Explore how the Companies Act, 2013 governs board reports under section 134 and learn practical, AI-driven methods to draft accurate disclosures. This guide explains auditor responses, section 186 investments, and related party transactions while ensuring compliance with the Companies Act, 2013. With step-by-step strategies it shows how to balance transparency, regulatory accuracy, and business sensitivity in board reports. Perfect for professionals seeking clarity on section 134 compliance and smart use of AI in corporate reporting.

About this series

This is Part 5 of our 8-part series on using AI to draft board reports under the Companies Act 2013.

Complete Series Overview:

- Part 1: Getting Started

- Part 2: Building the foundation (Groups 1-2)

- Part 3: Financial performance and capital management (Group 2)

- Part 4: Getting directors’ statements right (Group 3)

- Part 5: External stakeholders and audit relations (Group 4) ← You are here

- Part 6: Risk management and CSR disclosures (Group 5)

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – complete board report

Haven’t started from Part 1? No problem! This article works standalone, but you will get more value by reading the series sequentially.

What you will learn in this article: External scrutiny changes everything. Watch as Arjun and Ms. Rao craft responses to auditor qualifications and related party disclosures that satisfy regulators without revealing competitive business information.

Key Characters:

- Arjun Sharma: Junior lawyer mastering AI collaboration techniques

- Ms. Priya Rao: Senior partner, now actively contributing strategic insights

- Nova AgriTech: Their client-facing auditor qualification issues require a diplomatic response

Quick recap: where we are

[For series readers: Skip to “Today’s Focus” below]

[For new readers: Here is what happened so far.]

What happened previously: Ms. Rao was initially sceptical about using AI for legal work, questioning whether it could handle complex board report requirements. Arjun demonstrated that Claude understands section 134 legal requirements and can organise them systematically. They successfully created professional group 1 governance content and sophisticated group 2 financial analysis that impressed Ms. Rao with investment-grade quality. In Part 4, they tackled the most legally sensitive content – directors’ personal responsibility statements – proving the approach works even for liability-sensitive disclosures.

The step-by-step approach we have developed:

- Document-based context (upload comprehensive company info)

- Strategic analysis (test Claude’s understanding)

- Step-by-step improvement (refine drafts through focused prompts)

- Human oversight (lawyer review and validation)

Groups completed so far:

- Group 1: Company identity and governance

- Group 2: Financial performance and highlights

- Group 3: Directors’ statements and professional judgment

- Group 4: External stakeholders and audit relations (today’s focus)

Nova AgriTech Quick Profile:

- Agri-tech company with strong growth trajectory

- Facing an auditor qualification on revenue recognition timing

- Need to balance transparency with competitive positioning

- Board of 5 directors managing complex stakeholder relationships

Today’s focus: Group 4 – Communicating with external stakeholders and auditors through the board report

In this article, follow Arjun and Ms. Rao as they tackle the most sensitive parts of the board report — the sections that are scrutinised by investors, regulators, and auditors, where every word matters.

What you will learn:

- How to create context documents that help AI understand stakeholder concerns

- How to share information clearly without revealing too much to competitors

- How to respond to auditor comments in a constructive and professional way

By the end, you will know:

- Why external communications require a different tone and strategy

- How to build strong, respectful relationships with auditors

- Smart ways to present related party transactions without raising red flags

Section 134 board report disclosures: Auditor Comments, Investments and RPTs (Group 4)

“Three groups down, three to go,” Ms. Rao said, settling into her chair with her morning coffee.

The conference room at Khanna Legal Solutions felt more energised now. Their group 3 breakthrough had proven that a step-by-step approach could handle even ‘director’s statement and professional judgment’ communications.

But Arjun noticed tension in her posture as she reviewed their progress.

“Nova’s board meets next week,” she continued, glancing at her calendar. “We are making excellent time, but group 4 presents a different challenge.”

Arjun looked up from organising the Nova AgriTech files. After three successful groups, he felt confident in their methodology.

“How is group 4 different? We have proven the approach works for governance facts, financial analysis, and directors’ statements and professional judgment disclosures.”

Ms. Rao pointed to the group 4 requirements on her screen.

“External scrutiny,” she said simply.

“Everything we have drafted so far stays within Nova’s governance circle – board members, management, institutional investors, group 4 disclosures face public examination.”

