This guide shows you how to navigate grievance redressal systems when your insurance claim was wrongfully denied, use section 45 to beat pre-existing condition denials, and get companies to pay interest for delays. You will learn to structure your complaints and when to use an ombudsman versus consumer courts for faster redressal. So, if you are an insurance lawyer or a policyholder, this article will tell you what exactly you need to know.

Introduction

“They are calling my heart attack a pre-existing condition!”

Arjun Nair walked into my office looking like a man who had been betrayed twice, first by his heart, then by his insurance company.

“I had a massive heart attack three months ago,” he said, settling heavily into the chair across from my desk. “Emergency surgery, ICU for a week, the whole nightmare. The bill came to Rs. 8.5 lakhs. And now they are telling me it was a ‘pre-existing condition’ because I had high blood pressure!”

I looked at the rejection letter he handed me. The usual corporate language stared back: “claim denied due to non-disclosure of a pre-existing medical condition as per policy terms and conditions.”

“Arjun,” I said, setting the letter aside, “when you bought this policy three years ago, did you mention your blood pressure medication?”

“Of course I did! It is right there in my application form. They even insisted on a medical checkup, which I passed. The doctor cleared me for coverage.”

“And when you had the heart attack, who was supposed to cover your medical expenses?”

“The insurance company.”

“And who is refusing to pay now?”

His shoulders sagged. “The same insurance company that happily collected my premiums for three years, knowing full well about my blood pressure.”

This moment captures the cruel irony that thousands of policyholders face every year. The shield you bought for protection becomes the sword pointed at your chest.

Arjun’s case had all the hallmarks of wrongful denial: proper disclosure at the time of purchase, a legitimate medical emergency, and an insurance company desperately searching for technicalities to avoid a large payout.

Series recap and overview

In Part 2 of this series, we delved into the legal aspect of insurance fraud cases, covering how to navigate between civil and criminal proceedings (and when to pursue both simultaneously). We examined strategies for building evidence packages that withstand court scrutiny, ensuring digital evidence meets legal standards, and establishing practical systems for managing complex negligence litigation.

This comprehensive series addresses the following components:

Part 1: Fraud detection – Spot the red flags and behavioural patterns that reveal insurance fraud before you become a victim.

Part 2: Legal strategy – Build bulletproof cases, whether you are prosecuting fraud or defending against false allegations.

Part 3: Know your rights (This article) – Navigate every legal remedy available when insurance companies wrongfully deny your claims.

Part 4: Effective complaints – Write letters that insurance companies can actually act upon and respond to immediately.

Part 5: Ombudsman – Use this free, powerful system to force companies to pay what they owe.

Part 6: Consumer complaint – Win not just your claim but also compensation for harassment and mental agony.

Part 7: Criminal complaints – File police complaints that prosecutors will actually pursue for fraud and cheating cases.

Part 8: Constitutional protection – Approach a High Court when your fundamental rights are violated or urgent relief is needed.

This guide transforms you from feeling helpless against powerful medical institutions to holding them accountable through the law. Whether you’re a patient seeking justice or a lawyer advocating for clients, you’ll discover the exact legal pathways that can turn medical negligence from a personal tragedy into systemic accountability.

But first, understand the legal framework

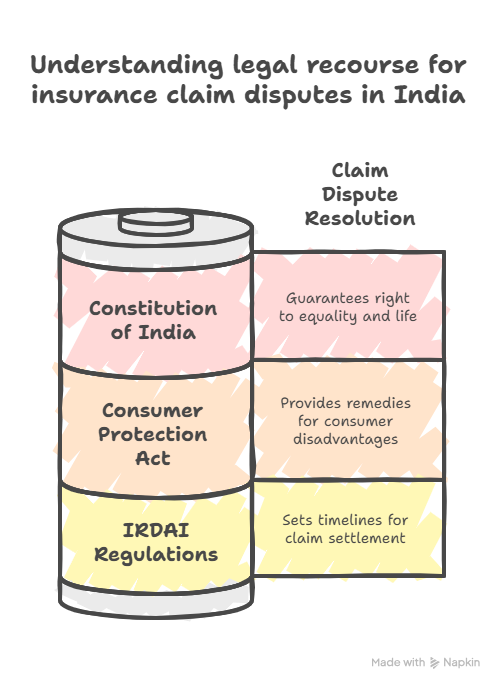

Before we dive into practical steps, it is essential to understand the legal foundation that protects your rights as a policyholder. Indian law provides multiple layers of protection, each designed to address different aspects of insurance disputes.

