You have spotted the fraud. Now what? This article walks you through taking those suspicions and turning them into solid court cases. Whether you are an insurance lawyer or work in-house for an insurance company, these strategies will help you win fraud cases that actually stick.

Introduction

Picture this: A warehouse burns down exactly 18 months after the owner increased his fire coverage by 400%. He files a Rs. 2.5 crore claim.

You are not going to believe this. That same inventory he claims got destroyed? He sold it to buyers in Chennai for six months.”

I am sitting there looking at photos, receipts, bank statements, everything spread across my conference table like pieces of a puzzle. This was the Bharti General Insurance case that would test everything I thought I knew about fraud litigation.

You know that moment when you realise catching the fraudster was the easy part? That is where I was.

Most lawyers I know get this backwards. They think if the evidence is strong enough, the case will handle itself. Wrong. I have seen sure-shot fraud cases fall apart because nobody thought through the litigation angle.

Here is what nobody tells you about insurance fraud cases: they are messy. Unlike other civil matters where you are arguing contract terms or liability percentages, fraud cases live in this grey area between civil and criminal law.

Do you file a civil suit to recover the claim amount? Go criminal and push for prosecution? Both? The choice you make here determines everything: your evidence requirements, your timeline, even your chances of actually getting paid back.

I learned this the hard way in my second year of practice.

Series recap and overview

In our previous part, that is Part 1 of this series, we explored the critical first line of defense against insurance fraud: detection. We examined how fraudsters follow predictable patterns across health, life, motor, and commercial insurance, revealing behavioural red flags. Through cases like the Rs. 25 lakh textile fire fraud, we saw how lawyers must combine traditional investigation techniques with modern technology, building professional networks and implementing systematic due diligence frameworks to catch fraud before it succeeds.

What will it cover?

Part 1: Fraud detection – Spot the red flags and behavioural patterns that reveal insurance fraud before you become a victim.

Part 2 (This article): Legal strategy – Build bulletproof cases, whether you are prosecuting fraud or defending against false allegations.

Part 3: Know your rights – Navigate every legal remedy available when insurance companies wrongfully deny your claims.

Part 4: Effective complaints – Write letters that insurance companies can actually act upon and respond to immediately.

Part 5: Ombudsman – Use this free, powerful system to force companies to pay what they owe.

Part 6: Consumer complaint – Win not just your claim but also compensation for harassment and mental agony.

Part 7: Criminal complaints – File police complaints that prosecutors will actually pursue for fraud and cheating cases.

Part 8: Constitutional protection – Approach a High Court when your fundamental rights are violated or urgent relief is needed.

This article breaks down the practical stuff:

- How to choose between civil and criminal proceedings (and when to do both)

- Building evidence packages that actually hold up in court

- Making sure digital evidence does not get thrown out on technicalities

- Practical systems for managing complex fraud litigation

This is not a theory. These are methods I have used in actual cases, including some spectacular failures that taught me what not to do.

Case study

Vishal Textiles operated a 50,000 sq. ft. warehouse in Tirupur, storing cotton fabric worth approximately Rs. 2.5 crores. The owner, Mr. Suresh Vishal, had been struggling with declining orders and mounting debts. Eighteen months before the fire, he increased his insurance coverage from Rs. 60 lakhs to Rs. 2.5 crores, a 400% jump that should have triggered immediate scrutiny.

It did not.

The fire occurred on a Sunday night in December 2023. By Monday morning, Vishal had filed a comprehensive claim with detailed inventory lists, fire department reports, and witness statements. Everything looked legitimate until our forensic accountant made a discovery that changed everything.

The discovery that broke the case

While reviewing Vishal’s GST returns for the six months preceding the fire, we found sales invoices for cotton fabric worth Rs. 1.8 crores, supposedly destroyed inventory that had been sold and delivered to buyers in Chennai, Coimbatore, and Madurai.

The warehouse had burned down, but it was nearly empty when it happened.

This discovery forced me to make the first critical strategic decision: civil recovery or criminal prosecution?

Insurance fraud litigation: Civil vs criminal proceedings strategy guide

“We can prove he sold the inventory before the fire,” Bharti Insurance’s claims head told me. “Is that not enough to deny the claim and move on?”