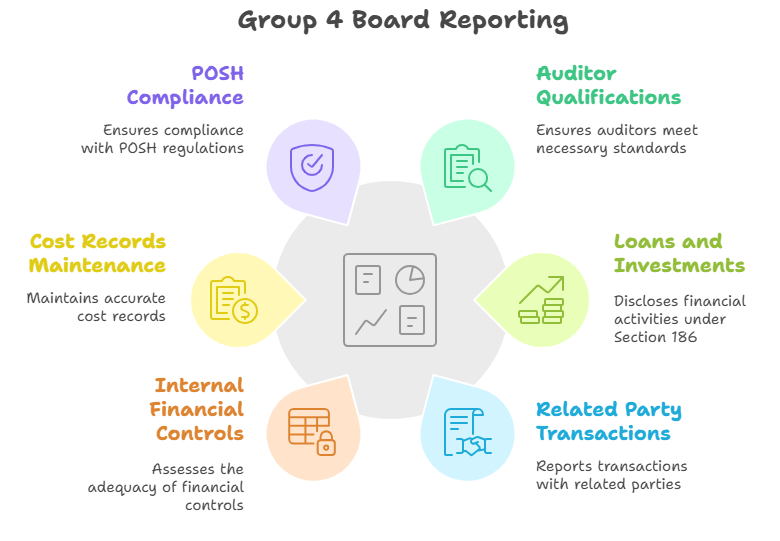

She highlighted the requirements:

- Section 134(3)(f): Auditor qualifications and comments

- Section 134(3)(g): Loans, guarantees, and investments under section 186

- Section 134(3)(h): Related party transactions (Form AOC-2)

- Rule 8(5)(9): Internal financial controls adequacy

- Rule 8(5)(10): Cost records maintenance disclosure

- Rule 8(5)(11): POSH compliance statement

“Auditors will scrutinise every word. Regulators might examine our section 186 disclosures. Competitors could analyse our related party transactions for strategic intelligence.”

Arjun understood immediately. “So our prompting strategy needs to balance transparency with competitive sensitivity.”

“Exactly. And there is another complexity,” Ms. Rao added, pulling up Nova’s audit file. “We are not just reporting good news anymore.”

“What do you mean?” Arjun asked, though he suspected he knew where this was heading.

Ms. Rao opened Nova’s draft audit report.

“Nova’s auditors flagged a qualification regarding revenue recognition timing on their agricultural contract with the Haryana Agricultural Department.”

She read from the audit notes: “The auditors question whether Nova should recognise the full ₹25 crores contract value over three years versus recognising it based on actual service delivery milestones.”

“It is not a major issue,” she continued, “but it requires board response under section 134(3)(f). And here is the challenge – how do we respond professionally without appearing defensive, while maintaining confidence in our revenue recognition policies?”

Arjun leaned back, considering the complexity.

This was not about presenting Nova’s strengths anymore. This was about addressing external criticism while maintaining credibility.

“Traditional approach would be to craft careful, diplomatic language that acknowledges the auditor’s concern while defending our position,” he mused.

“But can Claude handle that kind of nuanced professional relationship management?”

“That is what we are about to find out,” Ms. Rao replied.

“If Claude can help us navigate sensitive external disclosures professionally, it proves our approach works for the most challenging board report requirements.”

Preparing for the section 134 audit and related party transaction disclosures in the board report

“We need to enhance our document-based context strategy,” Arjun said, opening a fresh document.

“Groups 1-3 required a comprehensive business context. Group 4 requires stakeholder relationship context.”

He began typing rapidly:

Nova AgriTech External Stakeholder Context – Group 4 Disclosures

Auditor relationship status:

- Audit firm: M/s Khanna & Associates, Chartered Accountants

- Lead auditor: CA Rajesh Malhotra (3rd year on Nova engagement)

- Audit qualification: Revenue recognition timing on the Haryana Agricultural Department contract

- Auditor’s specific concern: ₹25 crores contract recognised upfront vs. milestone-based recognition

- Management position: Contract terms justify upfront recognition based on a committed government partnership

Section 186 investment profile:

- Subsidiary investment: ₹2.8 crores in Nova AgriTech Solutions Pvt Ltd (October 2024)

- Strategic rationale: Field operations and customer support capabilities

- Board approval: Unanimous approval in the October 12, 2024, board meeting

- Regulatory compliance: All section 186 limits and procedures followed

Related party transaction context:

- Founder service agreements: Technology consulting services from Amit Verma’s previous entity

- Board member connections: Mr. Suresh Patel represents GreenTech Ventures (institutional investor)

- All transactions: Conducted at arm’s length with proper board approvals

- Materiality: No transactions exceed prescribed thresholds for shareholder approval

Compliance status:

- Internal financial controls: Implemented with CFO certification

- Cost records: Not applicable (technology services company)

- POSH compliance: Policy implemented, no complaints received during FY 2024-25

Ms. Rao reviewed the stakeholder context document.