1. The Constitution of India, 1950

Article 14 (Right to equality): Insurance companies cannot discriminate arbitrarily between similar policyholders. If they settle comparable claims for others, they must provide valid reasons for denying yours.

Article 21 (Right to life and personal liberty): In health insurance cases, wrongful denial can directly impact your right to life. Courts have recognised that denying legitimate medical claims can violate constitutional rights.

2. The Insurance Act, 1938

Section 41 prohibits insurance agents and companies from making misleading statements to induce policy purchases. If your agent promised coverage that does not exist, this section provides both criminal and civil remedies.

Section 45 is perhaps the most important for health insurance disputes. After three years, an insurance company cannot challenge a policy based on non-disclosure or misrepresentation unless proven fraudulent. This means if you have held your health policy for over three years, pre-existing condition disputes become much harder for insurers to win.

In Arjun’s case, his policy was three years old, making the “pre-existing condition” defence legally weak under section 45.

3. IRDAI Regulations

The IRDAI (Protection of Policyholders’ Interests) Regulations 2017 provide specific timelines and procedures that insurance companies must follow. Understanding these regulations gives you concrete ammunition when dealing with delayed or denied claims.

- Health claims

- Cashless claims: 30 days from hospital discharge for final settlement

- Reimbursement claims: 30 days from receipt of complete documentation

Here is what this means in practice: Once you submit all required documents for a health insurance reimbursement claim, the company has exactly 30 days to either settle your claim or provide a written explanation for denial. They cannot simply ignore your claim or keep asking for more documents indefinitely.

I have seen health insurers try to reset this clock by claiming documents are “incomplete” or “unclear.” However, Regulation 16 specifically requires them to identify exactly which documents are missing within the first review, not discover new requirements each month.

- Motor claims

Motor insurance claims must be settled within 30 days from receipt of all documents. This is particularly important for accident claims where you might be dealing with multiple parties and complex damage assessments.

The key phrase here is “all documents.” Insurers cannot artificially extend this period by requesting documents that are not reasonably necessary for claim assessment. The surveyor’s report, repair estimates, and registration documents are standard requirements. Asking for your complete driving history from the RTO or unnecessary medical certificates for property damage claims would be unreasonable.

- Life Claims – Straightforward vs. Complex Life insurance claims are divided into two categories:

- Straightforward cases: Natural death with clear cause, policy in force – 30 days maximum

- Complex cases: Unnatural death, suicide clauses, contested nominations – longer investigation periods allowed, but with specific timelines

What makes this powerful for you is that insurance companies must classify your claim upfront. They cannot start processing it as “straightforward” and then suddenly claim it is “complex” to buy more time.

4. Consumer Protection Act 2019

This law specifically recognises that consumers face inherent disadvantages when dealing with large corporations. It provides remedies not available in regular civil courts, including compensation for mental agony, punitive damages, and litigation costs.

Common dispute patterns

Insurance disputes follow predictable patterns. Recognising these early can save you months of frustration and thousands (many times lakhs) in legal costs.

- The outright rejection

Insurers claim your loss is not covered, often citing policy exclusions that were not properly explained when you bought the policy. I have seen health insurers reject cancer claims, citing “pre-existing conditions” that the policyholder never knew existed.

- The delay game

Some companies have turned stalling into an art form. They request additional documents, then more documents, and then clarifications on those additional documents. Each request resets its internal clock while your financial pressure mounts.

Consider this: every month, the delay is money saved in their account earning interest, while you struggle to pay bills or rebuild your life.

- The partial settlement trap

You claimed Rs. 10 lakhs, and they offer Rs. 4 lakhs with complex explanations about depreciation, policy sub-limits, and “market value adjustments.” They are betting you will take what is offered rather than fight for what is rightfully yours.