It was not that simple. Vishal’s case involved multiple layers of fraud that required different legal approaches:

The fraud pyramid:

- Base layer: False inventory claims (Rs. 1.8 crore phantom stock)

- Middle layer: Forged purchase invoices (creating a paper trail for non-existent inventory)

- Top layer: Possible arson (fire timing and circumstances were suspicious)

Each layer required different evidence standards and legal strategies.

The civil track

Primary objective: Deny the fraudulent claim and recover costs (investigation, legal, etc.).

Legal foundation: Section 45 (material misrepresentation) of the Insurance Act 1938 and breach of policy conditions.

Evidence strategy:

- GST returns showing inventory sales before the fire

- Buyer confirmations of actual deliveries

- Transportation records proving inventory movement

- Bank records showing payment receipts

The civil approach offered certainty, but it would not address the broader fraud or deter future attempts.

The criminal track

Primary objective: Criminal conviction to deter organised fraud networks.

Legal foundation: Multiple BNS provisions depending on evidence development.

Investigation strategy:

- Section 318 BNS (Cheating): Three-element proof structure

- Section 336 BNS (Forgery): Focus on fabricated purchase invoices

- Section 326 BNS (Mischief by fire): If arson could be proved

Why should we run civil and criminal cases simultaneously?

I recommended running both tracks simultaneously for maximum leverage. Here is why:

Immediate benefits:

- Civil denial protects against fraudulent payout

- Criminal charges created settlement pressure

- Evidence gathering served both cases

- Media attention deterred copycat frauds

Long-term impact:

- A criminal conviction would prevent future fraud attempts

- Industry precedent for handling sophisticated schemes

- Recovery of investigation costs and punitive damages

How to build evidence?

When we first suspected Vishal’s fire claim was fraudulent, we had gut instinct and red flags, but gut instinct does not win court cases. We needed systematic evidence collection that could withstand aggressive cross-examination and meet both civil and criminal standards. Here is how we built an unshakeable foundation, phase by phase.

Phase 1: Follow the money trail

Why financial forensics comes first: Money leaves the clearest trail, and financial evidence is hardest to explain away in court.

Our forensic accountant, Priya Sharma, instead of examining Vishal’s claim, investigated what actually happened to his inventory over the six months preceding the fire.

What the numbers revealed:

- Purchase records: Vishal had invoices showing he bought Rs. 2.5 crores worth of cotton fabric

- Sales reality: His GST returns showed he had already sold Rs. 1.8 crores of that same fabric before the fire

- Payment proof: Bank statements confirmed he had received payments for the supposedly “destroyed” inventory

- Delivery evidence: Transportation records showed the fabric was actually delivered to buyers in Chennai months before the warehouse burned

Vishal was claiming insurance for fabric that customers had already received and paid for. When the fire happened, the warehouse contained maybe Rs. 70 lakhs worth of actual inventory, not the Rs. 2.5 crores he claimed.

Phase 2: Digital footprints do not lie

The modern advantage: Fraudsters think they are clever, but they leave digital footprints everywhere. Our cyber forensics expert, Arjun Malhotra, followed those footprints to build a timeline of premeditated fraud.

Digital evidence that sealed the case:

- Email chains: Detailed discussions about “liquidating inventory quickly” and “maximising recovery from insurance”

- WhatsApp coordination: Messages between Vishal and buyers arranging fabric pickup schedules

- Banking records: Digital payments flowing through multiple accounts to disguise the sales volume

- Cloud storage goldmine: Photos Vishal had taken of his warehouse, showing it was nearly empty weeks before the fire

Phase 3: Physical evidence tells the real story

The fire investigation challenge: Proving arson is notoriously difficult because fire destroys evidence. But fire investigation expert Rakesh Khanna found patterns that did not match Vishal’s accidental fire story.

Red flags:

- Multiple ignition points: The fire started in several places simultaneously, suggesting that an accelerant was used

- Burn patterns: The way the fire spread was inconsistent with accidental causes

- Missing smoke signatures: A warehouse full of cotton fabric should have produced specific smoke patterns, but these were absent

- Convenient timing: Sunday night fire with no security present and minimal inventory to actually burn

The limitation we faced: While the physical evidence strongly suggested arson, we could not directly link Vishal to setting the fire. This is where circumstantial evidence becomes crucial and why the financial and digital evidence was so important.

