Last verified: July 2026

In 2024, the Supreme Court looked hard at a question that decides how a cheque bounce case under Section 138 NI Act actually plays out. The question was blunt: can a trial court order an accused, not yet convicted, to hand over up to 20% of the cheque amount before a single witness has been examined? For years, the answer on the ground had been a near-automatic yes.

Trial courts across the country had been reading the interim-compensation power as a formality. A complaint was filed, the accused appeared, and almost reflexively came the order to deposit 20% of the cheque value under Sec. 143A. The logic seemed clean: the cheque bounced, so make the drawer put money on the table. In practice, though, that turned the provision into a settle-or-pay squeeze. Drawers with a genuine defence were paying up simply to avoid the deposit and the pressure that came with it.

Then a two-judge bench of the Supreme Court pulled the brakes. It held that the power to award interim compensation is discretionary, not mandatory. The word in the statute is “may”, not “shall”. A trial court, the Court said, must actually apply its mind before ordering a pre-conviction payment: is there a prima facie case, does the accused have a plausible defence, what is the accused’s financial condition, and are the reasons recorded in the order? Mechanical grants were rejected. The 20% was no longer a rubber stamp.

Why should you care about a single interlocutory ruling? Because it quietly rewired the incentives on both sides of every cheque dishonour matter in India. If you’re a payee chasing a bounced cheque, one of your sharpest pressure levers just became conditional: you can no longer assume the court will squeeze a 20% deposit out of the drawer on the strength of the bounce alone. If you’re a drawer who has just torn open a 30-day demand notice, your settlement maths changed overnight, because a plausible defence, put on the record early, can now hold off that pre-conviction payment. And if you’re the advocate on either side, your Sec. 143A application (or your reply to one) now has to carry a real argument, not a fill-in-the-blanks form: the prima facie case, the accused’s financial condition, and reasons the court can actually record.

That single shift is why this guide starts here, and not with the timeline everyone else leads with.

Here’s the catch: most explainers you’ll find still describe the old, near-automatic regime. They tell you the timeline and the punishment, and stop. That’s the easy half. The hard half, the half that wins or loses matters, is knowing how to file a defensible complaint and how to defend one, with the current case law in your hand. This guide does both.

A cheque bounce case under Section 138 of the Negotiable Instruments Act, 1881 is a criminal complaint, filed by the payee before a Magistrate, not a police FIR, when a cheque for a legally enforceable debt is returned unpaid. Punishment runs up to two years’ imprisonment, a fine of up to twice the cheque amount, or both.

What follows answers the fast questions first, punishment, timeline, notice, in the next sixty seconds. Then it walks the full file-and-defend workflow: how a payee builds and files a complaint, and how a drawer or accused defends one, section by section, with verified rulings.

What is a cheque bounce case under Sec. 138 NI Act?

Someone hands you a cheque to clear a debt. You deposit it. Days later, the bank slaps you with a return memo: “funds insufficient”. That single slip of paper is where a cheque bounce case under Section 138 NI Act begins, and where a lot of payees promptly do the wrong thing. Knowing exactly what the offence is, before you react, is what separates a complaint that survives from one that gets thrown out at the threshold.

At its core, Section 138 of the Negotiable Instruments Act, 1881 makes it a criminal offence to issue a cheque for a legally enforceable debt that is then returned unpaid for want of funds, provided the payee follows the notice-and-wait procedure and the drawer still doesn’t pay. It’s not enough that a cheque bounced. The offence is a structure with moving parts, and every part has to be in place. Miss one, and there is no Sec. 138 case, however aggrieved you feel.

That structure is why the constituent acts matter so much. The Supreme Court in K. Bhaskaran v. Sankaran Vaidhyan Balan, (1999) 7 SCC 510 broke the offence into a chain of distinct acts: drawing the cheque, presenting it, its dishonour, the giving of notice, and the drawer’s failure to pay. We’ll return to that chain when we get to jurisdiction, because where those acts happen decides which court hears the case. For now, hold on to the idea that Sec. 138 is cumulative, not a single event.

The five ingredients of a Sec. 138 offence

Think of the offence as five ingredients that must all be present at once:

- A cheque is drawn for the discharge of a legally enforceable debt or other liability (not a gift, not an advance for something never delivered).

- The cheque is presented to the bank within its period of validity.

- The cheque is returned unpaid because the funds in the account are insufficient, or the amount exceeds the arrangement with the bank.

- The payee makes a written demand for the cheque amount within 30 days of learning of the dishonour from the bank.

- The drawer fails to pay the amount within 15 days of receiving that demand.

Only when the fifth ingredient is satisfied, the drawer’s silence past 15 days, does the offence actually complete. Before that, there is no offence to complain about. This is the single most misunderstood feature of the section, and it trips up payees who rush to court the moment the cheque bounces.

What counts as “dishonour”

Not every bank rejection is the kind of dishonour Sec. 138 punishes. The section bites when a cheque is returned because the amount in the account is insufficient, or because it exceeds the arrangement the drawer has with the bank. Both are expressly covered by the language of the provision. So “funds insufficient” is the textbook case.

Courts have read this to cover more than a literal shortage. An “account closed” return is treated as dishonour for insufficiency, because a closed account by definition cannot honour the cheque. So is a “stop payment” instruction in most circumstances, once a legally enforceable debt exists, because a drawer cannot escape liability simply by instructing the bank not to pay. But (and this is the part many drawers cling to) a stop-payment on a cheque where no debt was ever owed is a different animal, and it loops back to the “legally enforceable debt” requirement below.

Technical dishonour: when Sec. 138 does and doesn’t bite

Then there is the grey zone: technical dishonour. What happens when a cheque is returned for “signature differs”, “image not clear”, or because it was presented before its date? Here the picture is genuinely mixed, and the outcome turns on facts. A return for a reason that has nothing to do with the state of the account, and nothing to do with any attempt to defeat payment, may fall outside Sec. 138, because the section is aimed at insufficiency of funds and exceeding the arrangement.

In practice, though, courts look at intent and effect. If a signature mismatch or a “payment stopped” is really a device to avoid an admitted debt, the section can still apply. If it’s a bona fide banking technicality with no debt-avoidance behind it, prosecution gets shaky. The safe reading for a payee: don’t assume every non-fund reason gives you a Sec. 138 case, and get the return memo reason in writing before you decide.

“Legally enforceable debt or other liability”

The phrase that decides most cheque bounce cases isn’t “dishonour” at all. It’s “legally enforceable debt or other liability”, which sits in the Explanation to Sec. 138. If the cheque wasn’t issued to discharge a debt the law would enforce, the whole prosecution collapses, no matter how cleanly the notice-and-wait steps were followed.

So what isn’t legally enforceable? A debt barred by limitation. A “debt” arising from an unlawful or wagering transaction. A cheque issued for a liability that never crystallised. This one phrase is where the payee’s case and the accused’s defence eventually meet, and we hand it to the defence track in a later section. For the payee, the lesson is upstream: before you file, be sure you can prove the debt, not just the bounce.

Is a cheque bounce case civil or criminal, and is it an FIR or a complaint?

“Should I go to the police?” is the first question most payees ask after a cheque bounces, and it’s the wrong first question. The confusion is understandable: the word “criminal” makes people picture a police station and an FIR. But a cheque bounce case runs on a track of its own, and getting the track wrong wastes weeks you may not have, given the tight limitation period.

The short answer is that a Sec. 138 case is criminal in nature but private in initiation. It’s a criminal offence, punishable with imprisonment and fine, yet it does not start with a police FIR. It starts with a written complaint that the payee (or holder in due course) files directly before a Magistrate. There’s no police investigation, no charge sheet. The complainant runs the case.