- The misspelling fallout

The agent promised comprehensive coverage. When disaster strikes, you discover crucial exclusions that were never disclosed. The company blames the agent; the agent has mysteriously vanished or claims he does not remember what he told you.

How does the grievance redressal system work?

Consider Priya Sharma’s motor insurance claim. Her car was damaged in Mumbai’s devastating 2023 floods, a genuine, documented natural disaster. The surveyor confirmed flood damage worth Rs. 2.8 lakhs. Everything seemed straightforward.

The insurer’s response? “Flood damage is not covered under standard motor policy.”

This is factually incorrect. The Motor Vehicles Act and IRDAI guidelines clearly mandate flood coverage in comprehensive policies. But the insurer was counting on Priya not knowing this technical detail.

She did not give up. Following the exact steps we will discuss, she not only got her claim settled but also received compensation for the delay. The insurer eventually paid Rs. 3.2 lakhs total, original claim plus interest and costs.

Why did they change their position? Because Priya understood which buttons to push and which authorities to approach. More importantly, she realised that insurance companies fear regulatory action more than individual complaints.

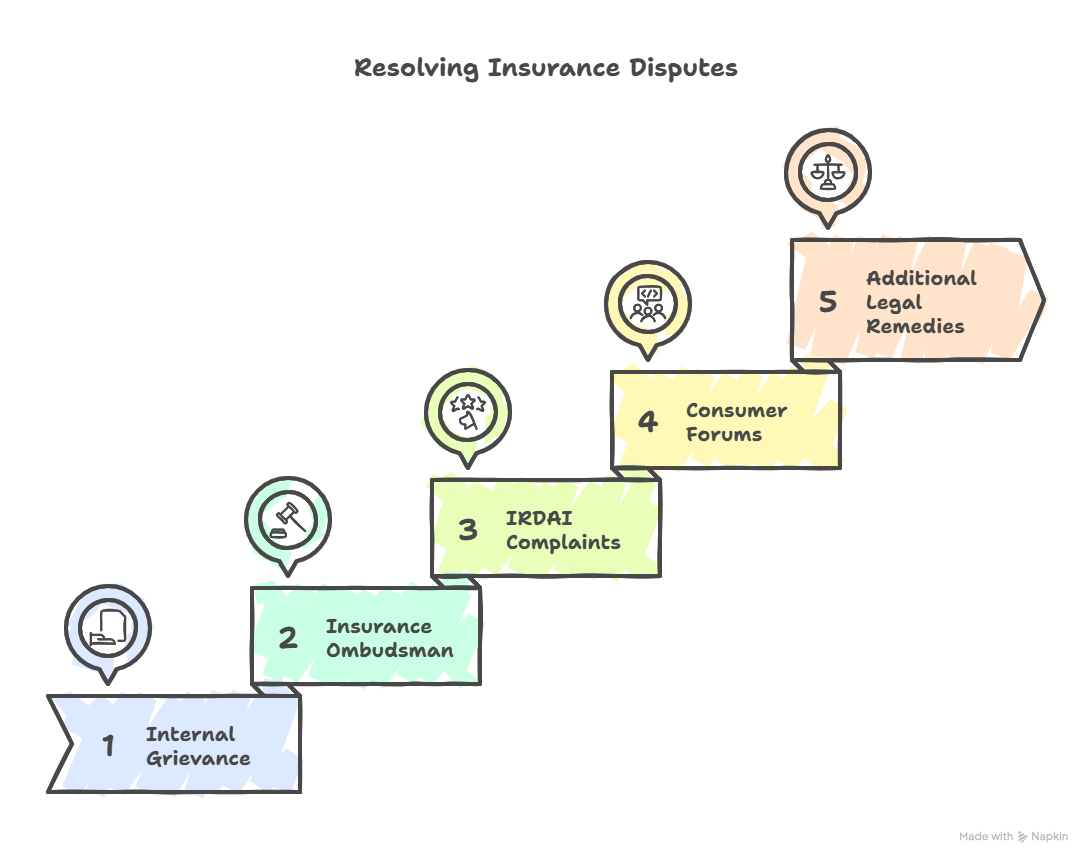

Step 1: Internal grievance

Before approaching any external authority, you must give your insurance company a chance to correct its mistake. This is not just courtesy, it is a legal requirement that can undermine your case if ignored.

