Learn how to use AI to draft investment-grade financial disclosures under section 134 of the Companies Act, 2013. In Part 3 of our board report series, discover how to turn raw financial data into compelling narratives for institutional investors, covering revenue growth, reserves, dividends, and market positioning. See how AI tools like Claude balance legal compliance with strategic financial storytelling.

About this series

This is Part 3 of our 8-part series “How you can use AI to draft a board report under section 134: Financial performance and capital management.”

Complete series overview:

- Part 1: Getting Started

- Part 2: Building the foundation (Group 1)

- Part 3: Financial performance and capital management (Group 2) ← You are here

- Part 4: Directors’ statements and professional judgment (Group 3)

- Part 5: External stakeholders and audit relations (Group 4)

- Part 6: Risk management and CSR disclosures (Group 5)

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – real-time board report Creation

Haven’t started from Part 1? No problem! This article works standalone, but you will get more value by reading the series sequentially.

What you will learn in this article: Today, Arjun and Ms. Rao tackle financial storytelling with AI. You will see how they transform Nova AgriTech’s impressive growth numbers into professional investor communication that meets legal requirements while building confidence.

Key characters:

- Arjun Sharma: Junior lawyer learning AI tools for legal work

- Ms. Priya Rao: Senior partner, now collaborative and contributing actively

- Nova AgriTech: Agri-tech client with 42% revenue growth, strong margins, needing a sophisticated financial narrative

Quick recap: Where we are

[For series readers: Skip to “Today’s Focus” below] [For new readers: Here’s what happened so far]

What happened previously: Ms. Rao was initially sceptical about using AI for legal work. Arjun demonstrated that Claude understands section 134 legal requirements and can organise them systematically. In Part 2, they successfully created professional Group 1 governance content that impressed Ms. Rao with its quality and strategic positioning.

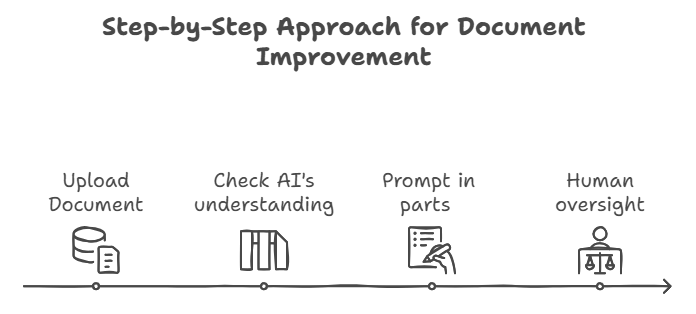

The step-by-step approach we use:

- Upload comprehensive company information (so Claude understands the business)

- Test Claude’s understanding (before asking it to draft anything)

- Improve drafts step by step (refine content through focused prompts)

- Review everything carefully (lawyer oversight ensures accuracy)

Groups completed:

- Group 1: Foundational structure & governance (completed in Part 2)

- Group 2: Financial performance & capital management ← Today’s focus

- Remaining Groups: 3-6 to be covered in subsequent parts

Nova AgriTech quick company profile:

- Agri-tech company with 42% revenue growth to ₹45.2 crores

- Improving margins from 19% to 23%

- Strong balance sheet with strategic reserve accumulation

Today’s focus: Group 2 – financial performance & capital management

In this article, you will watch Arjun and Ms. Rao handle the financial complexity that institutional investors care about most. They will transform numbers into strategic narratives.