Why Sec. 138 is criminal but a private complaint, not an FIR

The reason lies in Section 142 of the Negotiable Instruments Act, 1881. That provision says a court can take cognizance of a Sec. 138 offence only on a written complaint made by the payee or the holder in due course of the cheque. Police have no role in registering or investigating it. This is why “I’ll lodge an FIR” gets a payee nowhere: there is no FIR to lodge for a bare cheque bounce. If you want to understand the mechanics of a payee-driven prosecution more deeply, our explainer on how a criminal complaint before a Magistrate is drafted and filed walks through the procedure that Sec. 142 assumes.

Why did Parliament build it this way? Because the offence is essentially a commercial default dressed in criminal clothing. Loading the police with lakhs of cheque disputes would have been unworkable, and the real complainant, the person owed money, is far better placed to prosecute than an overburdened investigating officer.

How cheque dishonour was criminalised

It wasn’t always a crime at all. Before 1988, a bounced cheque was purely a civil matter: sue for the money and wait. Cheque dishonour had become a bad-cheque epidemic, and civil recovery was too slow to deter it. Parliament responded by inserting Sec. 138 into the NI Act through an amendment in 1988, criminalising dishonour for the first time and giving commercial India a credible deterrent that a slow civil suit could not.

That history explains the section’s odd hybrid character. It punishes like a crime but is prosecuted like a private grievance, because its whole point was to hand the aggrieved creditor a sharp, self-driven remedy. Understanding this origin helps you read every later development, from the compensation-first rulings to the interim-compensation machinery, as variations on a single theme: recovery with teeth.

Cognizable vs non-cognizable, bailable vs non-bailable

How is the offence classified? A Sec. 138 offence is non-cognizable, which is another reason the police stay out: for non-cognizable offences, an officer cannot arrest or investigate without a Magistrate’s direction, and here cognizance runs entirely through the private complaint route. It is also a bailable offence, so an accused is entitled to bail as of right rather than at the court’s mercy.

Is the distinction academic? Not for the accused. Because the offence is bailable, the fear of immediate arrest that people associate with a “criminal case” is largely misplaced here. The pressure in a cheque bounce matter is financial and procedural, not custodial, and we’ll come back to that when we deal with bail and appearance on the defence side.

Did the BNS 2023 or BNSS replace Sec. 138?

Here’s a worry that has spread since the new criminal codes came in: did the Bharatiya Nyaya Sanhita, 2023 or the Bharatiya Nagarik Suraksha Sanhita, 2023 wipe out Sec. 138? The answer is no. The NI Act is a special statute, and Sec. 138 lives inside it, untouched by the general criminal codes. What changed is the procedural wrapper: the BNSS replaced the old Code of Criminal Procedure for general process, but that procedure applies subject to the NI Act, not over it.

The Supreme Court confirmed this alignment in 2025. In Sanjabij Tari v. Kishore S. Borcar, 2025 INSC 1158, the Court directed that there is no requirement to issue a pre-cognizance summons to the accused under Sec. 223 of the BNSS in an NI Act complaint, precisely because the special procedure of the NI Act governs. Where the NI Act provides a special procedure, it prevails over the general provisions of the BNSS. The practical takeaway follows: don’t let anyone tell you the new codes killed the cheque bounce remedy. They didn’t. If you ask us, this is one of those misconceptions that costs people real time, because a drawer who believes the section is dead simply ignores the notice, and pays for it later.

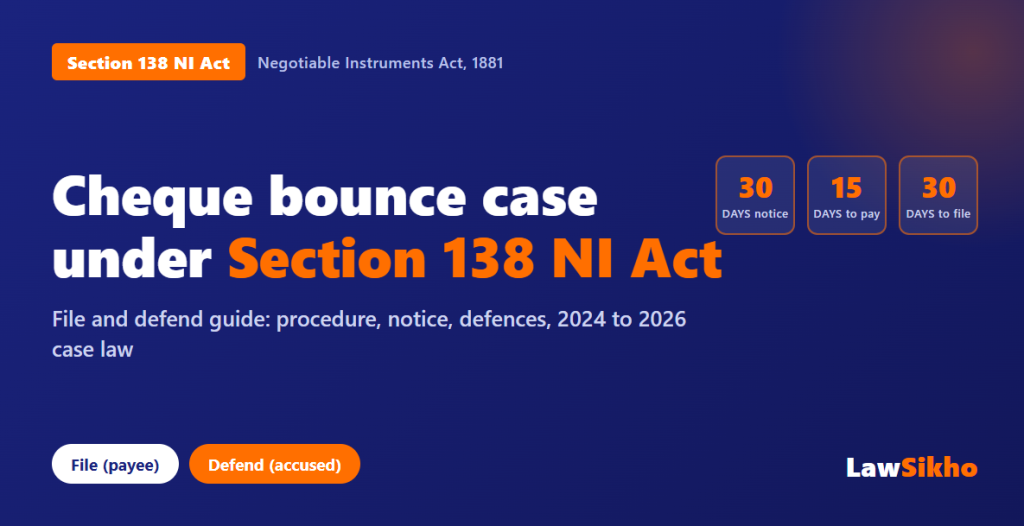

Cheque bounce punishment and the 30/15/30-day timeline

Two numbers dominate every cheque bounce case: the punishment ceiling and the deadlines. Get the punishment wrong and you’ll either over-threaten or under-prepare. Miss a deadline and it doesn’t matter how strong your debt is, the complaint is dead on arrival. This section pins both down, because they’re the facts an AI Overview will quote at you, and the facts a careless complainant most often botches.

Cheque bounce punishment under Sec. 138 is imprisonment for up to two years, or a fine that may extend to twice the cheque amount, or both. The offence completes only after a three-part clock has run: a 30-day window to send the demand notice, a 15-day window for the drawer to pay, and a 30-day (one month) window to file the complaint once the cause of action arises. Those are the load-bearing numbers of the entire remedy.

The punishment, and what courts actually award

On paper, the punishment looks fierce: up to two years inside, plus a fine of up to double the cheque value. In the real world, jail is the exception, not the rule. Courts have leaned heavily toward treating Sec. 138 as a compensation mechanism, using the fine (which can run to twice the cheque amount) to make the payee whole rather than sending drawers to prison. The Supreme Court’s approach in Meters and Instruments Pvt. Ltd. v. Kanchan Mehta, (2018) 1 SCC 560 captured this compensation-first thrust, encouraging disposal that puts money back in the complainant’s hands.

So can you actually recover the full cheque amount, or only “a fine”? In practice, the fine is the recovery vehicle. Because it can be set at up to twice the cheque value, courts routinely fix it to cover the cheque amount (and often interest and costs), then direct that the fine be paid to the complainant as compensation. That’s how a criminal complaint ends up delivering the money, even though its formal language is about punishment.

The three deadlines that make or break the case

Now the deadlines, and they are unforgiving. First, once the bank tells you the cheque has bounced, you have 30 days to send a written demand notice to the drawer. Second, the drawer then has 15 days from receiving that notice to pay the cheque amount. Third, and this is where people slip, the offence is complete only on the expiry of that 15-day window, so the cause of action arises on the 16th day.

From that 16th day, Section 142(b) of the Negotiable Instruments Act, 1881 gives you one month to file the complaint. File on day one of that month or day thirty, but not on day thirty-one, unless you can persuade the court to condone the delay under the proviso (which is discretionary and needs a real explanation, not an afterthought). The whole sequence is best held as a single mental picture: bounce, then 30, then 15, then the 16th-day trigger, then 30 to file. Fair warning: treating the 15-day window as optional is the fastest way to file a premature, and fatal, complaint.