Think of this step as giving them enough rope to hang themselves. Every response (or lack thereof) becomes evidence in your eventual case.

i. Finding the right person

Every insurance company must have a Grievance Redressal Officer (GRO). This person’s job is to resolve complaints that regular claims departments cannot or will not handle. In practice, GROs are often more reasonable than front-line claims staff because they understand the legal implications of wrongful denials.

ii. Language that commands attention

When writing to the GRO, certain phrases carry legal weight that separates your complaint from routine customer service issues:

“This complaint is being filed under section 42 of the Insurance Act, 1938, and IRDAI (Protection of Policyholders’ Interests) Regulations, 2017.”

This immediately signals that you understand the legal framework. Insurance companies take such complaints more seriously because they know you are not just venting, you are building a case that could land on a regulator’s desk.

iii. Essential elements of your complaint

Start with your policy number and claim number in the very first line. Insurance companies process thousands of claims daily. Making it easy for them to locate your file shows you mean business.

Include a clear, chronological timeline of events. Confusion works in their favour, so a clear timeline forces them to address each step of their handling.

Specifically mention policy clauses you believe support your claim. Do not just say, “This should be covered.” Say, “This loss is covered under section 4.2 of my policy, which specifically includes natural disasters.”

State the exact relief you are seeking. Do not just say, “settle my claim.” Say “I seek settlement of Rs. 15 lakhs as per the surveyor report dated [date] within 15 days as required under IRDAI settlement guidelines.”

iv. The 15-day rule that changes everything

Once you file a complaint with the GRO, the insurance company has exactly 15 days to respond. Not 15 working days, 15 calendar days. This is not a suggestion; it is a regulatory requirement with real consequences.

Mark your calendar for day 16. On that day, if you have not received a satisfactory response, you are legally cleared to escalate to the next level. This 15-day rule puts time pressure on them, not you.

Step 2: The insurance ombudsman

Here is what insurance companies desperately hope you do not discover: Ombudsman decisions are not just recommendations; they are binding on the insurance company. When an Ombudsman rules in your favour, the company must comply within 30 days or face serious regulatory consequences.

Think of the Ombudsman as a free arbitrator with real enforcement power. You get quasi-judicial resolution without the cost, complexity, or time delays of formal court proceedings.

Eligibility requirements

- Individual policyholders (not companies) with claims under Rs. 50 lakhs

- You must have first complained to the insurance company and either received an unsatisfactory response or waited 30 days without any response

- The complaint must be filed within one year of receiving the insurer’s final rejection

i. The BIMA Bharosa advantage

The government’s BIMA Bharosa portal has revolutionised ombudsman access. What used to require physical visits to distant offices can now be done entirely online.

However, do not rely solely on the online system. Create your complaint online, but also send physical copies to the relevant ombudsman office. This dual approach ensures your complaint is registered even if technical issues affect the online system.

ii. Making your case Ombudsman-ready

The ombudsman receives hundreds of complaints monthly. The ones that get resolved quickly are those that make the officer’s job easy by presenting information clearly and logically.

Structure your complaint like a legal brief:

Summary: One paragraph explaining what happened and what you want.

Chronology of events: Date-wise timeline from policy purchase to current date.

Legal grounds: Specific policy clauses, IRDAI regulations, or legal provisions supporting your case.

Relief sought: Exact amount and any additional compensation for delays or harassment.

Documentary evidence: Number and describe each document you are attaching.

Step 3: IRDAI complaints

The Insurance Regulatory and Development Authority of India (IRDAI) is not primarily a complaint resolution body like the ombudsman; it is a regulator with the power to fine, censure, and even cancel insurance licenses.