Phase 4: Witness testimony

The witness development dilemma: The people who knew the most about Vishal’s scheme were either his accomplices or his business partners. Getting them to testify required strategic thinking, not just investigative skills.

What they confirmed:

- They had received fabric deliveries 2-4 months before the fire

- They provided transportation and payment records proving the sales

- They verified the quality and quantities of fabric they had received

Insider’s testimony: Kumar, the warehouse manager, knew exactly what inventory was really in the warehouse, but he was also terrified of criminal charges and potential retaliation.

But how did we flip it?

- Legal protection: We offered immunity from criminal prosecution if he testified truthfully

- Physical protection: We arranged relocation assistance due to legitimate security concerns

- Clear incentives: We made cooperation more attractive than silence

His crucial testimony:

- Confirmed the systematic removal of inventory over six months

- Identified which purchase invoices were forged

- Revealed conversations about increasing fire insurance coverage

Expert testimony: Individual experts are valuable, but a coordinated expert team creates an overwhelming narrative that is difficult for the defence to challenge.

- Forensic accountant: Established the financial fraud foundation through GST analysis and inventory reconstruction

- Digital forensics specialist: Proved premeditation through electronic communications and payment tracking

- Fire investigation expert: Demonstrated the suspicious nature of the fire itself

- Insurance industry expert: Explained standard practices and the broader impact of this type of fraud

Why sequencing matters: Each expert’s testimony is built on the previous expert’s findings:

- Financial foundation: The accountant showed inventory was missing

- Intent proof: The digital expert proved this was planned, not accidental

- Method evidence: The fire expert suggested how the final act was carried out

- Impact context: The industry expert explained why this matters beyond just one case

By the time we finished presenting expert testimony, the court had heard the same basic story from four different professional perspectives, each using their specialised expertise to confirm what the others had found. This coordination made our case nearly impossible to refute.

Complete legal framework

Before we begin, please note that the following legal framework is based on and incorporates facts and scenarios derived from the aforementioned Vishal Textiles case study.

A. Criminal charges

- Section 318 BNS (Cheating)

| Element 1: Deception | Element 2: Inducement | Element 3: Wrongful loss | The evidence package: |

| False inventory claims (Rs. 1.8 crore phantom stock)Forged purchase invoices create a paper trailMisleading fire damage assessments | Bharti Insurance processed a claim based on false inventory listsRelied on forged purchase invoices as proof of stockTrusted fire damage claims without independent verification | Rs. 2.5 crore fraudulent claim amountRs. 15 lakh investigation costsReputational damage to the insurance industry | GST returns vs. insurance claim comparisonBuyer confirmations of actual deliveriesBank records showing payment receiptsExpert testimony on fraud methodology |

- Section 336 BNS (Forgery) – Document fraud

| The forged documents | Proof requirements | Forensic evidence |

| Purchase invoices for non-existent inventoryBackdated supplier agreementsFabricated storage receipts | Document creation with the intent to defraudKnowledge of false natureActual use in insurance claims | Paper analysis showing recent creation datesInk analysis reveals contemporaneous creationDigital forensics shows file creation timestamps |

B. Provisions of the Insurance Act 1938 that protect your client’s interests

- Section 45: Material misrepresentation

Vishal’s violations:

- Failed to disclose inventory sales before the fire

- Provided false inventory valuations

- Concealed actual warehouse contents

Legal consequences:

- Void insurance policy ab initio

- Eliminates coverage for the loss

- Supports claim denial

2. Section 42: Agent liability

The Agent’s role:

- Processed a 400% coverage increase without proper verification

- Failed to report suspicious circumstances

- Negligent in risk assessment

Legal implications:

- Agent liability for facilitating fraud

- License suspension proceedings

- Professional negligence claims

C. IRDAI (Insurance Fraud Monitoring Framework) Guidelines, 2013

- Investigation thresholds

Claims above Rs. 1 lakh trigger mandatory formal investigations, while Rs. 2.5 crore claims require comprehensive reviews with expert involvement. Complex cases automatically bring in specialised investigators and forensic experts to analyse fraud patterns.

- Compliance documentation

Insurers must maintain detailed investigation timelines, formally document expert appointments, and follow strict evidence preservation protocols. All records must be properly secured for potential legal proceedings.