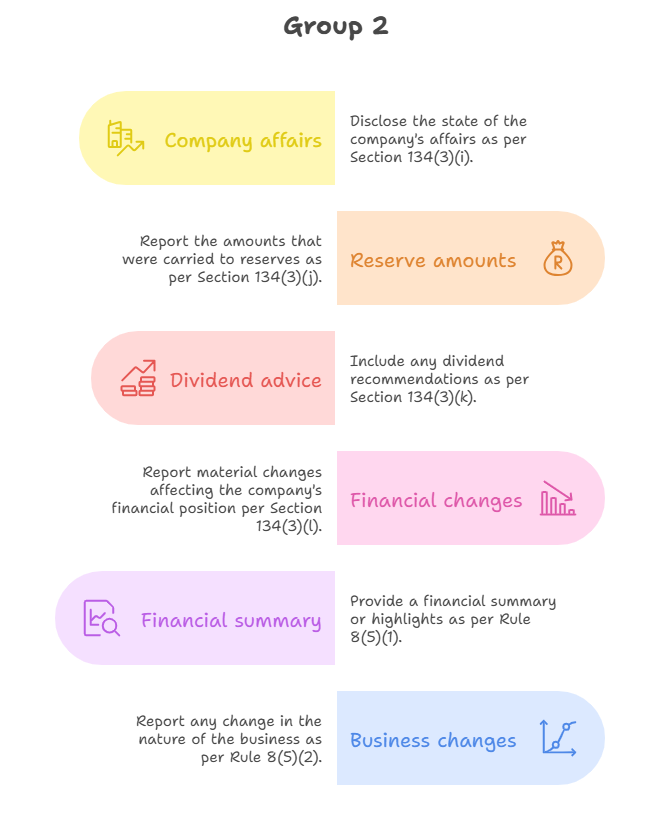

Group 2 requirements we are covering:

- Section 134(3)(i): State of company’s affairs

- Section 134(3)(j): Amounts carried to reserves

- Section 134(3)(k): Dividend recommendations

- Section 134(3)(l): Material changes affecting financial position

- Rule 8(5)(1): Financial summary or highlights

- Rule 8(5)(2): Change in nature of business

By the end, you will understand:

- How to create financial context documents for sophisticated AI analysis

- Techniques for balancing transparency with strategic positioning

- Ways to transform compliance disclosures into investor confidence builders

Moving ahead to make financial disclosure in the board report using AI

“That Group 1 content exceeded my expectations,” Ms. Rao said, reviewing their completed governance section.

“But now we need to see if Claude (AI) can understand and write in a financial context.”

She pulled out Nova AgriTech’s financial statements and quarterly reports.

The numbers told an impressive story:

- 42% revenue growth,

- margin expansion from 19% to 23%,

- strategic investments in R&D.

It would be interesting to see if Claude can translate these into professional board report language.

“Based on what we learned in Group 1, I think we should create a comprehensive financial intelligence document before we ask Claude to draft anything,” Ms. Rao suggested. “The governance content worked so well because Claude understood Nova’s complete context.”

Arjun nodded, pleased to see Ms. Rao actively contributing ideas.

“Exactly. Group 2 requires Claude (AI) to understand not just the current numbers, but the strategic logic behind Nova’s financial decisions.”

“Nova’s institutional investors need to see that management is not just growing revenue – they are doing it while building sustainable competitive advantages,” Ms. Rao added, examining the three-year progression.

Collecting and summarising financial information for AI

“Group 2 is more complex than governance facts,” Arjun explained, opening a new document. “Claude needs to understand Nova’s financial journey, strategic investments, and the market context that makes these results impressive.”

He began typing a comprehensive financial background:

Nova AgriTech Financial Summary Document – FY 2024-25 Board Report

Three-Year Financial Evolution:

- FY 2022-23: ₹18.5 crores revenue, ₹2.96 crores net profit (16% margin)

- FY 2023-24: ₹31.8 crores revenue, ₹6.04 crores net profit (19% margin)

- FY 2024-25: ₹45.2 crores revenue, ₹8.7 crores net profit (23% margin)

Strategic Investment Profile:

- R&D spending increased 65% to ₹4.2 crores (9.3% of revenue)

- Technology infrastructure: ₹2.8 crores IoT sensor development

- Market expansion: ₹1.9 crores, field operations setup

- Human capital: Technical team expanded from 45 to 78 professionals

Capital Allocation Strategy:

- Reserves accumulation: ₹6.8 crores retained for expansion

- Dividend distribution: ₹1.7 crores (₹2 per share) – 20% of net profit

- Working capital optimisation: Inventory days reduced from 45 to 32

- Debt management: Reduced debt-to-equity from 0.3 to 0.15

Market Context:

- Precision agriculture market growing 12% annually in India

- Nova’s growth rate (42%) significantly outpacing the market

- Strategic partnerships: Haryana Agricultural Department (₹25 crores, 3-year)

- Technology leadership in IoT sensor integration

Post-Year Developments (April-May 2025):

- Q1 FY 2025-26 revenue: ₹13.8 crores (38% growth over Q1 FY 2024-25)

- Two new state partnerships under negotiation (₹40 crores potential)

- Series B funding discussions initiated with existing investors

- Technology patent applications filed for next-generation sensors

Ms. Rao reviewed the financial intelligence document.

“This captures not just the numbers, but the strategic thinking behind every financial decision. Revenue growth driven by strategic partnerships, margin improvement through technology investments, and reserve accumulation for calculated expansion.”

“Exactly what Claude needs to write sophisticated financial analysis rather than basic compliance content,” Arjun agreed.

Can AI write a strategic financial narrative? Here is what happened

Following their step-by-step approach, Arjun uploaded the financial summary document and began testing Claude’s understanding:

First prompt:

Based on the Nova AgriTech financial summary document as uploaded, analyse the company’s three-year financial trajectory and current strategic position.

Focus on:

(1) Key performance drivers and strategic achievements,

(2) Capital allocation effectiveness and philosophy,

(3) Market positioning and competitive advantages demonstrated through financial results,

(4) Forward-looking strategic positioning.

Write this as a sophisticated financial analysis suitable for institutional investors who understand both technology sector dynamics and agricultural market opportunities.

Click here to see the complete conversation and here to see Claude’s response in pdf.

Ms. Rao read Claude’s response with growing amazement.

“This is extraordinary financial analysis,” she said, scrolling through the comprehensive response.

“Look at this executive summary: ‘Nova AgriTech demonstrates exceptional execution of a precision agriculture technology strategy, achieving a 144% revenue compound annual growth rate over three years while maintaining disciplined margin expansion and strategic capital deployment.'”

“The sophistication is immediately apparent,” Arjun observed.

“Claude calculated the CAGR as 56% and positioned it as ‘4.7x market outperformance’ compared to India’s 12% precision agriculture market growth. That’s institutional investor-grade analysis.”

Ms. Rao continued reading.

“I am particularly impressed with how Claude identified strategic patterns. Listen to this: ‘The acceleration pattern shows consistent momentum: 72% growth in FY 2023-24 followed by 42% in FY 2024-25, suggesting the company is maintaining velocity while scaling operations.'”

“And notice the sophisticated capital allocation analysis,” Arjun added.

“Claude wrote: ‘Nova’s capital allocation reflects sophisticated understanding of technology lifecycle management and market positioning requirements. R&D spending at 9.3% of revenue positions above typical technology companies, indicating commitment to innovation leadership.'”

Ms. Rao leaned back, clearly impressed.

“This analysis rivals the quality of investment banking pitch books I have seen. Claude identified investment merits like ‘demonstrated technology commercialisation with 4.7x market outperformance’ and ‘sustainable competitive advantages through IoT sensor integration expertise.'”

But as she continued reading, Ms. Rao identified the gap.

“Claude’s financial analysis is exceptional – probably better than most CFO presentations I’ve seen. But notice what’s missing?”

Arjun anticipated her observation.

“No section 134 compliance structure. No mandatory disclosure formatting. Claude gave us a brilliant strategic analysis, but not legal compliance documentation.”

“Exactly. We have investment-grade financial intelligence, but we need to structure it within Companies Act requirements.”

Prompting to create the first draft

“This is where strategic prompting becomes powerful,” Arjun explained.

“Claude has demonstrated sophisticated financial analysis capability. Now we guide it to structure that analysis within mandatory disclosure requirements.”