Think of IRDAI as the insurance industry’s strict supervisor. When you complain to them, you are not just seeking individual relief; you are potentially triggering broader regulatory action that can change how the entire company operates.

i. When to approach IRDAI

- When your complaint involves systematic regulatory violations

- When you are facing issues that affect multiple policyholders and suggest broader misconduct

- When insurance companies are blatantly violating IRDAI guidelines on timelines, procedures, or disclosure requirements

ii. The IGMS system

IRDAI’s Integrated Grievance Management System (IGMS) at www.irdai.gov.in provides direct access to the regulator’s supervisory team.

Unlike ombudsman complaints, which focus on individual dispute resolution, IGMS complaints focus on regulatory compliance and market conduct. This creates pressure from a different direction and shows the insurer you are serious about pursuing all available remedies.

Step 4: Consumer forums

Consumer forums operate under the Consumer Protection Act 2019, which specifically recognises that consumers are inherently disadvantaged in disputes with large corporations.

i. Why consumer forums work better than regular courts

Simplified procedures: You do not always need extensive legal knowledge, though having a lawyer certainly helps.

Cost-effective: Filing fees are minimal compared to civil courts.

Consumer-friendly presumptions: The law assumes good faith on the consumer’s part and places the burden on companies to justify their actions.

Compensatory relief: Forums can award compensation for mental agony, harassment, and litigation costs beyond just the claim amount.

Faster resolution: Consumer forums have mandated timelines that are generally respected.

ii. Jurisdiction based on claim value

- District Consumer Forum: Claims up to Rs. 1 crore

- State Consumer Commission: Claims between Rs. 1 crore and Rs. 10 crores

- National Consumer Disputes Redressal Commission: Claims above Rs. 10 crores

iii. The two-year filing deadline

Consumer complaints must be filed within two years of the “cause of action”, usually when you first knew or should have known about the unfair practice.

iv. Drafting a winning consumer complaint

You need to establish two main things: a deficiency in service and unfair trade practices.

Unfair trade practice: Clearly articulate how the insurance company’s actions constitute unfair trade practice under the Consumer Protection Act.

Service deficiency: Explain how the insurer’s service fell below reasonable standards expected from a professional insurance company.

Quantified damages: Claim not just the policy amount, but also:

- Original claim amount with interest

- Compensation for mental agony and harassment

- Litigation costs and lawyer fees

- Any additional financial losses caused by the delay

Step 5: Additional legal remedies

i. Alternate Dispute Resolution

- Check your policy first: Many insurance policies, especially high-value commercial ones, contain mandatory arbitration clauses that override your right to approach consumer forums. If your policy mandates arbitration, attempting to file complaints elsewhere will result in rejection. Always review your policy’s dispute resolution clause before choosing your legal strategy.

- Mediation as a strategic option: When arbitration is optional, consider mediation for ongoing policy relationships or complex disputes requiring creative solutions. This mode of dispute resolution is ideal when you want to preserve your relationship with the insurer while securing fair compensation.

ii. Civil courts

Approach civil courts only when:

- Your claim exceeds consumer forum jurisdiction (above Rs. 10 crores)

- Complex legal issues require detailed judicial examination

- You are seeking specific performance rather than just monetary compensation

iii. Criminal complaints

When insurance agents or companies knowingly misrepresent policy terms to induce purchases, criminal charges under section 318 of the Bharatiya Nyaya Sanhita become viable.

Key elements you must prove:

- Deliberate misrepresentation of material facts

- Clear intention to deceive you

- Financial loss resulting directly from that deception

Documents that you must have in place

The fundamental rule: If it is not documented, it did not happen in the eyes of the law.

1. Primary documents (Non-negotiable)

- Original insurance policy with all endorsements

- Premium payment receipts for the entire policy period

- Claim form with acknowledgement receipt

- All correspondence with the insurer

2. Secondary evidence

- Surveyor reports and damage assessments

- Independent expert opinions

- Witness statements

- Photographs or video evidence with timestamps

- Police or government agency reports

- The communication trail

Save every email, WhatsApp message, and written communication. Screenshot WhatsApp conversations immediately and save them as PDFs with timestamps visible.

Always respond in writing. Even after positive phone conversations, follow up with an email confirming what was discussed and agreed upon.