- FIU-IND reporting

Suspicious transactions must be reported within 7 days with detailed fraud pattern documentation. Inter-agency coordination ensures information sharing between insurers, investigators, and regulatory bodies.

- IRDAI notification

Fraud detection reports are due within 30 days, followed by regular progress updates throughout investigations. Final outcome reporting documents actions taken, recoveries made, and prevention measures implemented.

The three-phase trial strategy to navigate complex fraud cases

Act 1: Establishing the fraud foundation

Opening strategy: Present the fraud timeline chronologically, making it easy for the judge to follow.

Key testimony sequence:

- A forensic accountant explains inventory discrepancies

- Buyers confirm actual deliveries before the fire

- Digital expert presents electronic evidence

- Fire investigator discusses suspicious circumstances

Act 2: Defence

Vishal’s defence strategy:

- The claimed inventory was replacement stock

- Argued the fire was accidental

- Disputed GST return accuracy

Our counter-attack:

- Warehouse manager’s testimony about systematic inventory removal

- Transportation records proving no replacement deliveries

- Expert testimony on fire origin and cause

Act 3: Conviction

Final evidence presentation:

- Industry expert on fraud impact

- Character witnesses on Vishal’s financial desperation

- Summary of evidence chronology

Closing argument strategy:

- Emphasise the systematic nature of the fraud

- Highlight the impact on honest policyholders

- Request exemplary punishment for a deterrent effect

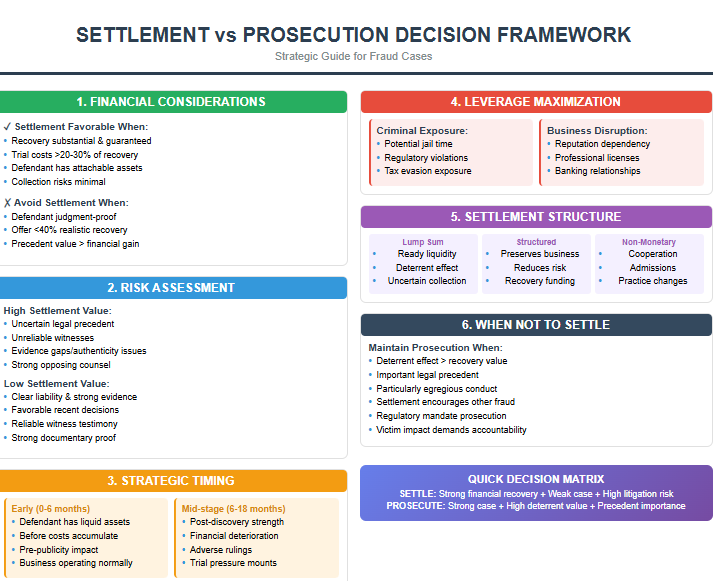

Settlement vs prosecution: a strategic decision-making guide

“We can take Rs. 40 lakhs today, or gamble on Rs. 2.5 crores in court.” Bharti Insurance’s CEO was weighing Vishal’s settlement offer, but I knew this decision would impact far more than one case.

In the Vishal Textiles fraud, our settlement choice did not just recover money; it sent a message across the industry about how fraudsters calculate their risks.

Here is the strategic framework that guided that decision:

Evidence standards and authentication guide

Understanding the burden of proof: civil vs criminal cases

In civil cases, you only need to prove that something is more likely than not to have happened. This means if there is a 51% chance your version of events is correct, you win the case.

What this means in practice:

- You do not need perfect evidence, just enough to tip the scales in your favour

- Multiple pieces of circumstantial evidence can build a strong case

- Expert opinions and inferences from facts are often sufficient

Our case example: The GST returns alone suggested fraud was likely. When we added buyer confirmations and expert testimony, we had enough evidence to convince the court. The claim denial was upheld within just 8 months because we met the civil standard.

Criminal cases: beyond a reasonable doubt standard

Criminal cases require much stronger evidence. The prosecution must prove guilt to such a degree that a reasonable person would not hesitate to rely on it in making important decisions. Now, what kind of evidence are we talking about here?