How long a cheque stays valid for presentation

There’s a fourth clock people forget, sitting before all the others: the cheque’s own validity. A cheque is valid for presentation for three months from the date written on it (banks stopped honouring the old six-month cheques years ago). Present it after it goes stale and the bank returns it for validity, not insufficiency, and that return generally won’t support a Sec. 138 case.

What if the cheque is undated, or bears a wrong date? Present it within three months of the date it actually carries, and if it’s undated, the safest course is to complete it properly before presentation, an issue that links to the blank-cheque questions we deal with on the defence side. The rule to remember is simple: the validity clock starts on the cheque’s face date, and everything else, notice, pay window, filing, only begins once a valid presentation has been dishonoured.

Cheque bounce timeline table

The whole timeline, on one screen:

| Action | Time limit | Counted from |

|---|---|---|

| Present the cheque | Within validity (3 months / date on cheque) | Date on the cheque |

| Send demand notice | 30 days | Receipt of bank return memo |

| Drawer’s window to pay | 15 days | Receipt of the notice |

| Cause of action arises | Day 16 | Expiry of the 15-day pay window |

| File the complaint | 30 days (1 month) | Date cause of action arose (Sec. 142(b)) |

How to file a cheque bounce case: step-by-step procedure (complainant track)

You’re the payee. The cheque bounced, and you want to move, not read theory. This is the “file” track: a clean, ordered procedure to take a cheque bounce case from the return memo to a judgment, with the documents and costs you’ll actually need. It doubles as the answer to the most common query on this topic, how to file a cheque bounce case, and it’s written so a passing reader who lands here first still gets the full picture.

The procedure to file a cheque bounce case is a fixed sequence: present the cheque, collect the bank’s return memo, issue a written demand notice within 30 days, wait out the drawer’s 15-day pay window, and then file a complaint before the Magistrate within 30 days of the cause of action. Do them in order, because each step is a legal precondition for the next.

The 7-step procedure

Here is the sequence, step by step:

- Present the cheque to your bank within its validity and, if it bounces, obtain the return memo (the cheque return slip stating the reason, usually “funds insufficient”).

- Within 30 days of learning of the dishonour, send a written demand notice to the drawer calling on them to pay the exact cheque amount within 15 days.

- Wait out the 15-day period from the drawer’s receipt of the notice. If they pay, the matter ends; if they don’t, the offence is complete on the 16th day.

- Draft the criminal complaint under Sec. 138, setting out the transaction, the debt, the cheque, the dishonour, the notice, and the drawer’s failure to pay.

- File the complaint before the Magistrate having jurisdiction (the court where your bank branch is located), within one month of the cause of action, along with the supporting documents and your list of witnesses.

- The Magistrate takes cognizance, may record the complainant’s evidence on affidavit, and issues summons to the accused.

- The matter goes to summary trial; evidence is led, arguments heard, and the court delivers judgment, conviction with fine/compensation, or acquittal.

That’s the spine of the whole remedy. Everything else in this guide, notice drafting, jurisdiction, defences, interim compensation, hangs off one of these seven steps.

Documents required to file

A complaint is only as strong as the paper behind it. Before you file, assemble this checklist:

- The original dishonoured cheque.

- The bank’s return memo (cheque return slip) showing the reason for dishonour.

- A copy of the demand notice, plus the postal dispatch receipt and the acknowledgement or tracking proof.

- The document proving the debt: the loan agreement, invoice, ledger, or written acknowledgement that shows why the drawer owed you the cheque amount.

- The complaint itself, with your list of witnesses.

- An affidavit of the complainant’s evidence under Section 145 of the Negotiable Instruments Act, 1881, which lets the complainant lead evidence on affidavit rather than only orally.

The debt document is the one people underprepare. The bounce proves the cheque was dishonoured; it does not, by itself, prove the debt. When the drawer later argues “no legally enforceable debt”, your invoice or a properly drafted loan agreement or promissory note is what carries the day. In our view, this is where most self-filed complaints are quietly weak.

Court fee and realistic cost and duration

What does it cost to file? Court fee on a Sec. 138 complaint is state-specific and, in most states, modest relative to the cheque amount, and in several High Court jurisdictions the fee is structured as a small slab tied to the amount claimed. (These rates vary by state and are indicative only; confirm the current schedule for your state before filing, as court-fee tables change.) The larger cost is usually professional fees, which vary widely by city and by the complexity of the matter and whether it runs to full trial.

And the honest question everyone asks: how long does a cheque bounce case take in India? Despite a statutory push for six-month disposal, the practical reality in busy metropolitan courts is often longer, frequently a year or more, because of docket load and the accused’s appearances. Set your expectations accordingly, and treat the criminal complaint as one lever, not a guaranteed fast recovery. We’ll come back to why running a parallel civil suit sometimes makes sense.

Can the police file it, or only the payee?

To close the loop from the earlier section: only the payee or the holder in due course can set a Sec. 138 case in motion, by filing the written complaint. The police cannot file it for you, and there is no FIR. The “complainant” is you, the person the cheque was meant to pay. If a lawyer or agent files, they do so on your behalf, not in place of you.

Why does this keep coming up? Because people transplant their instinct from theft or cheating cases, where you go to the police, onto a cheque bounce, where you go to the Magistrate. Get that straight at the outset and you’ll save yourself a wasted trip to the police station and, more importantly, weeks off your limitation clock.

The demand notice: format, timing and the drawer who dodges it

The demand notice is where a surprising number of cheque bounce cases are lost before they’re even filed. It looks like a formality, so people treat it as one, copying a template, guessing the amount, firing it off. Then, months later, the complaint is dismissed on a notice defect that could have been avoided in five minutes. This is the step to get obsessively right.

A valid Sec. 138 demand notice is a written demand, sent within 30 days of the dishonour, calling on the drawer to pay the cheque amount within 15 days. Its job is narrow and specific: identify the bounced cheque, state the reason for dishonour, and demand the cheque amount, no more, no less. Precision here is not pedantry; it’s the difference between a live case and a dead one.

What a valid Sec. 138 demand notice must contain

A sound notice should carry the cheque particulars (number, date, amount, drawee bank), a reference to the return memo and its reason, the underlying transaction in brief, and an unambiguous demand for the cheque amount within 15 days. Under Sec. 138, it is that demand for the cheque amount that the statute requires; get it wrong and the notice may not qualify.

The classic, fatal error is demanding the wrong sum. Payees often lump the cheque amount together with interest, penalty, legal costs, or other dues, and send a consolidated demand. Courts have repeatedly held that a notice must demand the cheque amount as such; a demand that muddles it with other claims can invalidate the notice. Demand the cheque amount cleanly. If you want interest or costs, that’s what your later prayer to the court, or a parallel civil suit, is for.

Deemed service: the drawer who refuses the notice

What if the drawer simply won’t accept the notice, refuses the registered post, “isn’t available”, dodges the postman? Drawers try this constantly, on the theory that if the notice is never “served”, the offence never completes. It doesn’t work. The Supreme Court in C.C. Alavi Haji v. Palapetty Muhammed, (2007) 6 SCC 555 held that where a drawer avoids or refuses a properly addressed registered notice, service is deemed to have been effected, drawing on the presumption in Section 27 of the General Clauses Act, 1897.

So the drawer who plays dead loses. Once you’ve sent the notice to the correct address by registered post and it’s returned “refused” or “not claimed”, the law treats it as served, and the drawer’s 15-day clock runs anyway. What experienced practitioners know is that this makes proof of correct dispatch far more important than proof of actual delivery: keep the postal receipt and the returned envelope, they’re your evidence of deemed service.

Wrong-address notices and mode of service

Deemed service has a hard limit, though: it presumes the notice went to the right address. Send it to a stale or wrong address and the presumption doesn’t rescue you, because the drawer never had a fair chance to receive it. Use the drawer’s correct, current address (ideally the one on record in your dealings), and send by registered post or speed post with acknowledgement.