Tried and tested success strategies

- The mindset that wins

Think like a prosecutor building a case, not a victim seeking sympathy. Your goal is to build an unassailable legal case based on facts, law, and evidence.

Insurance companies respect strength and preparation. They settle cases they might lose and fight cases they think they can win through superior resources or claimant fatigue.

- Common pitfalls that destroy strong cases

The incomplete claim Trap: Do not submit your claim until you have all required documents. Incomplete claims give insurers legitimate grounds for delay or rejection.

The settlement pressure mistake: Insurers often offer quick, low settlements, hoping you will take the money and disappear. Before accepting any settlement, calculate whether it is actually fair.

The documentation gap: Missing even one crucial document can derail your entire case, especially in consumer forums where the burden is on you to prove deficiency in service.

- When to engage professional help

Hire a lawyer when:

- Your claim is on the higher side

- The insurer alleges fraud or policy violations against you

- Multiple complex legal issues are involved

- You are facing criminal allegations

Choose lawyers with specific insurance law experience. A lawyer who has handled 50 insurance disputes is worth more than one who has handled 500 general civil cases.

Final thoughts

The insurance industry’s intimidation tactics only work when you allow them to. Every bureaucratic hurdle, every unnecessary delay, and every attempt to confuse you with complex jargon is simply a test of your resolve. The legal framework: ombudsman systems, consumer forums, and regulatory authorities, exists precisely to neutralise these corporate advantages and restore balance to what should be a fair transaction.

Your success depends on three pillars: acting swiftly within prescribed time limits, maintaining meticulous documentation of every interaction, and choosing the right legal avenue for your specific situation. Whether it is the ombudsman route for efficiency, consumer forums for comprehensive relief, or direct regulatory complaints for systemic issues, each path offers distinct advantages when used strategically.

Every successful challenge against wrongful claim denial creates a ripple effect throughout the industry. When you stand up for your rights, you are not just securing your own settlement; you are making it harder for insurance companies to exploit the next genuine claimant.

In the next part of this series, we will, I will show you exactly how to approach your insurance company strategically and draft compelling complaints using AI tools that level the playing field from day one.

FAQs

- Can I claim compensation for mental agony even if my insurance claim is eventually settled?

Absolutely. Consumer forums often award Rs. 50,000 to Rs. 2 lakhs for mental agony caused by wrongful denial or unreasonable delays, even when the original claim is later settled. The key is proving that the insurer’s conduct caused you genuine distress through medical records, therapy receipts, or impact statements. Insurance companies often try to settle just the claim amount, hoping you forget about the harassment compensation.

- What happens if my insurance agent has disappeared or denies giving me the wrong information about my policy?

Under IRDAI regulations, insurance companies are legally responsible for their agents’ actions and promises. Document everything: WhatsApp messages, emails, conversations with dates and witnesses. You can file separate complaints against both the agent and the company simultaneously, which often creates more pressure for a settlement. The company cannot simply blame the agent and walk away.

- Can I approach multiple forums simultaneously, or do I have to choose just one?

You can strategically use multiple forums, but timing matters. File IRDAI complaints for regulatory violations while your ombudsman case is pending since they serve different purposes. However, you cannot file identical relief claims in consumer forums and civil courts simultaneously. Criminal complaints for fraud can run parallel to civil remedies.

- If my policy is more than three years old, can the insurance company still deny my health claim for pre-existing conditions?

After three years, section 45 of the Insurance Act 1938 prohibits insurance companies from challenging your policy or denying claims based on non-disclosure unless they prove deliberate fraud. If you disclosed your blood pressure and they are calling your heart attack “pre-existing,” they are on weak legal ground. Many insurers try wrongful denials, hoping policyholders do not know the three-year rule.

- What is the difference between approaching a consumer forum versus the insurance ombudsman?

The ombudsman is faster and free but limited to Rs. 50 lakh claims and focuses on proper procedures. Consumer forums take longer but can award compensation for mental agony and punitive damages beyond your claim amount. If your case is straightforward under Rs. 50 lakhs, start with the ombudsman. If you have suffered harassment, consumer forums make insurers pay for their misconduct.

Allow notifications

Allow notifications