Second prompt:

Using your excellent financial analysis, now structure Nova AgriTech’s Group 2 financial disclosures to meet Section 134(3) and Rule 8 requirements.

Structure as:

(1) State of Company’s Affairs [Section 134(3)(i)],

(2) Amounts Carried to Reserves [Section 134(3)(j)],

(3) Dividend Recommendation [Section 134(3)(k)],

(4) Material Changes [Section 134(3)(l)],

(5) Financial Summary/Highlights [Rule 8(5)(1)],

(6) Business Evolution [Rule 8(5)(2)].

Maintain the sophisticated financial analysis tone while ensuring complete legal compliance.

Click here to see the complete conversation, and here to see Claude’s response in PDF.

The structured response was remarkable.

Claude had taken its sophisticated financial analysis and organised it precisely within legal compliance requirements while maintaining investment-grade communication standards.

“This is good stuff,” Ms. Rao said, reviewing the structured disclosure sections.

“Look at how Claude handled the State of Affairs section: ‘Your Company has delivered exceptional financial performance during FY 2024-25, reinforcing its position as a technology leader in India’s precision agriculture sector.'”

“The legal compliance integration is seamless,” Arjun observed.

“Claude structured each section with proper statutory references while maintaining the strategic narrative. For reserves, it wrote: ‘During FY 2024-25, your Company retained ₹6.8 crores in reserves after appropriating ₹1.7 crores for dividend distribution to shareholders. This reserve accumulation reflects our strategic approach to capital allocation.'”

Ms. Rao continued scrolling.

“I am particularly impressed with the dividend recommendation section. Instead of dry compliance language, Claude positioned it strategically: ‘Your Directors are pleased to recommend a final dividend of ₹2 per equity share for FY 2024-25, representing a total dividend distribution of ₹1.7 crores.'”

Ms. Rao nodded enthusiastically.

“The financial highlights section includes sophisticated metrics. Look at this table Claude created showing growth rates, strategic significance, and competitive advantages for each metric.”

But she paused, considering the overall positioning.

“While this meets all legal requirements and maintains sophisticated analysis, I think we can enhance it further for maximum strategic impact with institutional investors.”

Enhancing the language

“This is where Claude’s iterative refinement capability becomes exceptional,” Arjun explained.

“We have a legally compliant, professionally written financial disclosure. Now we can guide Claude toward investment-grade strategic emphasis.”

Third prompt:

Enhance the Group 2 financial disclosures to more strategically emphasise Nova AgriTech’s financial excellence and competitive positioning for institutional investors.

Specifically:

(1) Position the 42% revenue growth within the context of outpacing market growth rates and gaining market share,

(2) Emphasise the margin expansion (16% to 19.2%) as evidence of operational excellence and technology leverage,

(3) Frame the reserve accumulation and dividend balance as sophisticated capital allocation that enables growth while rewarding shareholders.

(4) Connect the financial performance to strategic competitive advantages that position Nova for continued market leadership.

Maintain full legal compliance while elevating the strategic business communication to institutional investor standards.

Click here to see the complete conversation, and here to see Claude’s response in PDF.

The enhancement was transformational.

Claude had elevated the already strong financial disclosure into a compelling investment narrative while maintaining complete legal compliance.

“This is investment banking-quality financial communication,” Ms. Rao said, reading through the enhanced version.

“Look at this opening for State of Affairs: ‘Your Company has delivered exceptional financial performance during FY 2024-25, demonstrating clear market leadership and operational excellence in India’s precision agriculture technology sector.'”

“The market positioning language is particularly powerful,” Arjun observed.

“Claude enhanced it to: ‘The Company achieved revenue of ₹45.2 crores in FY 2024-25, representing a robust 42% growth that significantly outpaces India’s precision agriculture market growth of 12% annually. This 3.5x market outperformance demonstrates systematic market share capture.'”

Ms. Rao continued reading with growing enthusiasm.