Can you serve by email or WhatsApp? Treat these as supplements, not substitutes. Registered/speed post remains the safe, court-tested mode, and it generates the dispatch proof that deemed service relies on. Email or WhatsApp can corroborate that the drawer knew, but building your case solely on a WhatsApp “double tick” is a gamble no careful complainant should take. Belt and braces: registered post for the record, digital as backup.

Missing the 30-day notice deadline: is the case dead?

Suppose you blew the 30-day notice window. Is the cheque bounce case finished? Not necessarily. If the cheque is still within its validity, you can present it again, and a fresh dishonour gives you a fresh cause of action and a fresh 30-day notice window. This re-presentation route (which we cover in the trial section) is the escape hatch for a missed notice deadline.

But (and it’s a real but) you cannot manufacture endless bites at the apple after the cheque has gone stale. Once validity expires, re-presentation is off the table, and a missed notice deadline on the last valid presentation generally is fatal. The practical reality is that the 30-day notice clock is tight, don’t treat re-presentation as a safety net you can lean on casually; treat it as a genuine second chance you may get exactly once.

Where to file: cheque bounce case jurisdiction (and how it changed)

Ask “which court do I file my cheque bounce case in?” and you’d expect a one-line answer. For a few chaotic years, it was anything but. The jurisdiction rule for Sec. 138 has swung dramatically, and the swings left thousands of pending cases in limbo. Knowing the current rule is essential; knowing how it got here tells you why the rule is written the way it is, and helps you argue it if a drawer challenges your forum.

Today, a cheque bounce case is filed where the payee’s bank branch (the branch where the cheque was presented or deposited for collection) is located. That’s the settled position after the 2015 amendment to the NI Act. But it took a foundational 1999 ruling, a disruptive 2014 reversal, and a legislative correction to arrive there, and that arc is the story of this section.

The current rule: file where your bank branch is

Start with what applies now. Under Section 142(2) of the Negotiable Instruments Act, 1881, jurisdiction lies with the court within whose local limits the payee’s bank branch, the one where the cheque was delivered for collection, sits. For a payee, this is friendly: you sue on your home turf, not wherever the drawer happens to bank. Deposit the cheque at your branch, and that branch’s court is your forum.

Is this just a technicality? Far from it. Filing in the wrong court is one of the surest ways to have a complaint returned or dismissed, and a drawer who spots a jurisdiction defect will raise it fast. Anchor your complaint to your bank branch’s location and state that basis clearly in the complaint itself.

The jurisdiction arc: 1999 to 2015

Now the story, because it explains everything. In K. Bhaskaran v. Sankaran Vaidhyan Balan, (1999) 7 SCC 510, the Supreme Court in 1999 held that because the offence is made up of several acts (drawing, presentation, dishonour, notice, failure to pay), a complaint could be filed at any of the places where one of those acts occurred. Payees had broad choice, which suited creditors but let some forum-shop.

Then came the whiplash. In Dashrath Rupsingh Rathod v. State of Maharashtra, (2014) 9 SCC 129, the Court in 2014 narrowed jurisdiction sharply, ruling that a Sec. 138 case could be tried only where the drawee bank (the drawer’s bank) was located. The effect was chaos: payees who had filed near their own bank suddenly faced transfer of their cases to distant courts wherever the drawer banked, and thousands of pending matters were shuffled across the country. Parliament stepped in within months. The Negotiable Instruments (Amendment) Act, 2015 inserted the payee’s-bank-branch rule (Sec. 142(2) and Sec. 142A), legislatively restoring the creditor-friendly forum and settling the question for good.

Jurisdiction evolution table

The whole arc, at a glance:

| Stage | Ruling / amendment | Where you could file | Practical effect |

|---|---|---|---|

| Foundational (1999) | K. Bhaskaran | Any of the multiple cause-of-action places | Broad payee choice |

| 2014 | Dashrath Rupsingh Rathod | Only where the drawee (drawer’s) bank is | Nationwide chaos; mass transfers |

| 2015 to present | NI (Amendment) Act 2015 (Sec. 142(2)/142A) | Where the payee’s bank branch is | Payee-friendly forum restored |

Multiple cheques, multiple branches

What if a single dispute involves several cheques deposited at different branches, or a transaction that spans banks? The governing idea is still the presenting branch: the court where the cheque in question was delivered for collection has jurisdiction over that cheque. When multiple cheques from one transaction are in play, the amendment also allows related complaints to be tried together to avoid the same parties running parallel cases in scattered courts.

The sensible move is to consolidate where you can: present the cheques through one branch if the transaction allows, so your matters cluster in one forum. Scattering cheques across branches to create leverage tends to create logistical headaches for you, not the drawer. Keep it simple, and keep it where your bank branch is.

How to defend a cheque bounce case: the accused’s playbook

Flip the coin. You’re the one who issued the cheque, and now a summons has landed. The instinct is panic, then either ignore it or rush to pay. Both are mistakes. A Sec. 138 defence is a real, structured thing, but it operates under a presumption that tilts the field toward the complainant, and you need to understand that tilt before you can push back against it. This is the “defend” track: the accused’s playbook, told honestly, including where defences fail.

To defend a cheque bounce case, the accused must rebut a statutory presumption that the cheque was issued for a legally enforceable debt. The complainant doesn’t have to prove the debt up front; the law presumes it once the cheque and signature are admitted or established, and the burden shifts to the accused to raise a probable defence. Winning means attacking that presumption with evidence, not just denying the debt.

Who proves what: the Sec. 139 presumption and burden of proof

Everything turns on Section 139 of the Negotiable Instruments Act, 1881. It presumes that the holder of a cheque received it for the discharge of a debt or liability. The Supreme Court in Rangappa v. Sri Mohan, (2010) 11 SCC 441 settled, with a three-judge bench in 2010, that this presumption extends to the existence of a legally enforceable debt itself, not merely to the handing over of the cheque. Once the signature on the cheque is admitted or proved, the presumption kicks in.

So who proves what? The complainant establishes the cheque and its dishonour; the presumption then does the heavy lifting on the debt. The accused must rebut it, and can, but on the standard of preponderance of probabilities, not beyond reasonable doubt. That means the accused doesn’t need to conclusively disprove the debt; they need to raise a probable defence that makes the court doubt the debt’s existence. Bare denial won’t do it. Evidence, admissions extracted in cross-examination, documents, and probabilities will.

The contrary view that was overruled

There was, for a while, a softer view for the accused, and it’s important precisely because you should not rely on it. In Krishna Janardhan Bhat v. Dattatraya G. Hegde, (2008) 4 SCC 54, a 2008 decision took a narrower reading of the Sec. 139 presumption, suggesting the complainant had to establish the debt’s existence more affirmatively. Defence counsel leaned on it for years.

Then Rangappa, sitting as a three-judge bench, effectively overruled that narrower view on the debt-presumption point, and restored the fuller presumption. The downstream consequence is one the accused must internalise: you can no longer argue that the debt is simply presumed away, or that the complainant carries the initial burden to prove it. The presumption is against you from the moment the cheque is admitted. Cite the 2008 view as current law and you’ll be corrected in open court. It is history, not authority.

Genuine defences that work

So what actually works? The defences that succeed all attack the “legally enforceable debt” foundation or the integrity of the instrument:

- No legally enforceable debt: show the cheque was not issued to discharge any real, enforceable liability (for instance, it was a gift, or for a transaction that fell through).

- Time-barred debt: a debt already barred by limitation is not “legally enforceable”, so a cheque issued for it may not sustain a Sec. 138 conviction.

- Blank or undated cheque misused: where a cheque was handed over blank and later filled in beyond any authority, the accused can challenge it, drawing on the rules around inchoate instruments in Section 20 of the Negotiable Instruments Act, 1881.