- Every single element of the crime must be proven with near certainty

- If there is any reasonable doubt about any part of the case, the defendant should be acquitted

- Circumstantial evidence needs strong corroboration from other sources

- Any weakness in the chain of evidence can destroy the entire case

The challenges we faced: We had no direct witness who saw the arson happen. Some of our digital evidence was not properly authenticated according to strict criminal standards. We also had to prove intent, which is difficult when you are relying on inferences from behaviour rather than direct evidence.

The outcome: We successfully proved cheating and forgery because we had solid documentation. However, the arson charges were dropped because we could not meet the higher criminal standard for those specific allegations.

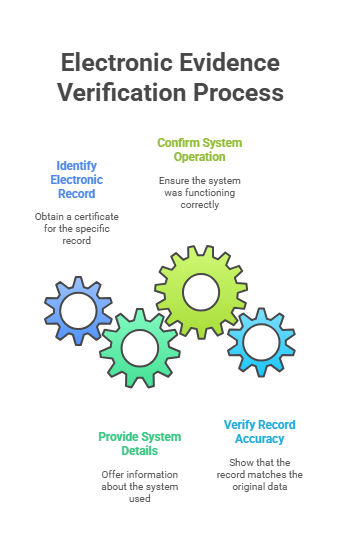

Digital evidence

Understanding the legal requirements

Section 63 of the Bharatiya Sakshya Adhiniyam sets out specific requirements for digital evidence to be admissible in court. Here is a checklist you must complete:

Step-by-step compliance strategy

We developed a systematic approach to ensure that all our digital evidence would be accepted:

Because we followed these procedures carefully, all our digital evidence was admitted without any objection from the defence. The court had confidence in the integrity of our evidence.

Defending against countersuits

Here is something that catches many insurance companies off guard: the moment you start investigating a suspicious claim, the fraudster often flips the script. Instead of defending their fraudulent claim, they go on the offensive and sue you. And it works more often than you would think.

Vishal was no different. When we started closing in on his insurance fraud scheme, he did not just quietly accept defeat. Instead, he hired lawyers and came at us from three different angles, each designed to put us on the back foot and make us think twice about pursuing fraud cases in the future.

The three-pronged counterattack

Attack #1: “You denied my claim in bad faith”

This is the fraudster’s favourite weapon. Vishal claimed we were just looking for excuses to avoid paying legitimate claims. His argument? We took too long to investigate, we asked for too much documentation, and we were essentially acting in bad faith by denying what he insisted was a perfectly valid claim.

The beauty of this attack, from the fraudster’s perspective, is that it puts you in a difficult position. Suddenly, you are not investigating fraud; you are defending your own business practices. The focus shifts from “Did this person commit fraud?” to “Did the insurance company follow proper procedures?”

Attack #2: “You defamed me by calling me a fraudster”

This one stings because there is always a grain of truth to it. During fraud investigations, information gets shared with lawyers, experts, and sometimes law enforcement. Vishal claimed that our “reckless accusations” of fraud had damaged his reputation in the business community.

The defamation claim serves multiple purposes. It makes you think twice about sharing information during investigations, it potentially exposes your investigators to personal liability, and it creates a chilling effect where your team becomes afraid to call fraud what it is.

Attack #3: “Your investigators harassed and intimidated me”

This is where things get personal. Vishal complained that our investigators were too aggressive, that they showed up at his business unannounced, that they asked “intimidating questions,” and that the whole process felt like harassment.

This attack is particularly effective because fraud investigations do involve confrontational moments. When you are trying to get to the truth, conversations can become uncomfortable. But there is a fine line between a thorough investigation and harassment, and fraudsters love to claim you have crossed it.

Why these tactics work (And why you should expect them)

These countersuit strategies are popular because they often succeed in achieving the fraudster’s real goal: making you go away. Here is the psychological warfare at play:

- They make fraud investigation expensive and risky. Suddenly, you are not just spending money to investigate a claim, you are spending money to defend your own actions. Legal costs multiply quickly.

- They create internal pressure to settle. Your own management starts asking whether it is worth the fight. “Maybe we should just pay the claim and avoid the lawsuit,” becomes a tempting option.

- They establish a pattern of intimidation. Other potential fraudsters hear about these tactics and think twice before filing suspicious claims, knowing you will fight back hard.

