to notify relevant authorities of the death. Medical boards face potential negligence claims for failing to maintain current databases. Insurance companies can seek recovery from estates if beneficiaries received proceeds from fraudulent claims.

- How do international jurisdiction issues complicate medical tourism fraud prosecutions?

Medical tourism fraud creates complex jurisdictional challenges when treatments occur abroad but billing targets domestic insurers. Prosecution requires proving that conspiracy elements occurred within Indian jurisdiction, typically the planning, billing submission, or money transfer phases. International cooperation becomes essential for evidence gathering, including medical records from foreign facilities. Extradition treaties may apply to defendants who flee abroad, but civil asset recovery often proves more practical than criminal prosecution.

Allow notifications

Allow notifications