- Material alteration: a cheque altered in a material particular after issue can be challenged under Section 87 of the Negotiable Instruments Act, 1881.

Notice what unites these: each one gives the court a concrete, evidence-backed reason to doubt the debt or the instrument. That’s what “rebutting the presumption on preponderance of probabilities” looks like in practice. A defence that is only “I don’t owe anything” without any of this is not a defence; it’s a hope.

Bail and appearance

Is a cheque bounce offence bailable, and how does bail work? Yes, it’s bailable, which changes the emotional temperature entirely. Because bail is available as of right for a bailable offence, an accused is generally not looking at custody the way one would in a serious cognizable case. Our overview of how offences are classified as bailable or non-bailable sets out why that classification carries the weight it does.

At the first summons, appearance matters. The accused (or counsel, where the court permits exemption from personal appearance) should appear rather than let the matter proceed ex parte, which can invite a warrant. Practically, a lawyer often seeks exemption from personal appearance in routine hearings so the accused isn’t dragged to court on every date. Ignoring the summons entirely is the worst option: it converts a manageable bailable matter into a warrant problem.

The security-cheque defence: when it works and when it fails

“It was just a security cheque.” If cheque bounce defences had a greatest-hits list, this would be the number one track, and the most misunderstood. Accused persons reach for it reflexively, sure it’s a magic exit. It isn’t. But it isn’t worthless either. The honest answer, the one most guides skip, is that it works in a narrow band of situations and fails everywhere else, and knowing the difference is the whole game.

Sec. 138 can apply to a security cheque. The label “security cheque” is not, by itself, a defence, because what matters is whether a legally enforceable debt existed when the cheque was presented, not what the parties called the cheque at the outset. Where the underlying debt had crystallised, a security cheque that bounces attracts Sec. 138 like any other.

Why “it was only a security cheque” usually fails

Here’s why the argument usually collapses. A cheque given as “security” for a loan or an obligation is still a cheque issued in relation to a debt. If, by the time it’s presented, the debt has become due and payable, the security cheque is now doing exactly what a cheque does: discharging (or attempting to discharge) an enforceable liability. The Sec. 139 presumption from the previous section applies, and the accused is back to rebutting a presumed debt.

So the drawer who says “you were only supposed to hold it as security” but who genuinely owed the money loses. The court’s focus is on the debt’s existence at presentation, not on the private understanding at issue. In our view, this is the single most over-relied-on and under-analysed defence in the whole area, treated superficially by nearly every online guide, and it costs accused persons dearly when their lawyer promises more than the label can deliver.

The narrow window where it succeeds

Now the band where it genuinely works. The security-cheque defence succeeds where no debt had crystallised at all, where the liability the cheque secured was contingent and the contingency never arose. If the cheque secured a facility that was never drawn, or an obligation that was discharged another way, or a liability that simply never came into existence, then at presentation there was no legally enforceable debt to satisfy, and the Sec. 139 presumption, honestly applied, is rebuttable.

The distinction, then, is not “security cheque yes/no” but “enforceable debt at presentation yes/no”. Run the security-cheque defence only when you can show the debt hadn’t arisen; run it as a mere label, and it fails. This is exactly the kind of fact-sensitive line that rewards careful pleading and sinks lazy pleading.

Blank or undated security cheque later filled in

A common variant: the drawer handed over a blank or undated cheque as security, and the payee later filled in the amount and date. Does that help the drawer? Sometimes. The point of attack is authority to complete: under Sec. 20, a person who delivers an inchoate (incomplete) instrument gives the holder authority to complete it, but only for an amount covered by the instrument and intended by the parties. Fill it beyond any agreed or intended liability, and the accused has a genuine challenge.

The practical trouble for the drawer is proof. Once the signature is admitted, the presumption assumes a proper filling-in, so the accused must lead evidence that the completion exceeded the authority given. A common question accused persons raise is whether simply saying “I gave it blank” is enough, and the honest answer is no: you must show what the agreed limit was and that it was breached. Absent that, the blank-cheque story is just another version of the failed label defence.

Cheque bounce case against a company and its directors (Sec. 141)

Cheques don’t always come from individuals. When the cheque is a company’s, a fresh layer opens up: who, exactly, do you prosecute, and who can be dragged in personally? This is where a lot of complaints overreach (naming every director on the board) and a lot of directors panic unnecessarily (assuming a board seat equals liability). The section that governs all of this is Sec. 141, and it draws sharp lines.

Where a company issues the dishonoured cheque, the company is the primary offender, and a director or officer is liable only if they were in charge of, and responsible to, the company for the conduct of its business at the relevant time. Merely holding a directorship is not enough. The complaint must say, specifically, that the person was in that responsible role, or the case against them fails.

How Sec. 141 works

Under Section 141 of the Negotiable Instruments Act, 1881, when the offence is committed by a company, every person who at the time of the offence was in charge of and responsible to the company for the conduct of its business is deemed guilty, along with the company itself. The key words are “in charge of and responsible for the conduct of business”. That is a functional test about actual responsibility, not a formal test about titles.

So the company must be arraigned as an accused (you generally can’t convict a director for the company’s offence without the company in the dock), and individual liability rides on the responsibility test. This is why blanket “sue everyone on the board” complaints are vulnerable: a director who had nothing to do with running the business, and against whom no specific role is pleaded, has a strong exit.

Individual drawer vs company drawer

How does a company case differ from an individual one in the drafting? With an individual drawer, the drawer is simply the accused, and the debt-and-presumption analysis runs directly. With a company drawer, the complaint must plead specific averments against each individual it seeks to make liable: that this director or signatory was, at the relevant time, in charge of and responsible for the conduct of the company’s business.

Vague, cut-and-paste averments (repeating the statutory words without facts) are exactly what get individual accused discharged. Is naming the managing director or the cheque signatory usually safer? Yes, because their responsible role is easier to establish, but even then, the averment has to be made and, if challenged, supported. The lesson for a payee is to plead role and responsibility with facts; the lesson for a director is to test whether those facts were pleaded at all.

Non-executive, independent and resigned directors

What about the director who wasn’t running anything, the non-executive board member, the independent director, or someone who had already resigned before the cheque was issued? These are the classic escape routes from vicarious liability under Sec. 141. A non-executive or independent director not in charge of day-to-day business, and a director who had resigned before the relevant date, ordinarily should not be liable, because the responsibility test isn’t met.

The catch is that these escapes usually have to be established on the record; a director can’t simply assert “I was non-executive” and walk. Resignation is best proved by the filing that records it; a non-executive role, by showing the actual division of responsibility. For the accused director, the message is: your defence exists, but you must be able to document it. For the complainant, the message is: don’t waste the case suing directors whose non-involvement is on the public record.

Interim compensation, settlement and appeal: Sec. 143A, 147 and 148

This is the section where money actually moves, before conviction, at settlement, and on appeal, and it’s where the 2024 development this guide opened with pays off. Three provisions do the heavy lifting: Sec. 143A (pay something during trial), Sec. 147 (settle and close), and Sec. 148 (deposit to appeal). Read together, they show that a cheque bounce case is, financially, a series of pressure points, and each one can be used or resisted.

Sec. 143A lets a trial court order the accused to pay interim compensation of up to 20% of the cheque amount during the trial; Sec. 147 makes the offence compoundable so the parties can settle at any stage; and Sec. 148 requires an appellant convicted under Sec. 138 to deposit a minimum of 20% of the fine or compensation as a condition of the appeal. The big recent shift is that the Sec. 143A power is discretionary, not automatic.