“This seems fine. You have captured the relevant facts that we will require to communicate each disclosure in group 4 effectively.”

“The key insight,” Arjun explained, “is that Claude needs to understand we are not just reporting to Nova’s board anymore. Every word will be examined by external parties with different interests and perspectives.”

Testing Claude’s understanding of external stakeholders’ concerns in the board report

“Before we ask Claude to draft sensitive responses,” Arjun said, uploading the enhanced context document, “let us test whether it understands the stakeholder relationship complexities.”

Ms. Rao nodded. “Smart approach. We learned from groups 1-3 that understanding comes before drafting.”

Arjun began crafting the first prompt, knowing this would set the foundation for all group 4 work:

“We are about to test whether Claude can navigate the most sensitive aspect of board report drafting,” he said, fingers poised over the keyboard.

Arjun’s first prompt for group 4:

“Based on the Nova AgriTech documents uploaded (external stakeholder context), analyse the Group 4 external disclosure challenges for their FY 2024-25 board report:

Section 134(3)(f) – responding to the auditor’s qualification on revenue recognition,

Section 134(3)(g) – disclosing section 186 investments transparently,

Section 134(3)(h) – related party transaction disclosure without competitive disadvantage, Rule 8(5)(9-11) – internal controls and compliance statements.

Explain how these four disclosure areas require different communication strategies than the internal governance and financial disclosures we have covered in Groups 1-3. Focus on the stakeholder relationship management challenges and how external scrutiny affects disclosure language and positioning.”

Click here to see the conversation with Claude.

- How Claude framed the auditor qualification in strategic terms

Ms. Rao leaned forward as Claude’s response appeared on screen – a focused, professionally structured analysis that immediately demonstrated a sophisticated understanding of external stakeholder dynamics.

“This is workable,” she said, reading through Claude’s opening.

“I liked the strategic framing: ‘These external-facing disclosures must balance transparency with stakeholder confidence while managing competitive positioning.'”

Arjun nodded, impressed by Claude’s immediate focus.

“Have a look at how it clearly identified the fundamental challenge: ‘a fundamentally different communication paradigm compared to internal governance disclosures.’ Claude understood we are not just reporting facts anymore – we are managing stakeholder relationships.”

- How Claude framed the auditor qualification

“The auditor qualification response is particularly sophisticated,” Ms. Rao observed, pointing to the screen. “Claude wrote: ‘The Board has thoroughly evaluated the auditor’s observations regarding revenue recognition timing… Management’s position is supported by a comprehensive legal analysis of contract terms.'”

“What I found very impressive,” Arjun said, “is how Claude positioned this as professional dialogue rather than a defensive response. Look at this language: ‘will continue dialogue with auditors to address their concerns while maintaining appropriate accounting standards compliance.’ That maintains management authority while showing responsiveness.”

Ms. Rao continued reading. “And notice the strategic insight about external versus internal communication: ‘Unlike internal discussions that can acknowledge uncertainty, external disclosure must project confidence while showing responsiveness to auditor concerns.’ That’s exactly the professional balance we needed.”

- Claude explained section 186 investment without giving away the strategy

“The section 186 investment disclosure demonstrates Claude’s understanding of capital allocation storytelling,” Arjun observed, reviewing the subsidiary investment section.

Ms. Rao highlighted Claude’s strategic language: “Listen to this positioning: ‘The Company strategically invested ₹2.8 crores in Nova AgriTech Solutions Private Limited to strengthen field operations and customer support capabilities.’ That immediately frames it as strategic value creation rather than capital deployment.”

“The external versus internal distinction is particularly insightful,” Arjun added.

“Claude wrote: ‘Internal communications can focus on operational details and risk assessment, while external disclosure must emphasise strategic rationale and value creation potential.’ That captures exactly why external disclosures require different language.”

“And notice how Claude connected the investment to broader strategy without revealing operational details,” Ms. Rao noted.