“The margin expansion narrative is brilliantly positioned. Listen to this: ‘More significantly, your Company has demonstrated exceptional operational leverage with margins expanding from 16% in FY 2022-23 to 23% in FY 2024-25—a 320 basis point improvement that showcases the scalability of our technology-enabled business model.'”

Human review

“Let us evaluate this systematically against our professional standards,” Ms. Rao said, applying her comprehensive review framework.

“AI can produce excellent content, but human lawyers must verify accuracy, consistency, and appropriateness,” said Arjun.

“The human review catches things Claude might miss,” Arjun explained.

“For instance, if Claude had incorrectly stated the dividend amount or misaligned the strategic narrative between groups, I would immediately correct it.”

“What would you do if you found an inconsistency?” Arjun asked.

“Simple – give Claude another prompt to fix it,” Ms. Rao replied.

“For example, if I noticed Claude incorrectly calculated the dividend yield or misrepresented the reserve accumulation strategy, I would prompt: ‘Please review your dividend recommendation section. The dividend per share should be ₹2 on 85,00,000 shares, totaling ₹1.7 crores, not the amount you stated. Also ensure the reserve accumulation amount of ₹6.8 crores is correctly positioned as strategic capital allocation for expansion rather than excess cash holding.'”

“The key insight,” she continued, “is that AI collaboration requires active human oversight. Claude excels at organisation, language, and consistency, but lawyers must verify legal accuracy, strategic appropriateness, and factual correctness.”

What we have accomplished

“In about 30 minutes, we have created investment-grade financial disclosures that integrate quantitative analysis with strategic narrative,” Arjun reflected.

Time comparison:

- Traditional approach: 6-8 hours for this level of financial disclosure analysis

- AI-assisted approach: 30 minutes, including iterative refinement and quality review

- Quality level: Investment-grade communication maintained throughout

Key benefits we have confirmed:

- Multi-document context integration enables sophisticated analysis

- Quantitative-qualitative synthesis produces professional financial narratives

- Strategic enhancement achieves institutional investor communication standards

- Foundation building creates a coherent narrative progression from Group 1

Ms. Rao studied their completed Group 1 and Group 2 sections.

“What strikes me most is the narrative coherence. Group 1’s governance foundation flows naturally into Group 2’s financial performance story.”

“That is the systematic advantage,” Arjun explained.

“The governance structures described in Group 1 become the management systems that delivered Group 2’s financial results. It is not fragmented compliance – it is integrated business communication.”

Key takeaways:

- Financial intelligence documents enable sophisticated AI analysis beyond basic numbers

- Strategic financial storytelling requires understanding three-year patterns and market context

- Legal compliance structure can maintain sophisticated financial analysis quality

- Professional financial communication builds naturally on governance foundations

Progress Check: You’ve now seen how to handle complex financial analysis and strategic positioning with AI. This financial foundation prepares you for Group 3’s professional judgment communications, where we’ll tackle Directors’ Responsibility Statements and board evaluations.

Next Steps

If you are following the series:

- Next: Part 4 covers Group 3 (Directors’ Statements and Professional Judgment)

- Previous: Part 2 covered Group 1 (Building the Foundation)

If you are new to the series:

- Start from Part 1 for the complete methodology

- Jump to Part 8 to see the live demonstration

Want to try this yourself?

- Create comprehensive financial intelligence documents before prompting

- Test Claude’s analytical capability before requesting structured disclosures

- Use strategic enhancement to achieve institutional investor communication standards

Complete article series

- Part 1: Getting started

- Part 2: Building the foundation (Group 1)

- Part 3: Financial performance and capital management (Group 2) ← You are here

- Part 4: Directors’ statements and professional judgment (Group 3)

- Part 5: External stakeholders and audit relations (Group 4)

- Part 6: Risk management and CSR disclosures (Group 5)

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – real-time board report creation

This financial performance foundation sets the stage for the professional judgment communications covered in Part 4, where we’ll see how Claude handles subjective assessments and director accountability disclosures.

Allow notifications

Allow notifications