Interim compensation under Sec. 143A

Start with the provision that opened this guide. Section 143A of the Negotiable Instruments Act, 1881 empowers a trial court to direct the accused to pay the complainant interim compensation of up to 20% of the cheque amount, and it can be ordered at the trial stage, before any conviction. For years this was granted almost mechanically. Then Rakesh Ranjan Shrivastava v. State of Jharkhand, 2024 INSC 205 changed the tenor: in 2024, the Supreme Court held that “may” in Sec. 143A means the power is discretionary and directory, not mandatory.

What must a court weigh now? The Court indicated parameters: whether there’s a prima facie case, whether the accused has a plausible defence, the accused’s financial condition, and, crucially, reasons must be recorded. Is interim compensation therefore “mandatory”? No, not anymore, and that single word shift is the payoff of this guide’s opening story. For a payee, it means your interim-compensation prayer now needs substance; for an accused, it means a genuine defence can resist the 20% deposit that used to be near-automatic.

Settling out of court: compounding under Sec. 147

Most cheque bounce cases don’t end in a fought judgment; they settle. Section 147 of the Negotiable Instruments Act, 1881 makes the Sec. 138 offence compoundable, meaning the complainant and accused can compromise and close the case, at more or less any stage. The Supreme Court in Meters and Instruments actively encouraged early compounding and compensation-first disposal, treating quick closure with the complainant made whole as the preferred outcome.

There’s a practical cost to settling late, though. In Sanjabij Tari v. Kishore S. Borcar, 2025 INSC 1158, the Supreme Court set out a graded cost of compounding that rises the longer you wait: nil if the offence is compounded before the accused leads defence evidence, an additional 5% of the cheque amount if compounded after defence evidence but before judgment, 7.5% at the Sessions Court or High Court appellate stage, and 10% by the time the matter reaches the Supreme Court. The direction of travel is unmistakable: settle sooner rather than later, and you keep more.

Appealing a conviction and the Sec. 148 deposit

Convicted, and want to appeal? There’s a price of admission. Section 148 of the Negotiable Instruments Act, 1881 provides that an appellate court, where an appeal is filed against a Sec. 138 conviction, may order the appellant to deposit a minimum of 20% of the fine or compensation awarded, as a condition connected to suspension of sentence during the appeal. This is designed to stop convicted drawers from using appeals purely to delay payment.

How does this differ from Sec. 143A? Timing and posture. Sec. 143A operates at the trial stage, before conviction, on an accused presumed innocent, which is exactly why the 2024 ruling made it discretionary. Sec. 148 operates after a conviction, on an appellant who has already been found guilty, so a mandatory-style deposit sits more comfortably there. Same 20% figure, very different stages, don’t confuse the two.

Compounding vs quashing vs acquittal

Three different ways a cheque bounce case can end, and they are not interchangeable. Compounding is a settlement: the parties compromise, the complainant is paid, and the case is closed by consent. Quashing is the High Court exercising its inherent power to terminate the proceedings (often to give effect to a settlement, or where continuing would be an abuse of process). Acquittal is the trial court’s finding, after trial, that the offence wasn’t made out.

Which one should you aim for? It depends on where you are. A settled matter is cleanest closed by compounding, and quashing if a court’s order is needed to record it; a genuinely defensible case with no settlement is fought to acquittal. The mistake is treating them as a menu you pick from freely; each has its own gateway, and choosing wrong wastes time and money.

The trial and what happens next: summary trial, re-presentation and the absconding accused

Once a complaint is filed and summons issued, what does the courtroom part actually look like? Cheque bounce trials have their own procedural shape, deliberately streamlined, because the system is drowning in them. This section covers how the trial runs, what happens if you need to present the cheque again, and the two headaches that dominate the back end: the accused who pays late, and the accused who vanishes.

A Sec. 138 case is ordinarily tried as a summary trial, a faster, lighter procedure, with the Supreme Court directing courts to run these trials day-to-day and aim to conclude them within six months. A payee can re-present a cheque within its validity and issue a fresh notice on a subsequent dishonour, and a drawer who pays after the notice but before filing generally escapes the offence, while one who absconds faces coercive process.

Summary trial vs summons trial

Under Section 143 of the Negotiable Instruments Act, 1881, a Sec. 138 complaint is to be tried summarily. A summary trial compresses the process: evidence is streamlined, affidavit evidence is used, and the aim is speed. That’s good for a complainant who wants a quick result and bearable for an accused who won’t be dragged through a full-blown summons trial for a bounced cheque.

But a Magistrate can convert a summary trial into a summons trial where the nature of the case makes summary disposal inappropriate (for example, where a sentence beyond the summary limit seems likely). The Supreme Court, in In Re: Expeditious Trial of Cases Under Section 138 of NI Act, 1881, (2021) 16 SCC 116, directed that a Magistrate must record reasons before making that conversion, precisely to stop routine, unexplained conversions that slow everything down. So conversion is possible, but it’s now a reasoned exception, not a reflex.

Clearing the backlog: the 2021 directions

Cheque dishonour is one of the most clogged categories of criminal litigation in India, and the courts know it. In its 2021 directions, the Supreme Court laid down a package to speed things up: record reasons before any summary-to-summons conversion, conduct trials on a day-to-day basis, target conclusion within six months, and, sensibly, hold a single trial for multiple cheques arising from the same transaction rather than a separate case per cheque.

More recent directions point the same way. In Sanjabij Tari v. Kishore S. Borcar, 2025 INSC 1158, the Supreme Court issued a further package to unclog Sec. 138 dockets: each District Court must operationalise dedicated online payment facilities through secure QR codes or UPI links, with the summons expressly telling the accused they can pay the cheque amount at the initial stage itself; summons may be served dasti (by hand, through the complainant) and by electronic means; and there is no requirement to issue a pre-cognizance summons to the accused under Sec. 223 of the BNSS in an NI Act complaint. The consistent theme across 2021 and 2025 is impatience with delay.

Re-presenting the bounced cheque

Can you present the bounced cheque again and start over? Yes, within limits. The Supreme Court in MSR Leathers v. S. Palaniappan, (2013) 1 SCC 177 held that a payee may found a complaint on a subsequent dishonour of the same cheque, even if no complaint was filed on an earlier presentation, so long as the cheque is presented within its validity. Each valid presentation that ends in dishonour can generate a fresh cause of action if you issue a fresh notice.

This is the practical rescue for the payee who missed a notice deadline (as we flagged earlier) or who wanted to give the drawer one more chance. Present within validity, get a fresh return memo, send a fresh 30-day notice, and the clock resets. The limit, again, is the cheque’s validity: once it’s stale, re-presentation is over, and so is this escape route.

If the accused pays late or absconds

Two end-game scenarios. First: the drawer pays after receiving the notice but before you file the complaint. In that situation, the offence generally isn’t complete, because paying within the window (or before the case is instituted, in practice) removes the very default the section punishes. The payee who’s been paid has, sensibly, lost the criminal case, but gained the money, which was the point.

Second: the accused absconds or dodges summons. The court isn’t powerless. It can issue coercive process to secure attendance, and because the offence completes on the drawer’s failure to pay, avoidance doesn’t undo the offence the way timely payment does. What experienced practitioners know is that an absconding accused often hurts their own position, courts take a dim view of evasion, and the modern push toward e-summons and electronic service (noted above) is steadily shrinking the room to hide.

Cheque bounce case vs money-recovery suit: criminal complaint vs Order XXXVII CPC

Here’s a question that separates people who understand this area from people who don’t: if the cheque bounced, should you file a criminal complaint, a civil suit, or both? Most readers assume it’s either/or. The sophisticated answer is that they do different jobs, and the smartest creditors often run both. This section lays the two remedies side by side and explains the dual-track strategy that competitors rarely mention.