“‘This investment directly supports our market expansion strategy and positions the subsidiary to capture emerging opportunities’ – strategic benefit without competitive vulnerability.”

- Balancing transparency and sensitivity in related party transactions

“The related party transaction section demonstrates Claude’s most sophisticated stakeholder communication understanding,” Ms. Rao said, studying the disclosure approach.

“Look at this strategic language,” she continued.

“Claude wrote: ‘Technology consulting services from the founder’s previous entity were essential for maintaining technical continuity during our growth phase, with pricing benchmarked against market standards.’ That provides business rationale while emphasizing arm’s length treatment.”

Arjun was particularly impressed with the institutional investor handling: “Notice how Claude addressed the GreenTech Ventures connection: ‘Board member Mr. Suresh Patel’s representation of institutional investor GreenTech Ventures enhances our strategic oversight while maintaining independence through established governance protocols.'”

“That language acknowledges the relationship while positioning it as a governance strength rather than a potential conflict,” Ms. Rao observed.

“And the external versus internal insight is spot-on: ‘Internal governance discussions can acknowledge potential conflicts and mitigation strategies, while external disclosure must emphasise the business rationale and governance safeguards.'”

- Compliance communication excellence

“The internal controls and compliance section shows Claude understands confidence projection,” Arjun noted, reviewing the Rule 8(5) disclosures.

Ms. Rao highlighted the professional tone: “Listen to this language: ‘The Company has implemented comprehensive internal financial controls with CFO certification ensuring accuracy and reliability of financial reporting.’ That projects control effectiveness without revealing specific operational details.”

“The POSH compliance disclosure is particularly well-handled,” Arjun added. “‘Our POSH compliance framework operates effectively with zero complaints received during FY 2024-25, reflecting our commitment to maintaining respectful workplace standards.’ Professional confidence without defensive positioning.”

- The strategic communication framework

“What convinced me that Claude truly understands external stakeholder complexity,” Ms. Rao said, “is how it consistently distinguished external from internal communication needs throughout each section.”

She pointed to Claude’s stakeholder relationship management analysis: “Claude identified four distinct challenges: investor relations requiring transparency with confidence, regulatory positioning demonstrating proactive compliance, competitive considerations avoiding strategic vulnerabilities, and audit relationship management maintaining professional relationships.”

“The fundamental insight is powerful,” Arjun observed.

“Claude wrote: ‘The fundamental difference in Group 4 disclosures lies in their dual audience nature – satisfying regulatory requirements while managing multiple stakeholder relationships and maintaining competitive positioning.'”

“That captures exactly why external disclosures require sophisticated communication strategies that internal governance communications do not face,” Ms. Rao agreed.

The real test: Can Claude draft the final board report language?

Ms. Rao concluded, “But I want to see if Claude can translate this analysis into actual disclosure language that balances all these competing considerations?”

Arjun understood the complexity. “It is one thing to analyse stakeholder dynamics strategically. It is another to craft specific disclosure language that addresses auditor qualifications diplomatically while maintaining management credibility.”

“Exactly. The analysis is investment banking quality, but now we need legally compliant, professionally diplomatic disclosure drafting.”

“Time to test Claude’s ability to produce final, filing-ready language,” Arjun said, crafting the second prompt.

Arjun’s second prompt – complete group 4 disclosure drafting:

“Based on your strategic analysis, now draft the complete Group 4 disclosures for Nova AgriTech’s FY 2024-25 board report in final board report format. Structure as:

(1) Section 134(3)(f) – Board’s response to auditor qualifications and comments

(2) Section 134(3)(g) – Loans, guarantees and investments under section 186

(3) Section 134(3)(h) – Related party transactions (narrative for Form AOC-2)

(4) Rule 8(5)(9) – Internal financial controls adequacy statement

(5) Rule 8(5)(10) – Cost records maintenance disclosure

(6) Rule 8(5)(11) – POSH compliance statement

Write in formal board report language suitable for Nova’s institutional investors and regulatory filings.

Maintain the strategic positioning from your analysis while ensuring complete legal compliance and professional tone throughout.”

Click here to see the conversation with Claude and here to see Claude’s response in PDF.

Professional excellence in sensitive Board report disclosures

Claude delivered a comprehensive 5-page board report section that immediately demonstrated professional legal drafting capability.