How to build your defence against such attacks

The key to handling these attacks is not just responding when they happen, it is building your defence into your investigation process from day one. Here is what actually works:

- Document everything with legal justification

Do not just document what you did; document why you did it. Every investigation decision should have a clear legal or business justification that you can explain to a judge later.

When we requested additional documentation from Vishal, we did not just say, “We need more information.” We documented exactly why each piece of information was necessary to evaluate the claim, and we tied it back to specific policy language and regulatory requirements.

When we brought in experts, we documented why expert analysis was necessary and how it related to determining coverage. This was not just good investigative practice; it was building our defence against future bad faith claims.

- Maintain professional standards (even when it is frustrating)

Fraud investigations are inherently confrontational, but how you conduct yourself matters enormously. Every email, every phone call, and every interaction with the claimant or their representatives should meet professional standards.

We trained our investigators to remain calm and professional even when dealing with obviously fraudulent claims. We avoided accusatory language in written communications. We followed up aggressive questioning with clear explanations of why we needed the information.

This is not just about being nice; it is about building a record that shows you conducted a thorough, professional investigation rather than a personal vendetta.

- Follow regulatory guidelines like your business depends on it

Because it does. IRDAI guidelines are not suggestions; they are your roadmap to avoiding regulatory trouble and your best defence against bad faith claims.

We created checklists to ensure every investigation followed IRDAI guidelines. We documented compliance at each step. When Vishal claimed we acted in bad faith, we could point to a comprehensive record showing we followed industry best practices throughout the process.

- Get litigation insurance (before you need it)

This is the protection most insurance companies overlook until it is too late. Litigation insurance covers the costs of defending against countersuits and can even cover damage awards if you lose.

We secured coverage that specifically included defence costs for fraud-related countersuits. When Vishal sued us, we were not making decisions based on legal costs; we could focus on the merits of the case because we knew our defence was covered.

Final thoughts

The Vishal Textiles case proved that successful fraud prosecution requires more than just catching fraudsters; it demands strategic legal thinking from day one. By running parallel civil and criminal tracks, building bulletproof evidence chains, and preparing for inevitable countersuits, we not only recovered the fraudulent claim but also sent a clear deterrent message across the industry. The key lesson? Fraud investigation is as much about building your legal defence as it is about building your case against the fraudster.

Building strong legal strategies for insurance fraud cases requires understanding that every investigation decision has litigation consequences. From choosing the right evidence authentication procedures to maintaining professional standards under pressure, success comes from treating each fraud case as both an investigation and a potential courtroom battle. When you build your defence while building your case, you transform from an easy target into a formidable opponent that fraudsters learn to avoid.

In Part 3 of this series, we will explore the other side of the equation, that is, when insurance companies get it wrong, how legitimate claimants can challenge it. We will examine the regulatory complaint process, ombudsman procedures, and legal remedies available when insurance companies cross the line from thorough investigation into bad faith claim handling.

Frequently asked questions

- Can insurance companies reject my claim just because I filed it late?

Not necessarily. While insurers set claim-filing deadlines, courts often excuse reasonable delays if you can show valid reasons. The key is acting promptly once you discover the loss and having good documentation for any delay.

- What happens if I win my case but the insurance company still does not pay?

Ombudsman decisions and consumer forum orders are legally binding. If insurers do not comply within 30 days, you can file contempt proceedings or execution petitions that can freeze their bank accounts and assets until they pay.

- Do I need a lawyer to fight my insurance company, or can I represent myself?

For claims under Rs. 10 lakhs, you can often handle ombudsman and consumer forum proceedings yourself; they are designed to be accessible. For larger claims or when facing fraud allegations, experienced legal representation becomes essential for navigating complex procedures and evidence requirements.

- How long do these disputes typically take from start to finish?

Ombudsman cases usually resolve in 3-6 months, consumer forums take 6-18 months, while civil court cases can stretch 2-5 years. The key is choosing the right forum initially rather than appealing through multiple levels, which can double your timeline.

- Can the insurance company claim I committed fraud just to avoid paying my legitimate claim?

Yes, this is a common intimidation tactic called “fraudulent repudiation.” However, insurance companies must prove fraud with solid evidence; they cannot just make accusations. If they falsely allege fraud, you can claim additional compensation for defamation and mental agony in consumer forums.

Allow notifications

Allow notifications