A Sec. 138 criminal complaint and an Order XXXVII CPC summary suit are two different remedies for the same bounced cheque: the criminal complaint delivers pressure, a possible conviction, and compensation, while the civil summary suit delivers an executable money decree. They can be pursued together, and increasingly are, because each supplies something the other lacks.

Two remedies, two goals

The criminal route, Sec. 138, is about deterrence and compensation. It threatens the drawer with conviction and uses the fine/compensation mechanism to route money to the payee. Its leverage is the discomfort of a criminal case. The civil route, a summary suit under Order XXXVII of the Code of Civil Procedure, 1908, is about recovery, pure and simple: it aims at a decree for the money, which you can then execute against the drawer’s assets.

Why does the distinction matter? Because a criminal conviction is not, by itself, an execution warrant against property. A civil decree is. If your real goal is to seize a defaulter’s bank balances or attach assets, the civil decree is the instrument that does it; the criminal case, meanwhile, keeps the pressure on. Two goals, two tools.

Sec. 138 complaint vs Order XXXVII CPC suit table

The two remedies, compared:

| Basis | Sec. 138 NI Act complaint | Order XXXVII CPC summary suit |

|---|---|---|

| Nature | Criminal (special statute) | Civil |

| Primary goal | Punishment + compensation / pressure | Executable money decree |

| Forum | Magistrate | Commercial / civil court |

| Typical speed | Summary trial, 6-month target | Summary suit (leave-to-defend gated) |

| What you get | Fine up to twice the cheque amount + possible jail + compensation | A decree you can execute against assets |

| Best when | You want leverage + a criminal deterrent | You want guaranteed recoverability |

Can I run both for the same cheque?

Yes. Running a Sec. 138 complaint and an Order XXXVII CPC suit for the same cheque is permissible, and it’s a deliberate strategy, not double-dipping, because the two proceedings seek different things: the criminal case seeks punishment and compensation, the civil suit seeks a recoverable decree. A drawer facing both feels pressure on two fronts at once.

Is there a risk of the money being counted twice? In practice, courts adjust so the creditor doesn’t recover the same sum twice over, any compensation actually received on the criminal side is accounted for against the civil claim. The point of the dual track isn’t to collect double; it’s to combine the leverage of the criminal case with the enforceability of the civil decree. For a payee who’s been strung along, that combination is powerful. If you decide to run the civil track, our practical guide to drafting a money recovery suit walks through how the Order XXXVII summary procedure works in practice.

Why sophisticated creditors run both

Now the non-obvious part, the downstream consequence most guides miss. As courts increasingly treat Sec. 138 as a compensatory mechanism more than a punitive one, the criminal case has quietly become a pressure-and-partial-recovery tool rather than a reliable route to a clean, executable recovery. That shift is precisely why experienced creditors don’t rely on it alone. They run the criminal complaint for the settle-or-face-conviction pressure it generates, and simultaneously run the civil summary suit to secure a decree they can actually execute if the drawer refuses to settle.

The sequencing is where the craft lies: the criminal case pushes the drawer toward the table, and the civil decree waits as the enforceable fallback if the push fails. Most creditors who only file the criminal complaint discover, a year in, that they have leverage but no asset to seize. The ones who understood the split filed both at the outset.

Sec. 138 complaint: pressure + compensation, before a Magistrate Order XXXVII CPC summary suit: executable money decree

Common mistakes that sink a cheque bounce case (both sides)

Most cheque bounce cases aren’t lost on grand points of law. They’re lost on avoidable, self-inflicted errors, a defective notice, a missed deadline, an ignored summons. This section is the pre-flight checklist for both sides: the mistakes that get a complainant’s case dismissed, and the mistakes that quietly destroy an accused’s defence. Read the half that’s yours, and then read the other half, because knowing the opponent’s likely error is its own advantage.

Complainant mistakes that get a complaint dismissed

If you’re the payee, these are the errors that end cases at the threshold. A late or defective demand notice, sent after 30 days or demanding the wrong amount, tops the list. So does filing beyond the one-month limitation without a proper condonation plea. So does filing in the wrong court, now that jurisdiction is fixed at your bank branch. And the quiet killer: no proof of the debt, relying on the bounce alone and having nothing to answer the “no legally enforceable debt” defence.

What’s the through-line? Each of these is a precondition the complainant controlled and got wrong. Which is the deadliest? In our experience, the debt-proof gap and the wrong-amount notice, because they can look fine at filing and only surface as fatal at trial, when it’s too late to fix. Build the paper trail before you file, not after.

Accused mistakes that weaken the defence

If you’re the accused, the damage is usually self-inflicted too. Ignoring the demand notice entirely (a silent drawer looks like a guilty one, and forfeits the chance to set up a defence on record) is mistake number one. Not replying to the notice to assert your version, carelessly conceding the signature or the debt, missing appearances and inviting a warrant, and turning up to trial with no rebuttal evidence, all of these hand the case to the complainant.

The pattern here is passivity. Because the Sec. 139 presumption already tilts against the accused, doing nothing is not neutral; it’s losing slowly. A drawer who replies to the notice, sets up the defence early, appears (or seeks exemption properly), and brings evidence to rebut the presumption is in a completely different position from the one who hoped it would go away. It won’t.

Shared procedural traps

Some traps catch both sides. Mishandling a re-presented cheque, presenting again but botching the fresh notice, or filing on the earlier cause of action after it lapsed, snares complainants and confuses accused. Condonation-of-delay pleadings are another: a complainant who files late without a proper application, or an accused who fails to spot and challenge that gap, both lose ground. And service proof, the postal receipts and returned envelopes, matters to the complainant proving deemed service and to the accused testing whether the notice was ever validly served.

The common lesson is documentary discipline. Keep every memo, receipt, envelope, and reply; date everything; and never assume the court will fill a gap you left. A cheque bounce case is won on a tidy file as much as on the law, and lost on a sloppy one.

Cheque bounce myths vs the law

A few stubborn myths circulate about cheque bounce cases, and each one leads people to make bad decisions, drawers who ignore notices, payees who march to the police. So which of the things “everyone knows” about a bounced cheque are actually wrong? Here they are, matched against what the law actually says. Short, blunt, and worth reading whichever side you’re on.

“Cheque bounce always means jail”

The myth: a bounced cheque sends the drawer to prison. The reality: jail is the exception. Although Sec. 138 permits imprisonment up to two years, courts overwhelmingly use the fine-as-compensation route, treating the offence as primarily compensatory and directing payment to the payee rather than incarceration. Most cheque bounce cases end in payment or settlement, not a prison term. The threat of jail is real as leverage; the routine outcome is money changing hands.

“The BNS 2023 scrapped Section 138”

The myth: the new criminal codes repealed the cheque bounce offence. The reality: they didn’t. The NI Act is a special statute, and Sec. 138 stands intact; the BNSS changed general criminal procedure, but that procedure applies subject to the NI Act’s special provisions. A drawer who believes the section is gone and ignores a notice is walking straight into an avoidable conviction.

“The police will file my case”

The myth: you report a bounced cheque to the police and they file it. The reality: it’s a private complaint before a Magistrate under Sec. 142, filed by the payee or holder in due course, not a police FIR. The police have no role in a bare Sec. 138 matter. A payee who wastes the limitation period at a police station instead of drafting a complaint may find the window to file has narrowed dangerously.

Frequently asked questions

1. What is the punishment for cheque bounce under Sec. 138? The punishment is imprisonment for up to two years, or a fine that may extend to twice the cheque amount, or both. In practice, courts lean toward the fine-as-compensation route, using it to route the cheque amount (and often interest and costs) to the complainant rather than sending the drawer to prison. Jail is the exception, not the norm.