“Look at this professional structure,” Ms. Rao said, reviewing the auditor qualification response. “‘Management Position,’ ‘Board’s Assessment,’ ‘Ongoing Engagement.’ Claude organised the response strategically while maintaining a diplomatic tone.”

Arjun was particularly impressed with the technical language: “Notice how Claude wrote: ‘The Board’s position, supported by legal opinion and technical consultation, is that the contract terms justify upfront revenue recognition based on unconditional commitment from government counterparty.’ That is exactly the confident but non-defensive positioning we needed.”

“The section 186 disclosure demonstrates perfect regulatory compliance,” Ms. Rao observed.

“Board resolution date, investment quantum, compliance confirmation – all the mandatory elements structured professionally with strategic rationale.”

“And look at the related party transaction handling,” Arjun added.

“Claude wrote: ‘Mr. Suresh Patel serves as Director representing GreenTech Ventures, an institutional investor in the Company. This representation enhances strategic oversight while maintaining board independence through established governance protocols.’ That turns a potential concern into a governance strength.”

“The compliance statements are particularly well-crafted,” Ms. Rao noted, reading through the internal controls and POSH disclosures. “Professional confidence without revealing operational vulnerabilities.”

Human review of external disclosures in the board report

She leaned back, satisfied.

“Group 4 complete. Claude translated sophisticated stakeholder analysis into filing-ready disclosure language that meets both legal requirements and business communication standards.”

“While we might not have found any glaring mistakes by Claude while preparing group 4 disclosures,” Arjun reflected, “it is always advisable to ensure that the response created is legally sound and factually correct. That can only be done through human review. Or as the techies say – human in the loop.”

What did we learn about AI’s role in handling sensitive disclosures in the board report?

“What have we learned about professional AI collaboration through group 4?” Arjun asked, gathering their systematic documentation.

Ms. Rao considered their progression thoughtfully.

“Three key insights,” she said.

“First, document-based context strategy scales beautifully. The enhanced stakeholder context document enabled Claude to understand relationship dynamics that would have taken multiple prompts to explain.”

“Second,” Arjun added, “strategic analysis before drafting produces superior results. Claude’s stakeholder relationship framework informed every word of the actual disclosures.”

“Third, and most importantly,” Ms. Rao concluded, “external stakeholder disclosures require the highest level of human oversight. Even with Claude’s sophisticated understanding, professional judgment about competitive sensitivity and regulatory implications remains essential.”

Professional AI collaboration framework validation:

- Systematic methodology over ad-hoc experimentation

- Progressive complexity building rather than attempting advanced tasks immediately

- Document-based context strategy for comprehensive understanding

- Strategic analysis before drafting for superior professional results

- Human oversight for sensitive disclosures, ensuring accuracy and appropriateness

Key takeaways:

- External stakeholder disclosures require enhanced context, strategy, and different communication approaches

- Strategic analysis before drafting enables sophisticated professional positioning

- AI collaboration works exceptionally well for complex stakeholder relationship management when properly guided

Progress Check: You have now seen how to handle the most externally sensitive board report content using AI. This stakeholder management foundation prepares you for group 5’s risk and CSR communications, where we will tackle forward-looking assessments and social impact storytelling.

Next steps

If you are following the series:

- Next: Part 6 covers group 5 (Risk Management and CSR Disclosures)

- Previous: Part 4 covered group 3 (Directors’ Statements and Professional Judgment)

If you are new to the series:

- Start from Part 1 for the complete methodology

- Jump to Part 8 to see the live demonstration

Want to try this yourself?

- Create comprehensive stakeholder context documents before prompting

- Test AI’s understanding of relationship dynamics before requesting drafts

- Apply enhanced human review for externally sensitive content

Complete article series

- Part 1: Getting started

- Part 2: Building the foundation (Group 1)

- Part 3: Financial performance and capital management (Group 2)

- Part 4: Directors’ statements and professional judgment (Group 3)

- Part 5: External stakeholders and audit relations (Group 4) ← You are here

- Part 6: Risk management and CSR disclosures (Group 5)

- Part 7: Final assembly and compliance verification (Group 6)

- Part 8: Live demonstration – real-time board report creation

This stakeholder relationship management foundation sets the stage for the risk and CSR communications covered in Part 6, where we will see how Claude handles forward-looking assessments and social impact storytelling while maintaining professional credibility.

Allow notifications

Allow notifications