2. Within how many days must the legal notice be sent after the cheque bounces? The demand notice must be sent within 30 days of your receiving intimation from the bank that the cheque has been returned unpaid. This 30-day window is strict. Miss it, and the only rescue is to re-present the cheque within its validity and issue a fresh notice on the new dishonour; once the cheque is stale, a missed notice deadline is usually fatal.

3. How many days does the drawer get to pay after receiving the notice? The drawer has 15 days from receiving the demand notice to pay the cheque amount. Only if the drawer fails to pay within those 15 days does the offence under Sec. 138 complete. This is why a complaint filed before the 15-day window expires is premature and liable to be dismissed, the cause of action simply hasn’t arisen yet.

4. Within how much time must the complaint be filed after the notice period? Once the 15-day pay window expires, the cause of action arises on the 16th day, and the complaint must be filed within one month (30 days) of that date under Sec. 142(b). Filing later requires a specific application to condone the delay, which the court may allow on sufficient cause. Don’t rely on condonation; treat the one-month window as firm.

5. How long is a cheque valid for presentation? A cheque is valid for presentation for three months from the date written on it. Present it after it goes stale and the bank returns it for validity rather than insufficiency, and that return generally won’t support a Sec. 138 case. Always present well within the three-month window, and count the window from the date on the cheque’s face.

6. Which court do I file a cheque bounce case in? You file where your own bank branch, the branch where you presented or deposited the cheque for collection, is located. This has been the rule since the 2015 amendment to the NI Act (Sec. 142(2) and 142A). Filing in the wrong court is a common reason complaints are returned, so anchor the complaint to your bank branch’s location and state that basis clearly.

7. Is a cheque bounce case civil or criminal? It is criminal in nature, punishable with imprisonment and fine, but it is prosecuted as a private complaint, not through a police FIR. That hybrid character is deliberate: Parliament criminalised cheque dishonour in 1988 to give creditors a sharp deterrent, while leaving the aggrieved payee to drive the prosecution. You can also run a separate civil recovery suit in parallel.

8. Is filing a cheque bounce case an FIR or a complaint? It is a complaint, not an FIR. Under Sec. 142, a court takes cognizance of a Sec. 138 offence only on a written complaint by the payee or holder in due course. The police neither register nor investigate it. Going to a police station to “lodge an FIR” for a bounced cheque achieves nothing and wastes your limitation period.

9. How long does a cheque bounce case take in India? Although the Supreme Court has directed courts to aim for a six-month conclusion, the practical reality in busy courts is often longer, frequently a year or more, because of docket load and the accused’s appearances. Treat the six-month target as an aspiration rather than a promise, and plan your recovery strategy (including a possible parallel civil suit) accordingly.

10. Is cheque bounce a bailable offence, and how do I get bail? Yes, a Sec. 138 offence is bailable, so the accused is entitled to bail as of right rather than at the court’s discretion. This means the custody fear people associate with a “criminal case” is largely misplaced here. The accused should still appear (or seek exemption from personal appearance through counsel) at the first summons, because ignoring it can invite a warrant.

11. Can I settle a cheque bounce case out of court? Yes. The offence is compoundable under Sec. 147, so the complainant and accused can compromise and close the case at more or less any stage. Courts actively encourage early settlement, and settling sooner is generally cheaper for the accused, as the cost of compounding tends to rise the later the settlement comes. A recorded settlement can also be given effect through the appropriate court order.

12. What is interim compensation under Sec. 143A, and is it mandatory? Sec. 143A lets a trial court order the accused to pay up to 20% of the cheque amount as interim compensation during the trial, before conviction. Since a 2024 Supreme Court ruling, this power is discretionary, not mandatory: the court must weigh the prima facie case, the accused’s plausible defence and financial condition, and record reasons. It is no longer granted automatically.

13. Can a cheque bounce case be filed against a company and its directors? Yes, under Sec. 141. The company is the primary offender, and a director or officer is liable only if they were in charge of and responsible for the conduct of the company’s business at the relevant time. Merely being a director is not enough; the complaint must plead specific averments. Non-executive, independent, or already-resigned directors often have a strong exit.

14. Can I present the bounced cheque again and issue a fresh notice? Yes, within the cheque’s validity. The Supreme Court has held that a payee may found a complaint on a subsequent dishonour of the same cheque, with a fresh 30-day notice, even if no complaint was filed on an earlier presentation. This is the practical rescue for a missed notice deadline, but it ends once the cheque goes stale, so you can’t re-present indefinitely.

15. Does Sec. 138 apply to a security cheque? It can. The “security cheque” label is not, by itself, a defence, because what matters is whether a legally enforceable debt existed when the cheque was presented, not what the parties called the cheque at the start. The defence succeeds only in the narrow band where no debt had crystallised, where the liability the cheque secured was contingent and never actually arose.

16. Does Sec. 138 apply if the account was closed, not just short of funds? Yes. An “account closed” return is treated as dishonour for insufficiency of funds, because a closed account cannot honour the cheque. A drawer cannot escape Sec. 138 by closing the account after issuing the cheque. Similarly, a “stop payment” instruction generally attracts Sec. 138 where a legally enforceable debt exists, because a drawer cannot defeat liability simply by instructing the bank not to pay.

17. Did the Bharatiya Nyaya Sanhita 2023 replace Sec. 138 NI Act? No. The NI Act is a special statute, and Sec. 138 remains intact. The Bharatiya Nagarik Suraksha Sanhita, 2023 replaced the old criminal procedure code for general process, but that procedure applies subject to the NI Act, not over it. A drawer who assumes the new codes killed the cheque bounce remedy, and therefore ignores a notice, is making a costly mistake.

18. Cheque bounce case vs Order XXXVII CPC suit: which recovers money faster? They do different jobs. The Sec. 138 criminal complaint delivers pressure and compensation but not a directly executable property remedy; the Order XXXVII CPC summary suit delivers an executable money decree, often quickly where the drawer has no real defence to obtain leave. For guaranteed recoverability, the civil decree is the instrument; for leverage, the criminal case. Many creditors run both for the same cheque.

References

Case Law

- C.C. Alavi Haji v. Palapetty Muhammed, (2007) 6 SCC 555; 2007 AIR SCW 3578

- Dashrath Rupsingh Rathod v. State of Maharashtra, (2014) 9 SCC 129; AIR 2014 SC 3519

- In Re: Expeditious Trial of Cases Under Section 138 of NI Act, 1881, (2021) 16 SCC 116; SC judgment PDF

- K. Bhaskaran v. Sankaran Vaidhyan Balan, (1999) 7 SCC 510; AIR 1999 SC 3762

- Krishna Janardhan Bhat v. Dattatraya G. Hegde, (2008) 4 SCC 54; AIR 2008 SC 1325 (narrower view of the Sec. 139 presumption, since overruled by Rangappa on the debt-presumption point)

- Meters and Instruments Pvt. Ltd. v. Kanchan Mehta, (2018) 1 SCC 560; AIR 2017 SC 4594

- MSR Leathers v. S. Palaniappan, (2013) 1 SCC 177; 2013 AIR SCW 597

- Rakesh Ranjan Shrivastava v. State of Jharkhand, 2024 INSC 205; (2024) 4 SCC 419

- Rangappa v. Sri Mohan, (2010) 11 SCC 441; AIR 2010 SC 1898

- Sanjabij Tari v. Kishore S. Borcar, 2025 INSC 1158; 2025 SCC OnLine SC 2069

Statutes

- Negotiable Instruments Act, 1881: sections cited 20, 87, 118(a), 138, 139, 141, 142, 142(2), 142A, 143, 143A, 145, 147, 148

- General Clauses Act, 1897: section cited 27

- Code of Civil Procedure, 1908: Order XXXVII

This article is for informational purposes only and does not constitute legal advice. For specific legal guidance, consult a qualified legal professional.

Allow notifications

Allow notifications